Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A mortgage used to finance high-valued properties that are above the Federal Housing Finance Agency (FHFA) conforming loan limits

A jumbo loan is a mortgage used to finance high-valued properties that are above the Federal Housing Finance Agency (FHFA) conforming loan limits. Jumbo loans are also known as non-conforming loans since they exceed the conventional local conforming loan limits as determined by the FHFA enterprises, Fannie Mae and Freddie Mac.

Properties that exceed the loan limit set for the metro area where they are located will require a jumbo loan to finance. Lenders consider jumbo loans riskier than conforming loans because they are not guaranteed by Fannie Mae and Freddie Mac. It means mortgage lenders are unable to sell jumbo loans to Fannie Mae and Freddie Mac, leaving them vulnerable to losses in the event of default.

Jumbo loans are available in a variety of terms, including fixed-rate and adjustable-rate loans. Such types of loans typically have higher interest rates, firmer underwriting conditions, and require a larger deposit than conventional conforming loans. They are generally used for financing the following:

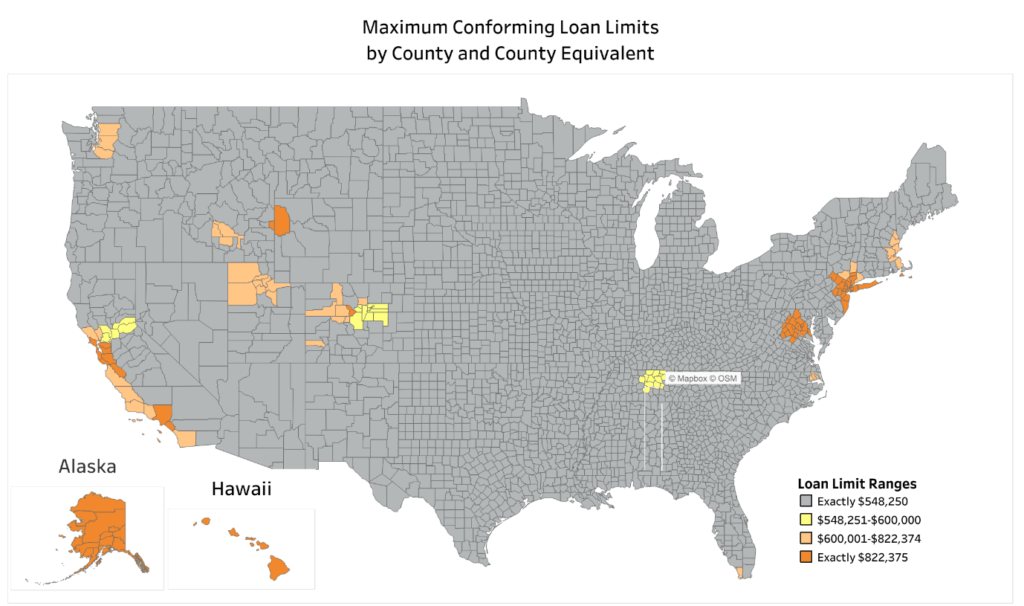

In 2021, most U.S. counties’ conforming loan limit is $548,250, but other higher-cost areas impose a limit of $822,375. Therefore, any amount above such limits is considered a jumbo loan. Expensive housing markets with high conforming loan limits include New York, San Francisco, Alaska, Hawaii, Washington D.C., and other metro areas.

It is important to understand that conforming loan limits apply to single-unit properties only; multi-unit properties are subject to higher separate conforming limits determined by Fannie Mae and Freddie Mac. Apart from size and other factors, jumbo loans are not very different from conventional mortgage loans as they share the same structure, payment schedules, and other details.

Federal Mortgage Protection Process

Lenders issue conventional mortgages to customers and then sell them to Fannie Mae and Freddie Mac, which are authorized to buy mortgage loans that conform to FHFA’s limits. The purchase relieves lenders to issue more mortgage loans.

After the purchase, Fannie Mae and Freddie Mac bundle the loans with similar loans and sell them on the secondary mortgage market as mortgage-backed securities (MBS). The same process also occurs for jumbo loans without both federal agencies but involving different investors.

Conforming loan limits as set by the FHFA vary by state, market, or county. The 2021 conforming loan limit of $548,250 for a single-family unit is common in most parts of the United States, as illustrated by the FHFA map below.

However, high-cost areas with a median home price higher than the national average carry a higher limit than low-cost areas. An FHFA maximum conforming loan limits map by county is illustrated below:

Areas with the highest conforming loan limits in 2021 include Alaska, Hawaii, several counties in California, Virginia, New York, and New Jersey.

Jumbo loans do not necessarily mean high interest rates as several aspects are factored in. Some lenders are known to offer competitive interest rates that can be lower than conforming loans. Interest rates on jumbo loans are determined by several factors: the lender, market conditions, borrower credit score, down payment, and borrower’s income and cash reserves.

According to bankrate.com, on 29 June 2021, a 30-year jumbo loan incurred a rate of 3.14% compared to a conventional 30-year fixed-rate mortgage at 3.15%. It is, however, generally more expensive to refinance a jumbo loan due to high closing costs.

A jumbo mortgage calculator contains the following variables to calculate interest payable and monthly repayment:

Sample Calculation

The requirements for a jumbo loan are, to a greater extent, similar to a conventional conforming mortgage. However, there are extra eligibility requirements that are over and above a conventional mortgage. The extra requirements may make it harder to qualify for a jumbo loan.

The qualifications for a jumbo loan are stringent as all factors are considered carefully. Such loans are also manually underwritten, which means a loan officer carefully analyzes the borrower’s bank statements, credit reports, and assets to unearth any questionable past activities, such as bankruptcy, foreclosure, or insolvency.

Lenders generally require a high credit score for jumbo loans. Even good credit scores on conventional mortgage loans may not be enough to qualify for jumbo loans. The credit score contains a borrower’s credit history showing proof of past ability to make timely payments.

Bankruptcy filings should be older to limit the damage to the credit score, but a history of foreclosure disqualifies a borrower.

An average credit score can be offset by a low debt to income ratio. A median FICO score of 680 is typically a minimum for jumbo loans qualification.

Although all mortgages require a down payment, jumbo loans typically require a large down payment of at least 20%.

Large cash reserves are normally required for jumbo loans to safeguard lenders from possible mortgage defaults. Cash reserves normally need to cover between six months to twelve months of mortgage payments.

Borrowers must furnish the lender with bank statements to prove the existence of cash flow reserves. Lenders can also consider up to 70% of a borrower’s retirement account towards cash reserve requirements.

Borrowers should be in a high-income bracket and demonstrate consistent, predictable income to qualify for jumbo loans. It makes jumbo loans a preserve for the rich or HENRYs, i.e., high earners, not rich yet, which are individuals or families earning between $250,000 and $500,000 annually.

The HENRYs income segment enjoys significant discretionary income able to service the high monthly repayments of jumbo loans.

Debt to income ratio (DTI) is a ratio of a borrower’s total debt relative to their monthly income. Jumbo loan lenders consider a borrower’s DTI very important. DTI shows the borrower’s capacity to meet all monthly payments, including the jumbo loan.

Borrowers can have other debts outstanding that include credit card bills and auto loans. The quantity of other debts can affect the borrower’s ability to repay the jumbo mortgage. The FHFA recommends a DTI under 43%, but jumbo loan lenders may require an even lower DTI.

The loan to value ratio (LTV) is a measure of the loan amount relative to the property’s value. LTV is calculated by dividing the loan amount by the property’s appraised value or purchase price, whichever is lower.

The LTV requirement for a jumbo loan is stricter than for a conforming loan with rates of 80% or lower. The lower the LTV, the better as it provides more security. A higher down payment can also reduce the LTV favorably.

Jumbo loan applications require additional documentation to show proof of income and ability to meet jumbo mortgage down payment, closing costs, and reserves. The extra documentation includes assets, tax returns, P & L statements for business applications, proof of additional income, and other qualifications. A property appraisal report is also needed to ascertain the value of the property.

The requirements to refinance a jumbo loan can be quite tough and strenuous. There are also extensive demands for documentation. Most lenders are reluctant to refinance jumbo loans because of the risk involved in high-value loans, as well as the fact that some jumbo loans may not have mortgage insurance.

Here is a brief overview of what it takes to apply for a jumbo mortgage loan refinancing facility.

CFI is the official provider of the global Certified Banking & Credit Analyst (CBCA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: