Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A savings account or highly liquid assets set aside to meet unexpected costs or financial obligations

A reserve fund refers to a savings account or highly liquid assets set aside to meet unexpected costs or financial obligations. Businesses, individuals, and condominium homeowners’ associations are common users of reserve funds.

Reserve funds are established to meet unexpected future costs or financial obligations that may occur. Additionally, they may be used to cover scheduled and routine expenses. Periodic deposits are usually made into the fund, and cash or highly liquid assets are drawn out as needed. Reserve funds are typically kept in a highly liquid account such as a savings account.

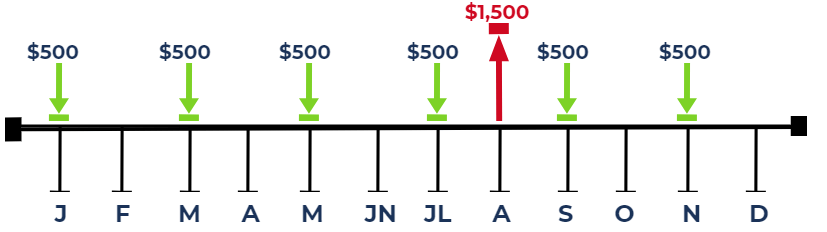

For example, consider a business that makes bi-monthly $500 deposits into a reserve fund and faces an unexpected cost of $1,500 in August:

Through a reserve fund, the business is able to accumulate cash and pay off the unexpected financial obligation in August without having to draw cash from the business’s general operating fund.

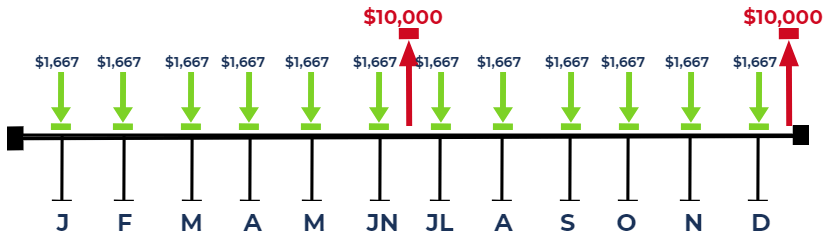

ABC Company is looking to establish a reserve fund due to the inconvenience of having to draw cash from the company’s general operating fund. The company anticipates paying expenses of $10,000 bi-annually related to third-party contracts. Currently, it is the beginning of 2027. Assuming no interest income or unexpected future costs, how much would the company need to deposit into the fund on a monthly basis?

To meet expenses of $10,000 paid bi-annually, the company must deposit at least $1,667 every month into the reserve fund. By doing so, the company would have $10,002 ($1,667 x 6) to meet the $10,000 expense due at the end of July and $10,002 ($1,667 x 6) to meet the $10,000 expense due at the end of December.

At the end of the year, the company would have $4 ($1,667 x 12 – $10,000 x 2) remaining in the fund.

Condominium homeowners associations commonly use such funds to handle renovation projects, unexpected maintenance costs, emergencies, etc. In Ontario, Canada, the Condominium Act, 1998 requires all condominium complexes to maintain a reserve fund.

For condominiums, cash inflows are through:

For a condominium complex, cash outflows are through:

The reserve fund balance fluctuates year-over-year depending on financial obligations. Therefore, the fund’s balance may be high one year and low the next year.

In this context, a “critical year” refers to a year in which the fund’s balance is unusually low. Low is referenced relative to the average fund balance.

For example, assume that the average planned reserve fund balance is $100,000 for the period 2021-2026. Unexpectedly, in 2027, a major repair cost is incurred, dropping the fund’s balance to a low of $20,000. In this case, 2027 would be termed a “critical year.”

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: