Get In-Demand Finance Certifications

The practice of mitigating financial risks resulting from a mismatch of assets and liabilities

Asset and liability management (ALM) is a practice used by financial institutions to mitigate financial risks resulting from a mismatch of assets and liabilities. ALM strategies employ a combination of risk management and financial planning and are often used by organizations to manage long-term risks that can arise due to changing circumstances.

The practice of asset and liability management can include many factors, including strategic allocation of assets, risk mitigation, and adjustment of regulatory and capital frameworks. By successfully matching assets against liabilities, financial institutions are left with a surplus that can be actively managed to maximize their investment returns and increase profitability.

At its core, asset and liability management is a way for financial institutions to address risks resulting from a mismatch of assets and liabilities. Most often, the mismatches are a result of changes to the financial landscape, such as changing interest rates or liquidity requirements.

A full ALM framework focuses on long-term stability and profitability by maintaining liquidity requirements, managing credit quality, and ensuring enough operating capital. Unlike other risk management practices, ALM is a coordinated process that uses frameworks to oversee an organization’s entire balance sheet. It ensures that assets are invested most optimally, and liabilities are mitigated over the long term.

Traditionally, financial institutions managed risks separately based on the type of risk involved. Yet, with the evolution of the financial landscape, it is now seen as an outdated approach. ALM practices focus on asset management and risk mitigation on a macro level, addressing areas such as market, liquidity, and credit risks.

Unlike traditional risk management practices, ALM is an ongoing process that continuously monitors risks to ensure that an organization is within its risk tolerance and adhering to regulatory frameworks. The adoption of ALM practices extends across the financial landscape and can be found in organizations such as banks, pension funds, asset managers, and insurance companies.

Implementing ALM frameworks can provide benefits for many organizations, as it is important for organizations to fully understand their assets and liabilities. One of the benefits of implementing ALM is that an institution can manage its liabilities strategically to better prepare itself for future uncertainties.

Using ALM frameworks allows an institution to recognize and quantify the risks present on its balance sheet and reduce risks resulting from a mismatch of assets and liabilities. By strategically matching assets and liabilities, financial institutions can achieve greater efficiency and profitability while reducing risk.

The downsides of ALM involve the challenges associated with implementing a proper framework. Due to the immense differences between different organizations, there is no general framework that can apply to all organizations. Therefore, companies would need to design a unique ALM framework to capture specific objectives, risk levels, and regulatory constraints.

Also, ALM is a long-term strategy that involves forward-looking projections and datasets. The information may not be readily accessible to all organizations, and even if available, it must be transformed into quantifiable mathematical measures.

Finally, ALM is a coordinated process that oversees an organization’s entire balance sheet. It involves coordination between many different departments, which can be challenging and time-consuming.

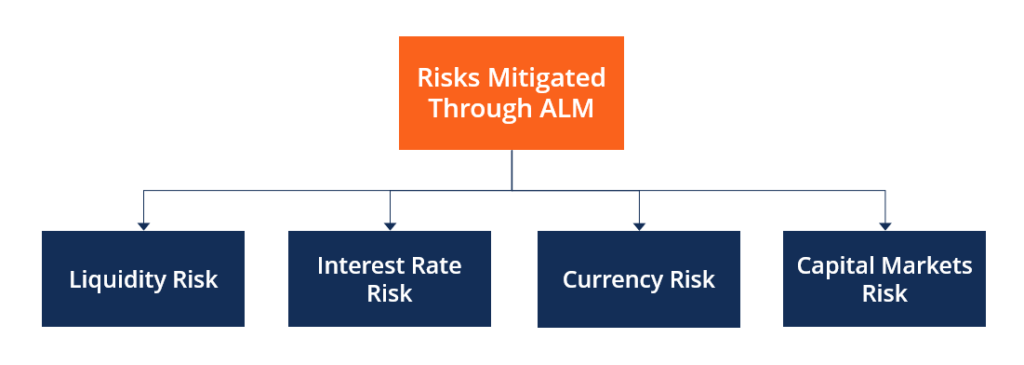

Although ALM frameworks differ greatly among organizations, they typically involve the mitigation of a wide range is risks. Some of the most common risks addressed by ALM are interest rate risk and liquidity risk.

Interest rate risk refers to risks associated with changes to interest rates, and how changing interest rates affect future cash flows. Financial institutions typically hold assets and liabilities that are affected by changing interest rates.

Two of the most common examples are deposits (assets) and loans (liabilities). As both are impacted by interest rates, an environment where rates are changing can result in a mismatching of assets and liabilities.

Liquidity risk refers to risks associated with a financial institution’s ability to facilitate it’s present and future cash-flow obligations, also known as liquidity. When the financial institution is unable to meet its obligations due to a shortage of liquidity, the risk is that it will adversely affect its financial position.

To mitigate the liquidity risk, organizations may implement ALM procedures to increase liquidity to fulfill cash-flow obligations resulting from their liabilities.

Aside from interest and liquidity risks, other types of risks are also mitigated through ALM. One example is currency risk, which are risks associated with changes to exchange rates. When assets and liabilities are held in different currencies, a change in exchange rates can result in a mismatch.

Another example is capital market risk, which are risks associated with changing equity prices. Such risks are often mitigated through futures, options, or derivatives.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Asset and Liability Management (ALM).To keep learning and developing your knowledge base, please explore the additional relevant resources below: