Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

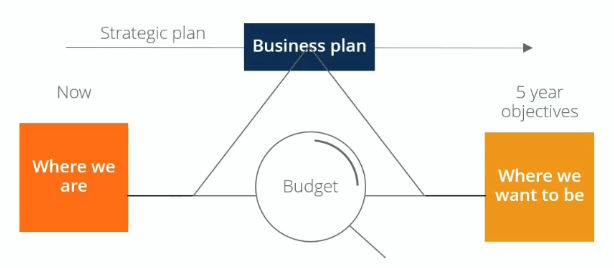

The tactical implementation of a business plan

Budgeting is the tactical implementation of a business plan. To achieve the goals in a business’s strategic plan, we need a detailed descriptive roadmap of the business plan that sets measures and indicators of performance. We can then make changes along the way to ensure that we arrive at the desired goals.

There are four dimensions to consider when translating high-level strategy, such as mission, vision, and goals, into budgets.

Budgeting is a critical process for any business in several ways.

The process prompts managers to consider how conditions may change and the steps they need to take, while also helping them understand how to address problems when they arise.

Budgeting encourages managers to build relationships with the other parts of the operation and understand how the various departments and teams interact with each other and how they all support the overall organization.

Communicating plans to managers is an important social aspect of the process, which ensures that everyone gets a clear understanding of how they support the organization. During budget reviews, using a structured communication framework can help ensure financial insights are clearly understood by leadership.

It encourages communication of individual goals, plans, and initiatives, which all roll up together to support the growth of the business. It also ensures appropriate individuals are made accountable for implementing the budget.

Budgeting gets managers to focus on participation in the budget process. It provides a challenge or target for individuals and managers by linking their compensation and performance relative to the budget.

Managers can compare actual spending with the budget to control financial activities.

Budgeting provides a means of informing managers of how well they are performing in meeting targets they have set.

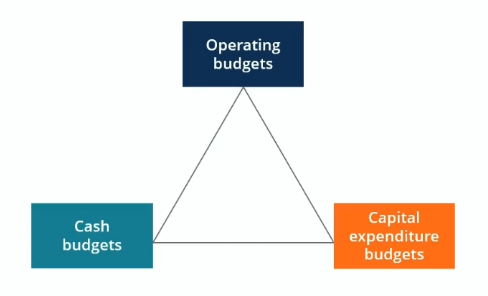

A robust budget framework is built around a master budget consisting of operating budgets, capital expenditure budgets, and cash budgets. The combined budgets generate a budgeted income statement, balance sheet, and cash flow statement.

Revenues and associated expenses in day-to-day operations are budgeted in detail and are divided into major categories such as revenues, salaries, benefits, and non-salary expenses.

Capital budgets are typically requests for purchases of large assets such as property, equipment, or IT systems that create major demands on an organization’s cash flow. The purposes of capital budgets are to allocate funds, control risks in decision-making, and set priorities.

Cash budgets tie the other two budgets together and take into account the timing of payments and the timing of receipt of cash from revenues. Cash budgets help management track and manage the company’s cash flow effectively by assessing whether additional capital is required, whether the company needs to raise money, or if there is excess capital.

The budgeting process for most large companies usually begins four to six months before the start of the financial year, while some may take an entire fiscal year to complete. Most organizations set budgets and conduct variance analysis monthly.

From the initial planning stage, the company goes through a series of steps to implement the budget. Common processes include communication within executive management, establishing objectives and targets, developing a detailed budget, compilation and revision of budget model, budget committee review, and approval.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.