Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Measures the ability of the bank to absorb losses

The Capital Adequacy Ratio sets standards for banks by looking at a bank’s ability to pay liabilities and respond to credit risks and operational risks. A bank with a good CAR has sufficient capital to absorb potential losses. Thus, it has less risk of becoming insolvent and losing depositors’ money. After the Global Financial Crisis in 2008, the Bank for International Settlements (BIS) began imposing stricter capital adequacy requirements to protect depositors.

As shown below, the CAR formula is:

CAR = (Tier 1 Capital + Tier 2 Capital) / Risk-Weighted Assets

The Bank of International Settlements separates capital into Tier 1 and Tier 2 based on the function and quality of the capital. Tier 1 capital is the primary way to measure a bank’s financial health. It includes shareholder’s equity and retained earnings, which are disclosed on financial statements.

As it is the core capital held in reserves, Tier 1 capital is capable of absorbing losses without impacting business operations. On the other hand, Tier 2 capital includes revalued reserves, undisclosed reserves, and hybrid securities. Since this type of capital has lower quality, is less liquid, and is more difficult to measure, it is known as supplementary capital.

The bottom half of the equation is risk-weighted assets. Risk-weighted assets are the sum of a bank’s assets, weighted by risk. Banks usually have different classes of assets, such as cash, debentures, and bonds, and each class of asset is associated with a different level of risk. Risk weighting is decided based on the likelihood of an asset to decrease in value.

Asset classes that are safe, such as government debt, have a risk weighting close to 0%. Other assets backed by little or no collateral, such as a debenture, have a higher risk weighting. This is because there is a higher likelihood the bank may not be able to collect the loan. Different risk weighting can also be applied to the same asset class. For example, if a bank has lent money to three different companies, the loans can have different risk weighting based on the ability of each company to pay back its loan.

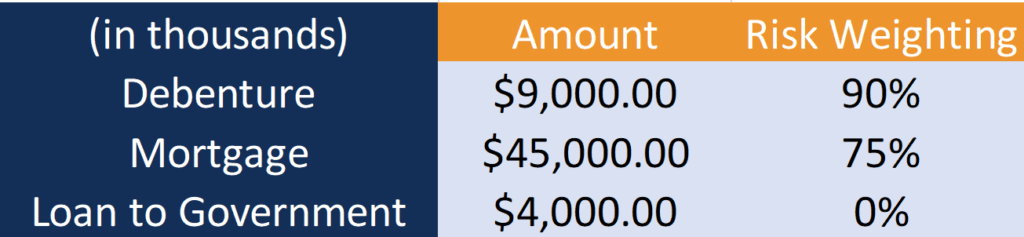

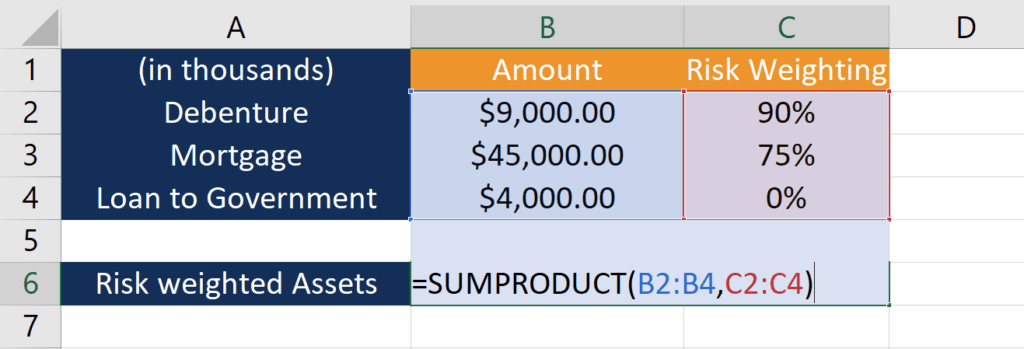

Let us look at an example of Bank A. Below is the information of Bank A’s Tier 1 and 2 Capital, and the risks associated with their assets.

Bank A has three types of assets: Debenture, Mortgage, and Loan to the Government. To calculate the risk-weighted assets, the first step is to multiply the amount of each asset by the corresponding risk weighting:

As the loan to the government carries no risk, it contributes $0 to the risk-weighted assets.

The second step is to add the risk-weighted assets to arrive at the total:

The calculation can be easily done on Excel using the SUMPRODUCT function.

To learn more about Excel functions, take a look at CFI’s free Excel course.

The Capital Adequacy Ratio of Bank A is as follows :

Where:

As Bank A has a CAR of 10%, it has enough capital to cushion potential losses and protect depositors’ money.

Under Basel III, all banks are required to have a Capital Adequacy Ratio of at least 8%. Since Tier 1 Capital is more important, banks are also required to have a minimum amount of this type of capital. Under Basel III, Tier 1 Capital divided by Risk-Weighted Assets needs to be at least 6%.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Capital Adequacy Ratio. To keep learning and advancing your career, the following CFI resources will be helpful: