Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The measures of money stock in a country

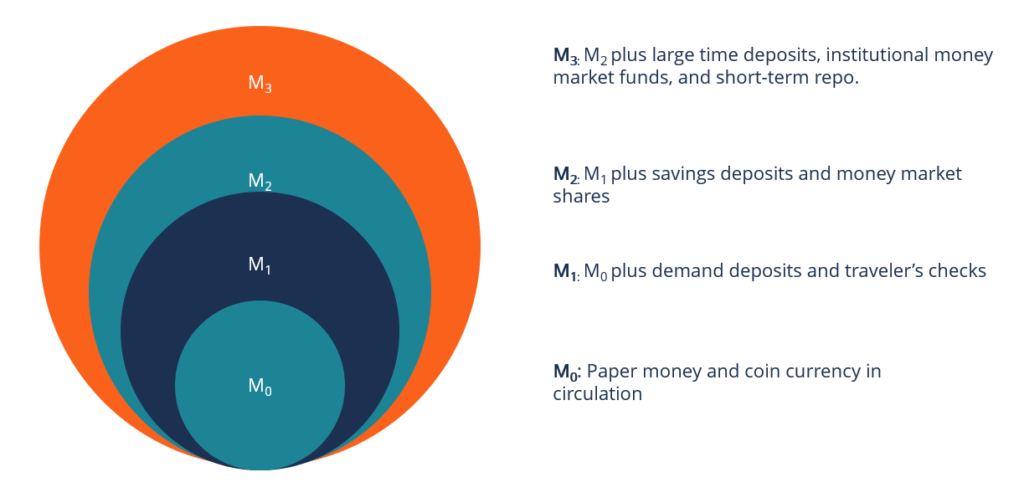

Monetary aggregates are the measures of money stock in a country. Central banks measure money aggregates and present them in the form of end-of-month national currency stock series. In the U.S., monetary aggregates are conventionally labeled as M0, M1, M2, and M3. The categories come with different definitions, as follows:

The monetary base is a monetary aggregate that differs from the money supply but is widely observed due to its importance in money circulation. It includes money held in the vaults of financial institutions and the money in circulation. Since the aggregate can sometimes be multiplied using fractional reserve banking, it is also referred to as high-powered money (HPM). M0 can be seen as the foundation on which deposits’ superstructures are erected.

An increase in the reserve element of the base means that the system of depository institutions equally expands their deposits. On the other hand, M1 is the narrowly defined aggregate and measures the money supply that includes demand deposits, non-bank travelers’ checks in circulation, checkable deposits, and demand deposits. It measures all components of M0 plus near money.

Near money consists of highly cashless but liquid assets, such as money market securities, saving deposits, time deposits, and mutual funds. Although the assets can be easily converted into cash or checking deposits, they are not suitable as exchange mediums.

The Federal Reserve heavily relies on the money aggregates as a guide to monetary policymaking. The relationship among the monetary aggregates and microeconomic variables is used to forecast how economic activities, such as inflation, change in interest rates, and trading in Treasury securities, affect the economy’s health.

Analysts and investors also study such relationships because they present an accurate overview of a country’s working money supply. By reviewing monthly data on various aggregates, investors can measure the velocity of money and its equal opportunity cost, which gives the aggregate rate of change. The Fed can only control the reserves held by the monetary base and depository institutions, but not the quantity of money.

They are variables that influence short-term interest rates and eventually affect the monetary aggregates’ growth rate. For example, purchasing securities through the Federal Reserve open market leads to a great provision of reserves that consequently push down short-term interest rates and the federal funds rate.

For years, economists were unable to reach a consensus on universally accepted groupings of financial assets. In 1944, monthly data reports on two types of exchange media were initiated by the Federal Reserve System’s Board of Governors. The media included demand deposits at banks, such as deposits convertible into cash, as well as those transferable by checks, and currency outside of banks. M1 was used to refer to the total demand deposits and currency outside banks.

Most proposals focus on money as the best measure, but there is no universal definition of money. One of the approaches used to define money is to determine the specific purposes and use of financial assets. The method classifies money as a store of value and a medium of exchange. The second approach is to organize financial assets’ groupings whose movements are closely linked with certain microeconomic variables, including employment, prices, and national income.

The Board released estimates using M1 until 1971. Data on the new aggregates, i.e., M1 and M2, was reported to reflect the importance of formulating monetary policy using monetary aggregates. Additionally, they also reflect some economists’ view that assets capable of providing a temporary store of value should also constitute an appropriate definition of money.

The introduction of many financial instruments during the 1970s led to the substitutes of new asset classes. The new changes coincided with the relationship between monetary aggregates and economic variables.

At such a point, the Federal Reserve used the two approaches of defining money to construct monetary aggregates in 1980. The definition of M1 was replaced with M1A and M1B. At the same time, M2 and M3 replaced the old M2 through M5. Since 1982, the Board redesigned M1B as M1, with their respective definitions undergoing slight modifications over the years.

A country’s economic health and financial stability is assessed using data on monetary aggregates. As a result, for decades, they’ve been used by central banks in establishing monetary policies.

Nevertheless, in the past few decades, economists were able to prove the disconnect between fluctuation in money supply metrics, such as unemployment, GDP, and inflation. The central bank’s monetary policy guides the release of money into the economy by the Federal Reserve.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: