Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Tax paid by employers to support the government (or state) unemployment program

FUTA is an abbreviation for Federal Unemployment Tax Act. FUTA Tax is a United States federal tax imposed on employers to help fund unemployment payments. The tax is imposed solely on employers who pay wages to employees.

FUTA Tax is used to pay employees who leave employment involuntarily and are eligible to claim unemployment insurance. The act requires employers to file Form 940 annually with the Internal Revenue Service (IRS). In some cases, the IRS may allow some employers to pay the tax in installments during the year.

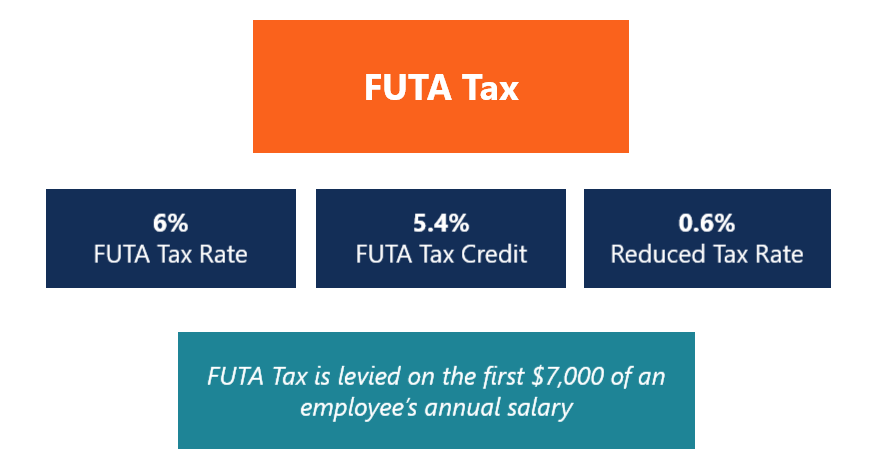

Employers are required to pay the Federal Unemployment Tax if they spend at least $1,500 in wages during a single calendar quarter. Still, it is only applied to the first $7,000 of each employee’s wages in the current or previous year.

Even if the employer records $1,500 or more in a single quarter and the other quarters fall below the threshold, the employer will still be required to pay the FUTA tax. As of 2021, the FUTA rate stands at 6.0%, and employers can claim a credit of up to 5.4% of their taxable income if they also pay state unemployment taxes.

When calculating FUTA taxes, it is important to understand the kinds of incomes that need to be taxed. Ideally, the unemployment tax is calculated on taxable wages that fall under the first $7,000 per employee per year limit. Any amounts exceeding $7,000 are tax-exempt. The taxable income comprises salaries and wages, commissions, bonuses, vacation allowances, sick pay, contributions to retirement plans, etc.

Other payments are also exempt from taxation, but they vary from state to state. Check with your state unemployment office to know which payments are exempt from the FUTA Tax. The tax amount is not deducted from the employee’s income – only the employer is responsible for it.

Let’s take the example of Company XYZ, which employs ten individuals. Each of these employees earns an annual taxable income of $10,000, bringing the total wages to $100,000. In such a case, the tax is applied to the first $7,000 in wages paid to each employee.

Therefore, the company’s annual FUTA tax will be 0.06 x $7,000 x 10 = $4,200. The employer will be required to submit $4,200 in FUTA taxes to the IRS. The company will also be required to remit any applicable state unemployment taxes to the state tax authority.

Some states are categorized as credit reduction states and are, therefore, ineligible to claim maximum credit reduction. When these states are unable to pay unemployment tax to residents who lost employment involuntarily, they may borrow from the federal government to facilitate the unemployment insurance payments. The federal government is entitled to recover the unpaid loans from the states by reducing the amount of credit available to them.

The reduction schedule is 0.3% for the first year and 0.3% for the following years until the loan is fully repaid. Before the loan is fully paid, the states cannot benefit from the maximum credit reduction of 5.4% and will, therefore, pay higher FUTA taxes than other states. However, if a state has fully paid these loans, it can claim the max tax credit reduction of 5.4%. It means that they will only pay 0.6% in FUTA tax.

Various forms of payments are paid to employees that are exempt from the Federal Unemployment Tax Act. The payments include:

Assume that Company XYZ company employs three staff – John, James, and Peter. John earns an annual income of $30,000, including $2,000 in employer contribution to health insurance, James earns an annual income of $20,000, including $1,200 in contribution to a 401 (k), while Peter earns an annual income of $25,000, including $1,800 in employer contributions to a SIMPLE retirement account. It means that total payments exempted from FUTA taxes are $2,000 + $1,200 + $1,800 = $5,000.

The IRS requires employers to make payments to the federal tax agency by the last day of the month after the end of the quarter. The FUTA tax liability for the quarter must be $500 or more for the employer to make a deposit with the IRS. If it is less than $500, it is carried forward to the next quarter.

The frequency of FUTA tax payments depends on the amount of tax owed and the number of employees. Employers must use the Electronic Federal Tax Payment System to make payments to the IRS.

Let’s take the example of a company that owes the IRS $400 in Quarter 1, $350 in Quarter 2, $490 in Quarter 3, and $550 in Quarter 4. Since the FUTA tax liability in Q1 is less than the required $500, the company will carry forward the $400 for Q1 to Q2. That will bring the total tax liability for Q2 to $750 ($400 + $350), which the company will be required to remit to the IRS by July 31st (the last day of the next month after the end of Q2).

The tax liability for Q3 is below the FUTA tax limit by $10. The tax liability will be carried forward to the last quarter of the year. It will bring the FUTA tax liability for Q4 to $1,040 ($490 + $550). The company must remit the FUTA tax liability by January 31st of the following month.

Note: The article above is for educational purposes only. Always consult a professional adviser before making any tax-related or investment decisions.

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: