Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A loan facility offered by a group of lenders to a large borrower

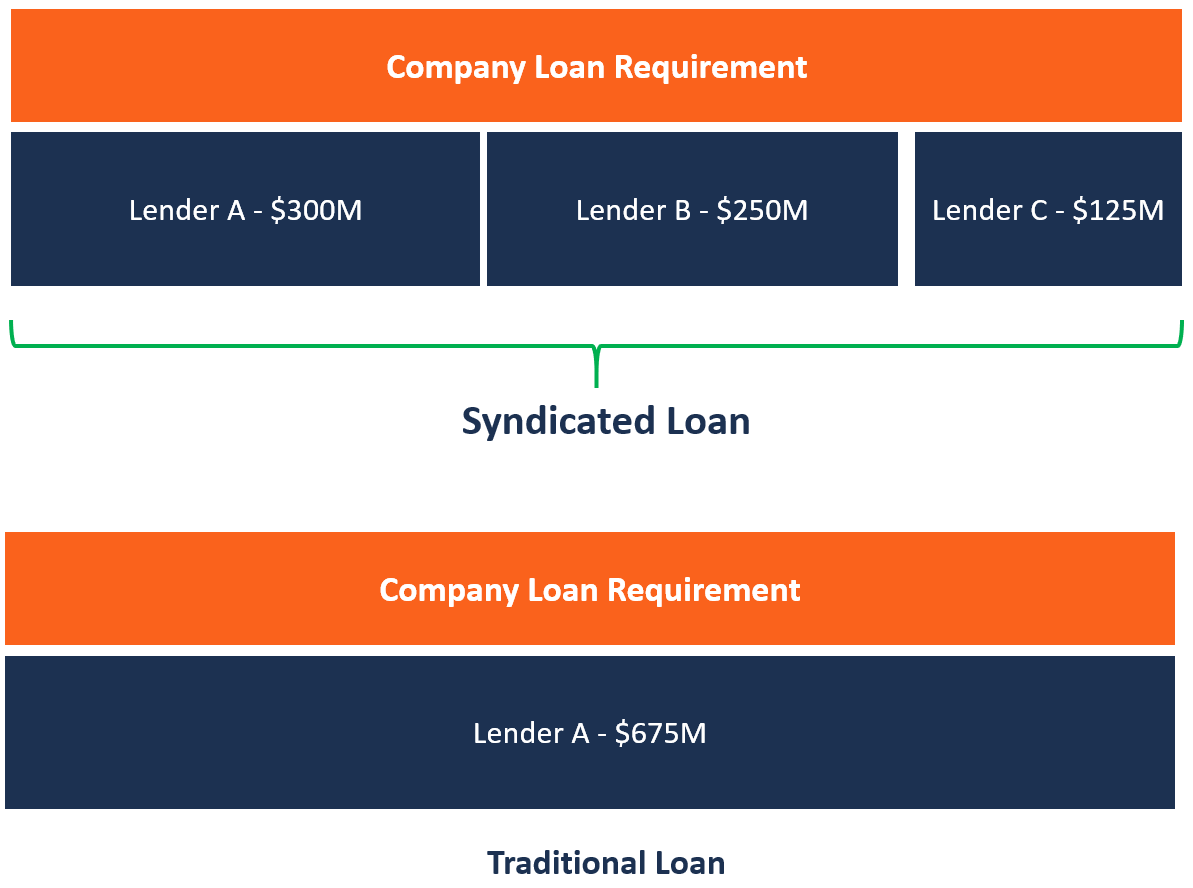

A syndicated loan is offered by a group of lenders who work together to provide credit to a large borrower. The borrower can be a corporation, an individual project, or a government. Each lender in the syndicate contributes part of the loan amount, and they all share in the lending risk.

One of the lenders acts as the manager (arranging bank), which administers the loan on behalf of the other lenders in the syndicate. The syndicate may be a combination of various types of loans, each with different repayment terms that are agreed upon during negotiations between the lenders and the borrower.

Loan syndication occurs when a single borrower requires a large loan ($1 million or more) that a single lender may be unable to provide, or when the loan is outside the scope of the lender’s risk exposure.

Lenders then form a syndicate that allows them to spread the risk and share in the financial opportunity. The liability of each lender is limited to their share of the total loan. The agreement for all members of the syndicate is contained in one loan agreement.

To learn techniques on how to analyze a company’s Financials check out CFI’s Financial Analysis Fundamentals Course.

Those who participate in loan syndication may vary from one deal to another, but the typical participants include the following:

The arranging bank is also known as the lead manager and is mandated by the borrower to organize the funding based on specific agreed terms of the loan. The bank must acquire other lending parties who are willing to participate in the lending syndicate and share the lending risks involved. The financial terms negotiated between the arranging bank and the borrower are contained in the term sheet.

The term sheet details the amount of the loan, repayment schedule, interest rate, duration of the loan and any other fees related to the loan. The arranging bank holds a large proportion of the loan and will be responsible for distributing cash flows among the other participating lenders.

The agent in a syndicated loan serves as a link between the borrower and the lenders and owes a contractual obligation to both the borrower and the lenders.

The role of the agent to the lenders is to provide them with information that allows them to exercise their rights under the syndicated loan agreement. However, the agent has no fiduciary duty and is not required to advise the borrower or the lenders. The agent’s duty is mainly administrative.

The trustee is responsible for holding the security of the assets of the borrower on behalf of the lenders. Syndicated loan structures avoid granting the security to the individual lenders separately since the practice would be costly to the syndicate.

In the event of default, the trustee is responsible for enforcing the security under instructions by the lenders. Therefore, the trustee only has a fiduciary duty to the lenders in the syndicate.

The following are the main advantages of a syndicated loan:

The borrower is not required to meet all the lenders in the syndicate to negotiate the terms of the loan. Rather, the borrower only needs to meet with the arranging bank to negotiate and agree on the terms of the loan.

The arranger then does the bigger work of establishing the syndicate, bringing other lenders on board, and discussing the loan terms with them to determine how much credit each lender will contribute.

Since a syndicated loan is contributed to by multiple lenders, the loan can be structured in different types of loans and securities. The varying loan types offer different types of interest, such as fixed or floating interest rates, which makes it more flexible for the borrower.

Also, borrowing in different currencies protects the borrower from currency risks resulting from external factors such as inflation and government laws and policies.

Loan syndication allows borrowers to borrow large amounts to finance capital-intensive projects. A large corporation or government can borrow a huge loan to finance large equipment leasing, mergers, and financing transactions in telecommunications, petrochemicals, mining, energy, transportation, etc.

A single lender would be unable to raise funds to finance such projects, and therefore, bringing several lenders to provide the financing makes it easy to carry out such projects.

The participation of multiple lenders to finance a borrower’s project is a reinforcement of the borrower’s good market image. Borrowers who have successfully paid syndicated loans in the past elicit a positive reputation among lenders, which makes it easier for them to access credit facilities from financial institutions in the future.

Thank you for reading CFI’s explanation of a syndicated loan. CFI offers the Commercial Banking & Credit Analyst (CBCA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: