Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A specific term in a credit agreement that requires or restricts certain circumstances or behaviors by a borrower

Loan covenants are a series of small, independent agreements made between a debtor (borrower) and a creditor (lender). Loan covenants expressly outline behaviors that a borrower must – or must not – engage in.

When a debtor borrows money from a creditor, the loan terms are expressly outlined in a legal document called a credit agreement or a loan contract. The specific loan terms you may find in a credit agreement include the loan amount, the interest rate, the repayment schedule, and (usually) a lengthy list of loan covenants. When a borrower violates one of these loan covenants (often called a covenant breach), it is considered an event of technical default.

Loan covenants may be categorized in a variety of ways. They include:

Standard loan covenants are generally outlined in a boilerplate format, meaning they’re standard for all borrowers.

Standard loan covenants outline circumstances or behaviors that are often taken for granted but must still be stipulated in a credit agreement for the legal enforceability of the contract. Examples include:

Non-standard loan covenants are designed based on particular characteristics or risks related to a credit request or a borrower.

Non-standard loan covenants are typical with commercial lending since business operations and financial results are more complex than personal lending. Examples include:

Positive loan covenants (often called affirmative covenants) outline what a borrower must do. These are typically worded as:

Negative loan covenants stipulate actions that the borrower must NOT do. Negative covenants are usually worded as:

Both standard and non-standard loan covenants can be worded as either as a positive or as a negative.

Financial loan covenants are explicitly related to a borrower’s financial metrics. They should be designed based on specific risks inherent in the credit structure or particular risks the borrower presents. Examples of financial covenants are:

Non-financial covenants include a wide variety of expected behaviors or circumstances that are not specific to the borrower’s financial measures. Examples include:

Creditors extend loans to generate interest income. Part of the calculation is to ensure the full repayment of principal, so to the extent that it’s possible, a lender will always seek to exert any influence on that borrower to help ensure financial well-being. This is where loan covenants come in.

By expressly requiring or restricting specific actions or circumstances, loan covenants serve two primary purposes. The first is to help align incentives between the borrower and the lender; the second is to mitigate transaction (or borrower) specific risks.

Both of these processes improve the likelihood of full loan repayment.

An example in commercial lending is where a management team may wish to distribute a large proportion of company earnings to shareholders through dividend payments. The lender would rather see that cash retained within the corporation to provide a cash buffer or, perhaps, to repay some of its outstanding credit.

This misalignment of incentives can be managed by limiting or restricting dividends or by requiring that financial covenant calculations be net of dividend payments.

The most basic illustration of this concept is a loan agreement where strict repayment dates are not expressly outlined in the credit agreement. What incentive would a borrower have to make payments on time?

The concept of aligning incentives is a crucial one.

Loan covenants are also used to mitigate specific risks. Think about a borrower taking on high leverage (or gearing) to make an acquisition. It’s in the lender’s best interest to have that borrower deleverage as quickly as possible to bring its leverage ratios back to long-term expectations or industry norms.

Loan covenants should only be employed when specific incentives need better alignment or when mitigating a particular risk. Loan covenants that are too restrictive can have ramifications for the lender. These include, but are not limited to:

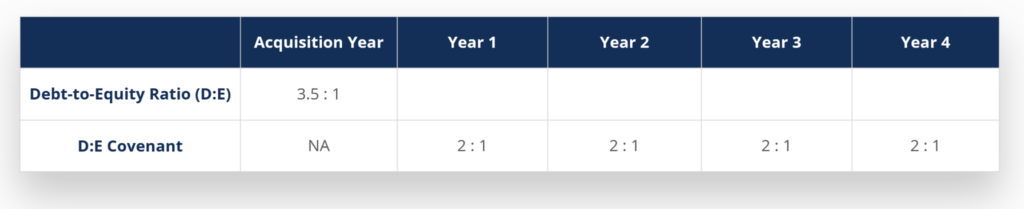

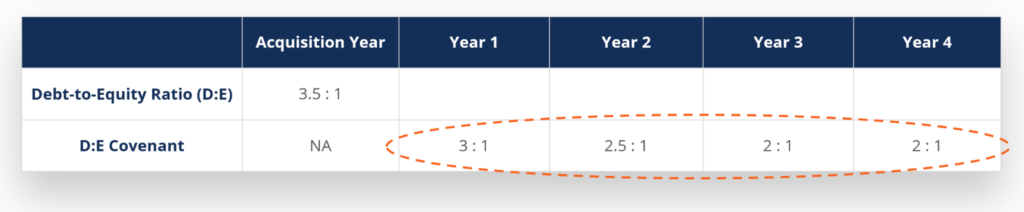

This is when a lender forces a covenant on a borrower that is unrealistic or not likely to be attainable. Consider the earlier example of a company that borrows heavily to acquire another company – it’s normal for the debt-to-equity (D:E) ratio to balloon in the acquisition year.

Let’s say the ratio is 3.5 : 1 in the acquisition year, but the lender generally prefers 2 :1 or below. Many lenders may institute a going-forward covenant of 2 : 1, as illustrated below:

However, it’s unlikely the borrower can realistically accomplish this by the first fiscal year-end post-acquisition. An alternative might be the use of a stepped covenant, like below:

Stepping covenants is a more prudent strategy to align incentives and to de-risk the relationship without the risk of setting the borrower up for almost inevitable failure. Using steps like this allows the borrower to gradually return to a normal range without undue stress on company management.

Another risk of overusing covenants is that someone from the middle office at the financial institution must track and action each covenant at the end of each reporting period. This administrative burden can increase headcount and cause potential compliance issues since each breached covenant must be documented and overseen appropriately.

All other factors being equal, most borrowers prefer fewer and less restrictive loan covenants. If a financial institution consistently puts proposals in front of clients and prospects that overuse loan covenants (relative to competitors), they may lose some opportunities.

When a loan covenant is violated, it’s often referred to as a covenant breach.

Since loan covenants are part of the credit agreement between a borrower and a lender, a covenant breach is considered an event of debt default. These can be financial defaults (like a delinquent payment) or technical defaults (like late reporting).

All covenant breaches must be reviewed by a risk manager and documented in writing by the lender since they violate the credit agreement. But while all loan covenants are important and legally binding, not all covenant breaches are created equally.

For example, late financial reporting may be an issue with the client’s accountant that could be resolved within a few days or a week. Similarly, a client that must adhere to a DSC covenant of 1.25 : 1 (but that reports a DSC ratio of 1.23 : 1) is unlikely to receive an accelerated repayment notice from the bank.

Fraudulent financial results presented to a lender, however, would be considered a severe technical default that would likely have immediate and serious legal consequences for the borrower.

Thank you for reading CFI’s guide to Loan Covenant. To keep advancing your career, the additional CFI resources below will be useful: