Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A bullish options trading strategy that involves both buying and selling call options

A call ratio back spread is a bullish options trading strategy that involves both buying and selling call options. The strategy is designed to maximally profit from a significant upward movement in the price of the underlying stock in the near term. The combination of options bought and sold limits your risk while still maintaining theoretically unlimited profit potential.

Higher volatility in the price of the underlying stock is a plus for the call ratio back spread strategy, likely to help maximize gains.

The “ratio” in the option strategy name refers to the fact that a 2:1 ratio of bought call options to sold call options is employed. It is referred to as a “back spread” because it is commonly employed using longer-term or “back-month” options, thus affording more time for the trade to work in the investor’s favor.

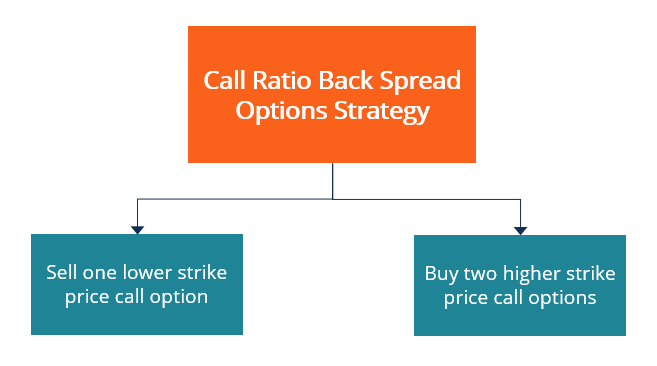

The call ratio back spread strategy is implemented as follows:

All options bought and sold should have the same expiration date. The trade may be put into place for a net credit if the money received for selling the one lower strike price call option is more than the cost of the two higher strike price call options that are purchased.

Whether the trade is put into place with a net credit or net debit will depend on the specific option strike prices, the distance between the option strike prices, the volatility of the option prices, and the time remaining until the options expire.

There is theoretically unlimited potential profit from a rise in the underlying stock price, thanks to the purchase of two call options, which makes the strategy a net long call position.

If you can establish this call spread position for a net credit, then there is also potential profit even if the price of the underlying stock falls rather than rises. If at the time all of the options expire, the price of the stock is below the strike price of the call option that was sold, then all of the options will expire worthless, but you will retain the credit received when the position was established.

There is no potential profit from a downside move if the position is established at a net debit, but the maximum loss is limited to the amount of the net debit incurred when the strategy was put in place.

The maximum potential loss occurs if, at the time of the options’ expiration, the price of the underlying stock is at the higher strike price of the two calls that were purchased. The maximum amount of loss at that point will equal the difference between the bought and sold call strike prices and either minus the net credit received when establishing the position or plus the net debit incurred when establishing the position.

Assume that the underlying stock is trading at $32 per share when a trader implements the call ratio back spread strategy by selling one call option with a strike price of $30 and buying two call options with a strike price of $35. There are four possible scenarios that can unfold for the trader, as follows:

1. Maximum Loss: If the underlying stock is trading at $35 per share when the options expire, then both $35 strike price calls purchased will expire worthless, while the $30 strike price call that was sold is in-the-money with an intrinsic value of $500 for the option buyer. Thus, it will cost the trader employing the call ratio back spread strategy $500 to close out their position.

2. Breakeven: If, at the time of the options expiration, the underlying stock is at $40 per share, then the sold call will show a $1,000 loss, but the purchased calls, combined, will show a $1,000 profit.

3. Maximum Profit: Maximum profit from the call ratio back spread is achieved as the price of the underlying stock rises above $40 per share. Beyond such a point, the intrinsic value of the two purchased calls will be greater than the intrinsic value loss incurred from the lower strike price call that was sold.

4. If, at expiration, the price of the underlying stock has fallen to below $30 a share, then all the options expire worthless, and whether the trader generates a small profit or incurs a small loss depends on whether the call spread was implemented with a net credit or net debit.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: