Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The tendency of an economic agent to strictly prefer certainty to uncertainty

Risk aversion refers to the tendency of an economic agent to strictly prefer certainty to uncertainty. An economic agent exhibiting risk aversion is said to be risk averse. Formally, a risk averse agent strictly prefers the expected value of a gamble to the gamble itself.

A gamble consists of three elements:

Consider the following example: John and Mark are playing a game. John flips a coin and if it is heads, then Mark gives him $10. If it is tails, then Mark gives John $20.

The general formula for expected value is the following:

Therefore, the expected value of the gamble described above is +$15 for John. He will make $15 every time he takes part in the gamble. If John is risk averse, then he strictly prefers receiving $15 with certainty to the gamble.

The risk premium of a gamble is the extra amount required to make an agent indifferent between the gamble and the expected value of the gamble. Conversely, it can also be thought of as the amount of money a risk averse agent will pay to avoid any risk.

In the example above, the expected value of the gamble is $15. The utility received from the expected value of the gamble is 1.17 (log 15). The expected utility from the gamble is 1.15 (½ log 10 + ½ log 20). It is equal to the utility received when consumption is $14.

Therefore, the risk premium is $15 – $14 = $1. A risk averse agent is indifferent between a gamble that offers an expected value of $15 and receiving $14 with certainty. The consumer would pay up to $1 to avoid taking the gamble.

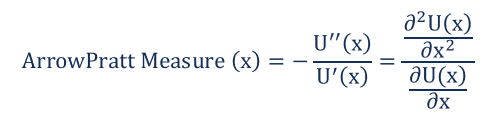

The Arrow-Pratt measure of risk aversion is the most commonly used measure of risk aversion. It analyzes the degree of risk aversion by analyzing the utility representation. The measure is named after two economists: Kenneth Arrow and John Pratt. The Arrow-Pratt formula is given below:

Where:

Speaking more practically, risk aversion is an important concept for investors. A risk averse investor prefers low risk investments that offer a guaranteed, or “risk-free,” return. They prefer this lower risk even if it means lower returns compared to potentially higher returns that carry a higher degree of risk.

For example, extremely risk-averse investors prefer low risk investments such as government bonds and certificates of deposit (CDs) to higher risk investments such as stocks and commodities.

Investors with a higher risk tolerance — or lower levels of risk aversion — are willing to accept more risk in exchange for the opportunity to earn higher returns on investment. Many investment portfolios include a mix of risky assets like stocks and low risk assets like bonds.

Thank you for reading CFI’s guide on Risk Aversion. To keep learning and developing your knowledge of risk aversion in finance, we highly recommend the additional CFI resources below: