Fixed Income Portfolio Mandates

The set of rules that should be followed while investing in a variety of fixed-income securities

What are Fixed Income Portfolio Mandates?

Fixed-income portfolio mandates refer to the set of rules that should be followed while investing in a variety of fixed-income securities. A fixed-income security is one that gives the investor a fixed amount of interest payment every year until maturity. Some examples of fixed-income securities include certificates of deposit, corporate bonds, and government bonds.

Although fixed-income securities are considered safer investment options compared to the stock market, they face certain risks. In order to eliminate such risks, investment managers follow certain mandates while building a portfolio.

Summary

- Fixed-income portfolio mandates refer to the set of rules that should be followed while investing in a variety of fixed-income securities.

- Fixed-income securities are prone to certain risks, such as interest rate risk, credit risk, inflation risk, and liquidity risk.

- Mandates such as cash flow matching, duration matching, diversification, and indexing are used to minimize such risks.

Risks Associated with Fixed-Income Securities

Like all investments, fixed-income securities also face the following major risks:

1. Interest Rate Risk

The market value of fixed-income securities, like bonds, move inversely with changes in the interest rate. Bonds need not be held from the time of issue until maturity; they can be traded like stocks. If a 5% bond with a face value of $1,000 is available for sale in the market with an interest rate of 5%, then prospective investors would buy the bond for $1,000.

However, if the market interest rate is greater than 5%, investors would pay less than $1,000 for the bond, because other assets would give the investor higher returns than the bond. Therefore, a rise in interest rates causes a fall in the bond’s value and vice-versa. The fluctuation can lead to a capital loss if the bondholder wishes to sell the bond before maturity.

2. Credit Risk

Credit risk refers to the risk of default, that is, the risk that the issuer fails to make payments. In situations of economic uncertainty, issuers face the prospect of bankruptcy. Under such conditions, they fail to make payments on the securities issued, and the investors incur losses on their investment. The risk of default is higher for securities that offer higher returns.

3. Inflation Risk

Fixed-income securities pay a constant amount of interest every year. If the level of inflation rises, the purchasing power of the fixed income will fall. It is a serious risk for people who expect to live off their income from such investments, like retired people.

4. Liquidity Risk

The market for fixed-income securities is not as liquid as that for stocks. It is because the number of buyers and sellers is much less in the fixed-income market, owing to the fixed payment structure and comparatively lower returns.

As a result, bondholders wishing to sell their bonds before maturity may not find buyers offering the quoted price. It can cause bonds to sell for a lower price, and the seller can incur a capital loss.

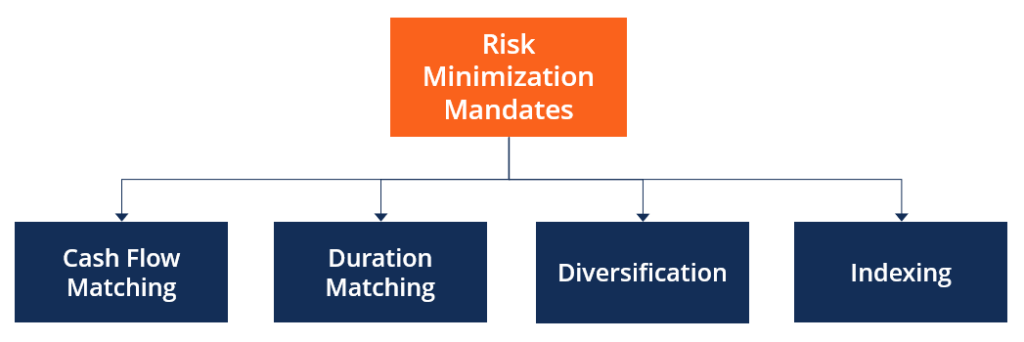

Mandates for Risk Minimization

In order to safeguard fixed-income portfolios from one or more of the above risks, there are certain steps that investors and portfolio managers undertake. All steps are referred to as immunization strategies, that is, strategies to immunize a basket of securities from exposure to risk. Some of the most popular immunization strategies are as follows:

1. Cash Flow Matching

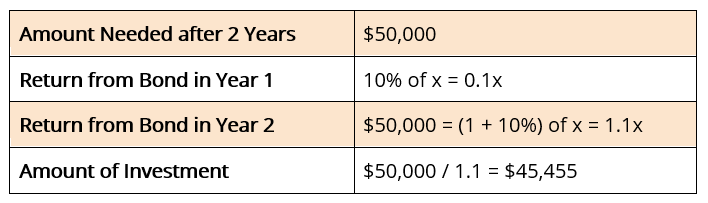

Investors use the cash flow matching strategy when they want their portfolios to amount to a value in the future equivalent to a liability or payment for certain expenses. For example, Individual A wants $50,000 after two years to pay for their children’s college tuition.

The individual must invest an amount today (say, x) that will be worth at least $50,000 at the end of two years. A is given the option of investing in a certain two-year 10% bond. The amount required for investment is calculated as follows:

individual A must invest $45,455 at present to receive the $50,000 needed for their children’s tuition.

2. Duration Matching

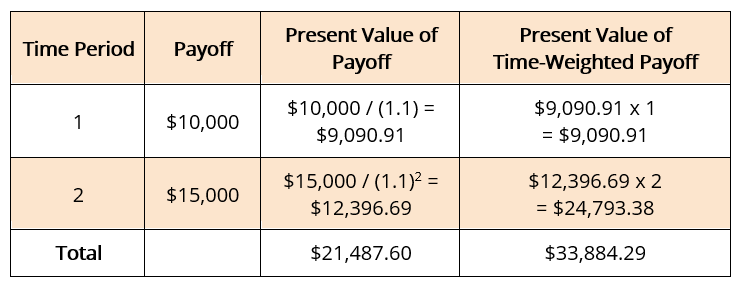

The duration of a cash flow refers to the time it will take to pay the present values of future maturities. It is calculated as the time-weighted average of maturity periods. For example, a pension fund needs to pay out $10,000 after one year and $15,000 after two years. Assume that the market rate of interest is 10%. The duration of the payment is calculated as follows:

The duration of the above payoff = 33,884.29 / 21,487.60 = 1.58 years

Any change in interest rates will change the present values and the duration of the payoff. In order to mitigate such a risk, the pension fund should invest in fixed-income securities with the same duration as the payoff, that is, 1.58 years. It will ensure that the value of cash outflows always equal those of inflows even in case of interest rate fluctuations.

3. Diversification

The diversification strategy is mainly used to mitigate default risk. A diversified portfolio contains a variety of securities from different industries and investment grades. It is done to reduce complete dependence on only one class of assets.

For example, bonds with high coupon rates are also the ones most likely to default. A combination of the bonds with low-yielding ones will reduce the possibility of default and increase the average interest rate of the portfolio.

4. Indexing

The fixed-income security market has certain indices that project the performance of the market as a whole. Investors and portfolio managers find it a safe strategy to invest in those securities that constitute the market index.

Diversification ensures that returns from a portfolio equal the market performance. Moreover, since market indices are composed of the most reliable securities, indexing ensures a certain level of safety in investments.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: