Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A corporation is a legal business structure that operates independently of its owners, offering limited liability and the ability to own assets, pay taxes, and enter into contracts.

A corporation is a legal entity created by individuals, stockholders, or shareholders, with the purpose of operating a business for profit. A corporation, by definition, exists as a separate legal structure from its owners and is recognized under state laws. This separation provides limited liability protection, meaning the corporation (not its owners) is responsible for debts and legal obligations.

A legally incorporated business can:

Corporations are commonly chosen for their ability to scale, attract investors, and limit personal liability for their owners.

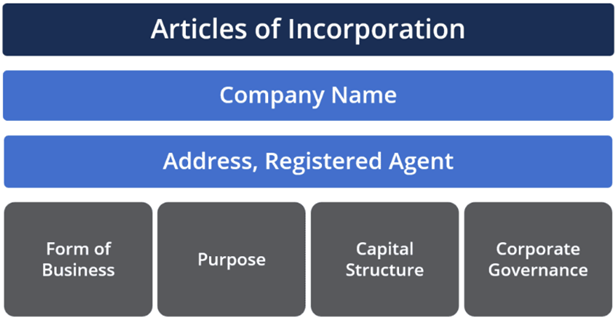

The process of incorporation involves filing Articles of Incorporation with a state agency, paying registration fees, and defining the business’s legal structure. Key details typically include:

Once incorporated, a corporation becomes a separate entity, responsible for its own taxes and obligations. This structure enables businesses to grow, raise funds, and operate with a professional governance framework.

A corporation can be formed by a single shareholder or by a group of investors pursuing a shared goal. Depending on the business model, it may be registered as either a for-profit or non-profit organization.

| C Corporation | Large or growing businesses | Double taxation | Unlimited shareholders (U.S. or foreign) | Easier to raise capital, grant employee stock options |

| S Corporation | Small U.S.-based businesses | Pass-through taxation | Max 100 U.S. shareholders | Avoids double taxation, retains limited liability |

| Non-Profit | Charitable or social orgs | Tax-exempt (IRS 501(c)(3)) | No shareholders; governed by the board | Eligible for grants, donations, tax-deductible funding |

Businesses can choose from several corporate structures depending on their goals, tax treatment, and ownership model. The most common types include:

C Corporation is the most common form of incorporation among businesses. Owners receive profits and are taxed at the individual level, while the corporation itself is taxed as a business entity.

This structure offers flexibility for raising capital by issuing stock and is often favored by businesses seeking outside investment.

S Corporation is created in the same way as a C Corporation but is different in owner limitation and tax purposes. An S Corporation consists of up to 100 shareholders and is not taxed as separate — instead, the profits/losses are shouldered by the shareholders on their personal income tax returns.

S Corps can be a smart choice for small business owners who want legal protection without double taxation.

Commonly used by charitable, educational, and religious organizations to operate without generating profits. A non-profit is exempt from taxation. Any contributions, donations, or revenue received are retained in the entity to spend on operations, expansion, or future plans.

Profits generated by a non-profit must be reinvested in the organization’s mission — not paid out to shareholders.

Corporations are owned by shareholders who invest money in exchange for stock. Each share typically gives its owner one vote in important company matters, including the election of the board of directors. The board is responsible for overseeing big-picture decisions and appointing officers — like the CEO, CFO, or vice presidents — to handle daily operations.

Shareholders don’t run the business’ day-to-day operations, but they can be elected to the board. This setup separates ownership from management, which allows shareholders to invest in the company without needing to be involved in its daily activities.

Board members are expected to act in the best interest of the company and its shareholders. To stay organized and legally compliant, corporations follow key governance practices like:

This structure helps ensure the business is well-managed and accountable to its owners.

Incorporating your business brings significant benefits — but also comes with some trade-offs. Below, we break down the key pros and cons to help you understand how forming a corporation compares to other business structures like partnerships or sole proprietorships.

Corporations offer a number of structural and financial benefits that can help your business grow, raise capital, and reduce personal risk.

While incorporating provides legal and financial benefits, it can also involve higher costs, more paperwork, and tax complexities.

While corporations can exist indefinitely, there are times when the business needs to close. This is called dissolution, and it can happen voluntarily or involuntarily, depending on the situation.

Dissolution is the legal process of shutting down a corporation. It includes settling debts, distributing any remaining assets, and officially ending the business with the state.

Once a corporation is set to dissolve, the liquidation process begins:

Even during closure, shareholders are generally not personally responsible for the company’s debts, unless they’ve personally guaranteed a loan or committed fraud.

A corporation is a legal business structure that exists separately from its owners. It can enter contracts, own assets, pay taxes, and be held liable without exposing its shareholders to personal financial risk.

A business becomes a corporation when it is legally incorporated by filing articles of incorporation with the state. This gives it a separate legal identity and allows it to issue stock, raise capital, and provide limited liability to its owners.

The main difference is how they’re taxed and managed. A corporation has shareholders and a board of directors and may face double taxation. An LLC is more flexible, with pass-through taxation and fewer formal requirements.

“Company” is a general term for a business, while a “corporation” refers to a specific legal structure that is incorporated under state law. All for-profit corporations are companies, but not all companies are corporations.

Understanding how corporations work is just one part of building a strong foundation in business and finance. Whether you’re exploring different business structures or preparing to launch a company, it’s important to know how corporations compare to other entities and how they fit into the broader legal and financial landscape.

If you’re looking to build deeper knowledge in financial analysis, corporate structure, and valuation, CFI’s certification programs are designed to help you take the next step.

Explore more free learning materials from CFI: