Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

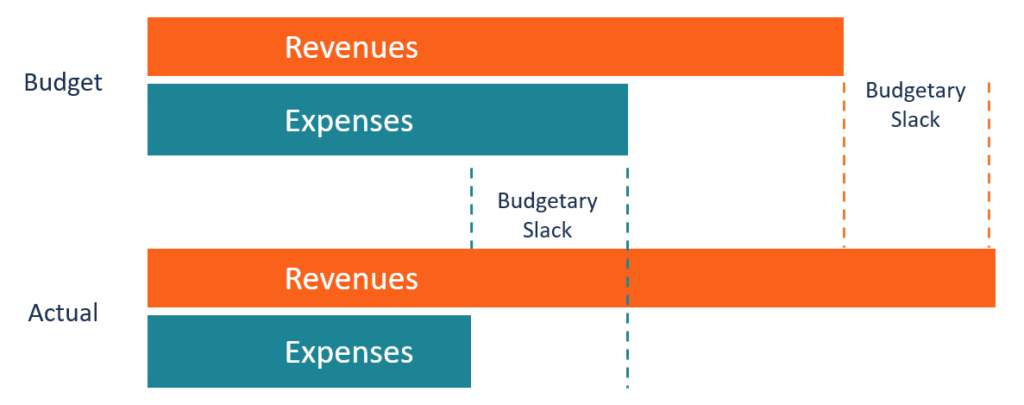

The practice of overestimating the expenses and/or underestimating the projected revenues in budget preparations

Budgetary slack is the practice of overestimating the expenses and/or underestimating the projected revenues when preparing a budget statement for the next financial period. It is a cushion created by management or lower-level managers to prepare budget estimates that will not be hard to achieve.

In other instances, budgetary slack may be a result of the management adding unverified numbers, especially in highly competitive industries where changes are common. A true budget statement must be honest; it should reflect actual anticipated revenues and expenses.

The following are some of the common causes of budgetary slack when preparing an annual budget for the company:

The managers of a company may face a lot of uncertainty over the results expected in a future period. For example, when the company is introducing a new product line, the managers lack actual data on the kind of results to expect.

As a result, they will be conservative when setting up the budget for the coming financial year to avoid promising beyond what they can achieve. Budgetary slack may occur when the managers underestimate the expected revenues to remain in a range that is easy to achieve for a new product line.

Information asymmetry occurs when one party possesses more information about the subject than the other. In such a case, departmental-level managers may be able to access private information about resource requirements, employee productivity, and expenditures which the senior management may not be privy to.

The lower-level managers may take advantage of the information asymmetry to advance their self-interest without the knowledge of the top management. They can set easy-to-achieve revenue targets so that they can be seen to be working hard by the management, even when they are guaranteed to outperform the previous year’s results.

In organizations where employee awards and payoffs are dependent on budget attainment, lower-level managers may create budget slacks to make the target easy to achieve. The subordinate managers are often under pressure from top management to make sure that the set goals are achieved, which means that they can influence the process to work in their favor.

As the managers perform supervisory roles, they know what is achievable and what resources are required. They would, therefore, present a high budget for expenses while low-balling the expected revenue target at a level that is easily attainable. This would make it easy for them to beat the set targets in every period and enjoy the promised rewards, salary hikes, and job promotions.

The occurrence of budgetary slacks within an organization can result in declining productivity and performance because the employees work towards attaining goals that are within their capability. Implementing the measures below can help reduce budget slacks in an organization:

When too many managers are allowed to contribute to the budget model, they may allow too much slack as a way of downplaying their company’s expectations. This will allow too much wastage since the employees lack the motivation to be productive when the targets are easily achievable.

Limiting the number of managers who prepare the budgets to a few aggressive managers can help reduce the slack. The managers will set the expectations high to create a challenge for the employees to move out of their comfort zone and work towards attaining those goals. If the employees are unable to achieve that target, they will be motivated to attempt the challenge again in the next financial period.

Most organizations use the budget as a tool to measure how well the employees performed in a given period. Employees who are found to have achieved their targets are rewarded with bonuses and payoffs, whereas those who are unable to achieve the targets are reprimanded.

However, this encourages employees to create a budgetary slack that allows them to easily achieve targets so that they can be rewarded in every financial period. Removing any link between performance, bonuses, and the budget can reduce the motivation to cheat the system and benefit from a performance-based reward.

A budgeting slack comes with the following disadvantages:

When the subordinate managers continually create easy targets, the business will be seen as underperforming in a highly competitive market. Even when the business is on track to hit new highs, the managers will use up the additional revenues left in the budget because of the budgetary slack made to the budget.

Such a practice will portray the business as struggling and may force high-performing employees to jump ship to stronger competitors. Artificially slowing down the growth may also adversely affect the company’s performance. Shareholders will start casting doubt on the company’s ability to continue generating revenues.

When the budget estimates for the next financial year show that the revenues are lower than what the top management projected, the company will cut the expense budget for important functions such as marketing and advertising, research and development, production, and administrative expenses. Slashing the expense budgets will affect the long-term viability of the business.

For example, reducing the expense budget for the marketing department will limit the company’s potential to get new customers and even retain existing customers, which is critical to the ongoing profitability of the business.

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.