Home Equity Loan

A personal loan secured by the value of a property

What is a Home Equity Loan?

A home equity loan is a type of consumer borrowing that allows homeowners to borrow and use personal equity in residential property as collateral. Such a type of loan is also known as a second mortgage or home equity installment. The loan amount is determined by the current market value of the property.

Home equity loans are frequently used as consumer credit and can finance major consumption expenses such as medical, education, and home repairs. It reduces the actual home equity by creating a lien against the property of the borrower. Such loans exist in two forms – variable-rate credit lines and fixed-rate loans. The idea of offering two types of equity lines of credit is to separate heterogeneous borrowers.

Summary

- A home equity loan is personal borrowing secured by the value of a property.

- The loan is typically offered either as a closed-end loan, which requires the repayment of installment and principle in equal amounts, or as a home equity line of credit, which comes with more flexible repayment schedules.

- The Home Equity Loans Consumer Protection Act (HELCPA) regulates the advertisement of home equity loans by compelling lenders to disclose the consequences of defaulting, eligibility criteria, and conditions for termination.

Understanding Home Equity Loans

Fundamentally, a home equity loan is a mortgage contract in which a borrower’s property serves as collateral. Lenders use a combined loan-to-value (CLTV) ratio of 80% and above, alongside credit rating and payment history to determine the amount for which the borrower is eligible.

Home equity loans offer homeowners an option to convert their home equity into cash, especially if such spendable funds are channeled into the renovation to increase the property’s value. At one end of the spectrum, a homeowner may sell his property and buy a less expensive home, and on the other end, he may refinance the current mortgage and borrow more to pay off the old loans and closing costs.

The availability of the alternatives above significantly influences the home equity credit market. Since homeowners often pay off other debts, refinancing is likely to occur in large volumes when interest rates fall.

Taxation of Home Equity Loans

Home equity lending in the form of home equity loans became popular in the late 1980s. Initially, nearly all home equity borrowing was of the traditional type, which imposed federal income tax deductions for debts secured by homes. The Tax Reform Act of 1986 marked the phaseout of the unfair tax on mortgage debt.

The deductions of interest on most of the previously-financed expenditures – through personal cash loans, credit cards, or auto loans – become favorable to consumers. Although relatively attractive, the tax law changes left in place a major exception – mortgage interest remained tax-deductible.

The deduction for interest was suspended in the Tax Cuts and Jobs Act of 2017. The new tax law posits that a home equity loan acquired to purchase, construct, or renovate taxpayers’ lettings attract a deductible interest. However, the loan cannot be used for other non-qualified expenses, such as paying personal debt or paying college fees.

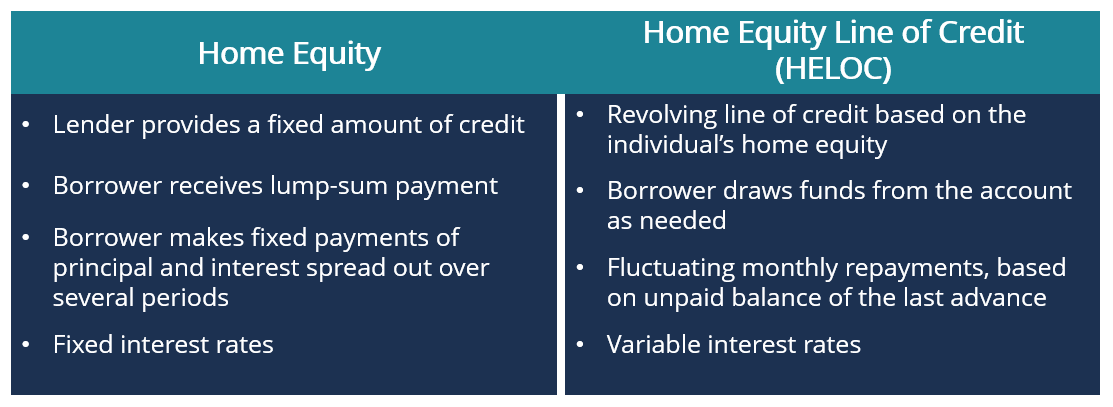

Home Equity Lines of Credit (HELOCs) vs. Fixed-Rate Loans

A home equity line of credit (HELOC) is a revolving credit that allows multiple borrowings at the consumer’s discretion for a term proposed by the lender. Furthermore, its payment schedules are more flexible than a fixed-rate loan. Although it offers a variable interest rate, some creditors may assign a fixed interest rate.

Comparatively, a fixed-rate home equity loan allows the borrower to receive a single lump-sum payment, which is usually completed over a series of repayments. The interest rate on a fixed-rate home loan is ordinarily fixed for the life of the loan. If the borrower fails to remit the regular installments, the property can be auctioned to service the remaining debt.

In such regard, taking a home equity loan means putting your home on the line, and a decrease in real estate value can attract more debt than the market worth of the property. If you intend to relocate, the loss on the property’s sale may suffice, or even become immovable.

Regulating Home Equity Loans

The popularity of home equity loans triggered the U.S. Congress to enact the Home Equity Loans Consumer Protection Act (HELCPA) to regulate their disclosure and advertising. The law came forth as a substitute for the Truth-in-Lending Act, which obligated lenders to provide full disclosure statements and consumer pamphlets within the time they offer an application to a prospective consumer borrower.

The disclosure statement must state that (1) default on the home equity loan may result in the loss of property; (2) some conditions must be met when applying for a home equity loan, and (3) the lender, under certain conditions, may terminate the arrangement and accelerate the standing balance, reduce the plan’s credit limit, prohibit the further extension of the credit, or impose fees upon the termination of the account.

Additionally, the law requires that the lender must disclose the annual percentage rate imposed if the plan contains a fixed interest rate.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: