Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A dividend issued by a business as part of its liquidation process

A liquidating dividend is a dividend issued by a business as part of its liquidation process. Liquidation is the process by which a company ends its business activities and exits the market. Liquidation can be voluntary or involuntary (forced).

A liquidating dividend is also known as a liquidating distribution or a terminal distribution, as it involves the distribution of semi-liquid and liquid assets among the shareholders of the company. When the operators of a business believe they can no longer sustain operations, they wind down the business and return the assets of the business to shareholders via dividend payments.

A dividend is a reward that shareholders receive for investing in a company. A company can distribute dividends in many different ways, such as cash payments or additional stock. The board of directors of a company decides how much of a dividend the company will pay out and follow a certain dividend policy when distributing the profits.

Many investors find dividends attractive because they provide a regular stream of income. Usually, dividends are paid out quarterly (in line with the company’s earnings), but in certain instances, the company may choose to pay out a special or irregular dividend.

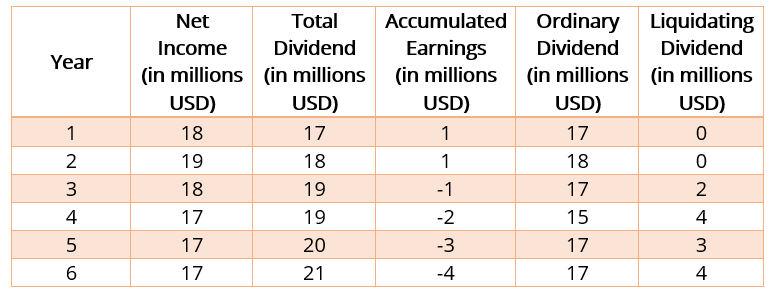

Company X purchases a 20% stake in Company Y for $200 million. A 20% transfer of ownership does not constitute a significant change in influence or control. Consider the following information about Company Y’s stock. The table below shows the Company Y’s net income, total dividends, accumulated earnings, ordinary dividend, and liquidating dividend.

During Year 1 and Year 2, the net income of Company Y was $20 million and $22 million, respectively. During the same period, Company Y paid out $17 million and $18 million as dividends. The dividends are paid out of Company Y’s income and constitute income for Company X.

Company X Balance Sheet for Year 1

| Account | Debit | Credit |

| Cash | $17 million | |

| Dividend Income | $17 million | |

Company X Balance Sheet for Year 2

| Account | Debit | Credit |

| Cash | $18 million | |

| Dividend Income | $18 million | |

During Years 3, 4,5, and 6, the dividends declared exceed net income. The dividend paid out from the year’s net income or the accumulated income from previous years is considered an ordinary dividend. The rest is considered a liquidating dividend.

Company X Balance Sheet for Year 3

| Account | Debit | Credit |

| Cash | $19 million | |

| Dividend Income | $17 million | |

| Investment in Company Y | $2 million | |

Company X Balance Sheet for Year 4

| Account | Debit | Credit |

| Cash | $19 million | |

| Dividend Income | $15 million | |

| Investment in Company Y | $4 million | |

Company X Balance Sheet for Year 5

| Account | Debit | Credit |

| Cash | $20 million | |

| Dividend Income | $17 million | |

| Investment in Company Y | $3 million | |

Company X Balance Sheet for Year 6

| Account | Debit | Credit |

| Cash | $21 million | |

| Dividend Income | $17 million | |

| Investment in Company Y | $4 million | |

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: