Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Compares the additional benefits derived from an activity and the extra cost incurred by the same activity

Marginal analysis compares the additional benefits derived from an activity and the extra cost incurred by the same activity. It serves as a decision-making tool in projecting the maximum potential profits for the company by comparing the costs and benefits of the activity.

The term “marginal” is used by economists to refer to the changes resulting from one unit change in activity. It is concerned with the incremental cost and benefit stemming from a change in production.

In microeconomics, most decisions usually evaluate whether the benefit of a particular activity or action is greater than the cost. Marginal analysis comes in handy when making a decision with a causal relationship involving two variables. It explains the potential effect of some conditional changes on a company as a whole.

By examining the associated costs and potential benefits, marginal analysis provides useful information that is likely to prompt price or production change decisions.

Marginal analysis also looks at the conditions under which the company may continue with the same cost of producing an individual unit or output in the face of expected or actual changes. Here, the dominating principle is the adjustment to change. The idea is that it is worthwhile for a company to continue investing until the marginal revenue from each extra unit is equal to the marginal cost of producing it.

Marginal analysis may also be applied in a situation where an investor is faced with two potential investments but with the resources to only invest in one. The investor can use marginal analysis to compare the costs and the benefits of both investments to determine the option with the highest income potential.

The following are the two prevalent uses of marginal analysis:

Marginal analysis can be used by managers to create controlled experiments based on the observed changes of particular variables. For example, the tool can be used to evaluate the impact of increasing production at a given percentage on cost and revenues.

A benefit is accrued when the marginal cost is reduced or the increased revenues cover and spill over total production costs. If the experiment yields a positive result, incremental steps are taken until the result yields a negative outcome. This may be the scenario when the market cannot take the additional production units, leading to excessive overheads. At that stage, a company with the capacity to expand will opt to increase its market reach.

Managers regularly find themselves in situations where they are required to make a choice among available options. For example, suppose a company has a single job opening, and they have the choice of hiring a junior administrator or a marketing manager.

Marginal analysis may indicate that the company has resources to grow and that the market is saturated. As a result, hiring a marketing manager will yield higher returns than an administrator.

There are two rules for profit maximization that make marginal analysis a key component in the microeconomic analysis of decisions. They are:

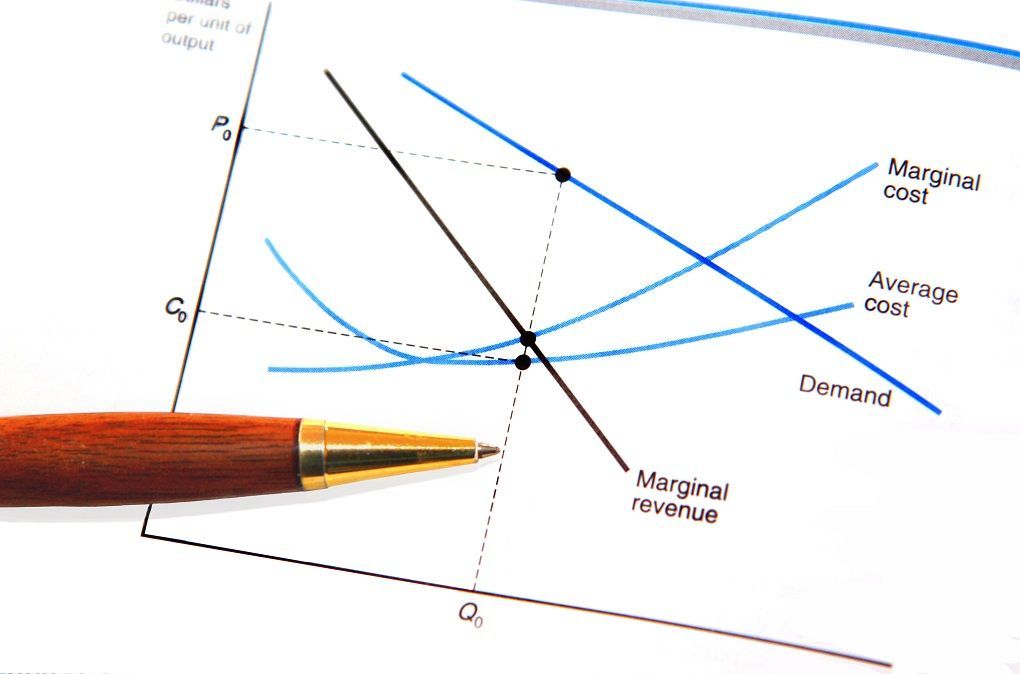

The first rule posits that the activity must be carried out until its marginal cost is equal to its marginal revenue. The marginal profit at such a point is zero. Typically, profit can be increased by expanding the activity if the marginal revenue exceeds marginal cost.

Marginal benefit is a measure of how the value of cost changes from the consumer side of the equation, while the marginal cost is a measure of how the value of cost changes from the producer side of the equation. The equilibrium rule implies that units will be purchased up to the point of equilibrium, where the marginal revenue of a unit is equal to the marginal cost of that unit.

The second rule of profit maximization using marginal analysis states that an activity should be performed until it yields the same marginal return for every unit of effort. The rule is premised on the idea that a company producing multiple products should allocate a factor between two production activities such that each provides an equal marginal profit per unit.

If it is not achieved, profit could be realized by allocating more input to the activity with the highest marginal profit and less to the other activity.

One of the criticisms against marginal analysis is that marginal data, by its nature, is usually hypothetical and cannot provide the true picture of marginal cost and output when making a decision and substituting goods. It therefore sometimes falls short of making the best decision, given that most decisions are made based on average data.

Another limitation of marginal analysis is that economic actors make decisions based on projected results rather than actual results. If the projected income is not realized as predicted, the marginal analysis will prove to be worthless.

For example, a company may decide to start a new production line based on a marginal analysis projection that the revenue will exceed costs to establish the production line. If the new production line does not meet the expected marginal costs and operates at a loss, it means that the marginal analysis used the wrong assumptions.

Marginal analysis may also apply to the effects of small changes and the opportunity cost concept. In the former, marginal analysis relates to observed changes with total outputs. Evaluating such changes can help determine the standard production rate.

It is common in employment scenarios, where the Human Resource (HR) manager makes a hiring decision. Suppose a company’s budget allows the recruitment of one employee. With marginal analysis, the HR can know whether an additional employee in the production department provides a net marginal benefit.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: