Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The number of units of one product that can be increased by reducing the quantity of another product

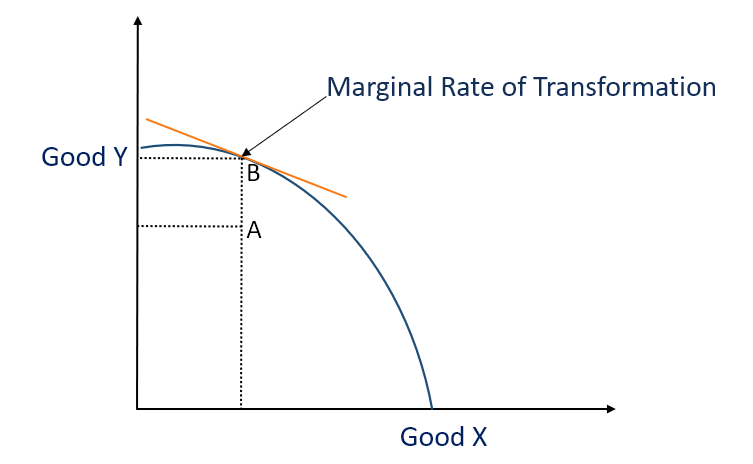

The marginal rate of transformation is the number of units of one product that can be increased by reducing the quantity of another product. It is also considered as the opportunity cost for generating an extra unit of output. It examines the number of good X that will be foregone to produce an additional unit of good Y while keeping the factors of production constant.

It can be calculated by dividing the extra units of output by the quantity freed up by reducing the production of another product. However, factors of production and technology must remain constant.

The marginal rate of transformation helps the management analyze the opportunity costs of producing one additional unit of output. Although it is possible to compute the marginal rate of transformation for a variety of products, rates differ according to the types of products compared. Increasing production of one item means decreasing the production of the other since resources are diverted to creating the new unit.

Opportunity cost escalates as more of the other good is produced. The trade-off between the products is examined by the marginal rate of transformation. For example, if producing one less hotdog would free up enough resources to produce three more burgers, then the rate of transformation is 3 to 1 at the production margin.

The marginal rate of transformation can be used by businesses to determine how many more units of a good can be generated if the production of another item is decreased. Generally, it outlines the relationship between items by describing the number of units of one good that is equivalent to the other unit of production.

It changes with the difference brought by the production of an extra unit and a decrease in the production of the other unit. However, for the company to choose perfect substitute items, the marginal rate of transformation must remain constant. This is because the marginal rate of transformation focuses on the supply of a product.

Product possibility frontier describes the maximum output that can be generated, with the factors of production and technology held constant. Generally, the opportunity cost increases as more of the extra items are produced.

A business operating on the efficient product possibility frontier may be unable to produce more of one item without reducing the production of the other good. Therefore, production of one unit will be halted, and the resources of production will be directed to produce the other unit since more of one item can only be generated by producing less of the other.

A company working on the inefficient product possibility frontier will not decrease the production of one item to produce the other. Instead, the management will reallocate resources to generate more of both units. The company may also make use of unutilized resources to produce more of both units.

The opportunity cost is the benefit or cost incurred after choosing to produce an alternative unit. If the opportunity cost is constant, production resources can be substituted for each unit without any added costs. However, if there is no increase in production resources, raising the production of the first unit will force the company to lower the production of the second unit. Opportunity cost can be measured by the number of units of the forgone good for one or more units of the first unit.

The following are types of opportunity costs:

The marginal rate of transformation requires frequent recalculation since the rate is not always constant. If the MRT is indifferent to the marginal rate of substitution, the products may be efficiently distributed.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA®) certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: