Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A measure used by financial institutions to help estimate potential credit losses in order to calculate a loan’s projected profitability

LGD (Loss Given Default) is a lender’s (creditor) ‘s projected loss in the event that a borrower triggers an event of default.

LGD is a measure used by financial institutions and other private, non-bank lenders to help calculate the projected profitability of a loan (often referred to as a credit facility – which may include operating credit, term loans, commercial mortgages, capital leases, etc.).

LGD is most commonly expressed as a percentage; however, it can also be expressed as an absolute dollar figure. It is tied very closely to any collateral security underpinning the credit exposure. In fact, in its most literal sense, LGD is the inverse of an asset’s recovery rate.

When a lender extends credit to a borrower, there are three ways the creditor can get its principal back. We’ll work with a commercial borrower for our illustration.

These are (in order of preference):

1. Repayment. Note – there are two repayment scenarios:

If the borrower triggered an event of default, however, and could not pay back (or refinance) the exposure, then the lender would seek to:

2. Liquidate some (or all) of the borrowing entity’s assets in order to recover as much of its principal outstanding as possible.

If liquidation of the borrower’s assets was unable to cover the lender’s total exposure (at the time of default), then there would remain what’s called “residual” exposure outstanding. The lender would try to recover this “residual” by way of:

3. Some form of alternative “recourse,” usually a personal or corporate guarantee from the owner operator(s) or from a parent company (or otherwise related entity), respectively. This is assuming that the lender and the borrower had previously agreed to some form of alternative recourse.

Since scenario #2 is a very realistic possible outcome in any commercial relationship, lenders go to great lengths to project what their anticipated losses would be if a liquidation scenario arose.

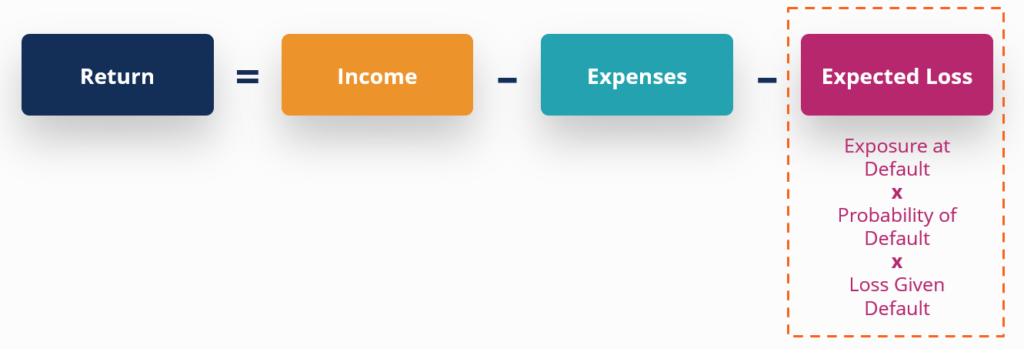

While this is a bit of an oversimplification, at a high level, a lender’s returns are calculated as income less expenses and less expected (credit) losses.

Income includes interest income, as well as closing or origination fees (and other fees), charged to a borrower. Expenses include any disbursement-related costs, as well as the lender’s interest expense (after all, lenders use leverage in their capital structure, too).

But it’s the expected loss bucket that’s most relevant here. Expected loss is calculated as the credit exposure (at default), multiplied by the borrower’s probability of default, multiplied by the loss given default (LGD).

Let’s assign some numbers to illustrate. Assume:

The expected loss in this example (expressed in dollars) would be $5,000. That’s:

$1,000,000 x 0.02 x 0.25 = $5,000

LGD is calculated as 1 minus the anticipated recovery rate of an asset (or assets). The recovery rate (expressed as a percentage) is the proportion of an asset’s value that a lender can realistically expect to get back if a client were to trigger an event of default that eventually leads the creditor to a liquidation scenario.

If the expected recovery rate for an asset (or an asset class) is 75% (0.75), then the LGD would be (1 – 0.75), which equals 25%.

A higher anticipated recovery rate equals a lower LGD.

Let’s consider two example loans/borrowers:

The proceeds of loan #1 are secured by an asset that has an active secondary market, and its value is (relatively) easy to ascertain by way of a third-party appraisal. The proceeds of loan #2 are, for all intents and purposes, unsecured by any tangible underlying physical asset(s).

It would be reasonable to assume that, should borrower #1 trigger an event of default on the commercial mortgage, the lender would recover a reasonable proportion of its principal by foreclosing on the property and auctioning it off (if necessary). This is particularly true if the loan-to-value (LTV) is low.

It would be equally reasonable to assume that the lender in scenario #2 would have a much more difficult time recovering its full loan exposure in a liquidation event.

Most large financial institutions will use historical default/liquidation data to calculate an expected recovery rate on the various assets the firm is willing to finance using balance sheet lending.

Alternatively, smaller firms may employ a risk rating or risk management organization that aggregates data (like Moody’s or Fitch) to determine what LGD rates should be for various asset classes.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Loss Given Default (LGD). To keep learning and advancing your career, the following resources will be helpful: