Fisher Effect

The relationship between nominal interest rates and real interest rates and inflation expectations

What is the Fisher Effect?

The Fisher Effect refers to the relationship between nominal interest rates, real interest rates, and inflation expectations. The relationship was first described by American economist Irving Fisher in 1930.

The relationship is described by the following equation:

(1+i) = (1+r) * (1+π)

Where:

- i = Nominal Interest Rate

- r = Real Interest Rate

- π = Expected Inflation Rate

The Fisher Effect is an important relationship in macroeconomics. It describes the causal relationship between the nominal interest rate and inflation. It states that an increase in nominal rates leads to a decrease in inflation. The key assumption is that the real interest rate remains constant or changes by a small amount.

Applications

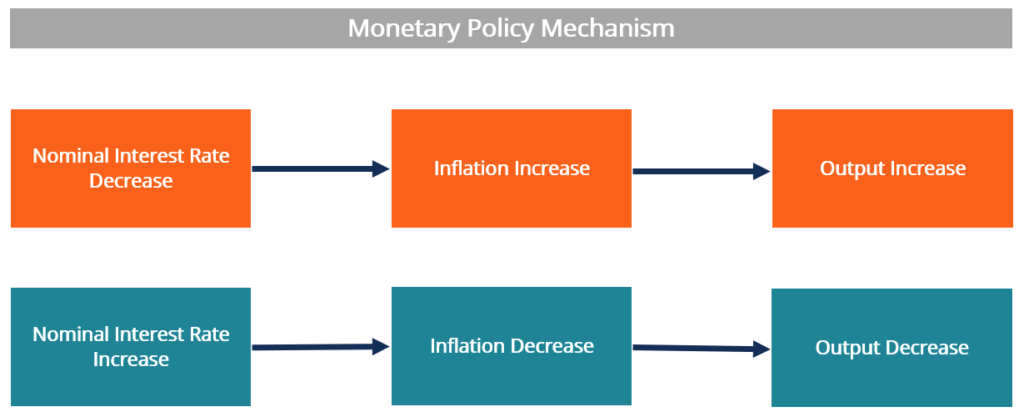

Monetary Policy

The central bank in an economy is often tasked with keeping inflation in a tight range. The practice is to prevent the economy from overheating and inflation spiraling upwards in times of expansion. It is also important to have a small amount of inflation to prevent a deflation spiral, which pushes an economy into a depression in times of recession.

The main tool available to most central banks is their ability to set the nominal interest rate. They achieve this through many mechanisms like open market operations, changing reserve ratios, etc.

Given a fixed interest rate, we can see that an increase in the nominal interest rate will bring down inflation expectations and prevent overheating. Similarly, a decrease in the nominal interest rate can increase inflation expectations, and spur more investment, thereby avoiding a deflation spiral.

The following figure illustrates how monetary policy acts through the Fisher Effect:

Measuring Portfolio Returns

One of the major objectives of investing is to generate enough returns to outpace inflation. It is necessary because if the returns are lower than inflation, the purchasing power of the total wealth of the investor will be lower than when they started investing.

For example, an investment in the sovereign debt of a country is considered risk-free and offers a yield of 2% over one year. Assume that the inflation in that country is 3% per year, and a business needs to purchase goods that are worth $100 today. They invest their cash in government debt, which means they get $102 in a year.

Since the inflation rate was 3%, the goods are now worth $103. Hence, there is a shortfall of $1 when the business needs to make the purchase.

The example above illustrates an important point that ignoring the impact of inflation can create liquidity issues in the future. The Fisher Effect is important because it helps the investor calculate the real rate of return on their investment.

The Fisher equation can also be used to determine the required nominal rate of return that will help the investor achieve their goals.

Currency Markets

In currency markets, the Fisher Effect is called the International Fisher Effect (IFE). It describes the relationship between the nominal interest rates in two countries and the spot exchange rate for their currencies.

Hence, given the nominal interest rates in the two countries and the spot exchange rate today, we can calculate the future spot rate. Use the following formula to calculate the future spot rate:

Futures Price = Spot Price * (1 + rD) / (1 + rF)

Where:

- rD = Nominal Interest Rate in the Domestic Currency

- rF = Nominal Interest Rate in the Foreign Currency

It is evident from the equation that if the domestic rate is lower than the foreign rate, the domestic currency is expected to depreciate relative to the foreign currency. It is the International Fisher Effect.

Evidence of the Fisher Effect

As discussed above, the Fisher Effect is important in economic policymaking as it applies to monetary policy. As a result, there are many empirical studies conducted by economists who try to determine if the Fisher Effect exists and to measure it.

Mishkin 1991, 1995

A paper written by Fredric Mishkin of Princeton University found that the Fisher Effect exists in the long term, but in the short term, the paper found there was no relationship between inflation and nominal interest rate. Another paper by the same author conducts an empirical analysis of the Fisher Effect in Australia and comes to the same conclusion.

Jaffe and Mandelker, 1976

Jaffe and Mandelker studied the relationship between inflation and returns on risky assets. More specifically, they studied the relationship between stock market returns and inflation. Most studies of the Fisher Effect study the relationship between the risk-free rate (or nominal interest rate) and inflation.

Their study found no evidence for the existence of the Fisher Effect in stock market returns. In fact, it found that increased inflation expectation is negatively correlated with market returns. The finding runs counter the relationship described by the Fisher Effect.

Uribe, 2018

One of the more recent investigations into the Fisher Effect finds that it holds true for temporary changes in the nominal interest rate, but in case of a permanent increase in the nominal interest rate, the opposite holds true, and an increase in the nominal rate leads to inflation.

Note that the above is the exact opposite of the mechanism described in the monetary policy section. The author calls the mechanism the neo-Fisher Effect. It is a new theoretical framework in response to the unconventional monetary policy being used since the Great Financial Crisis (GFC) of 2008.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: