Forward Premium

Occurs when the forward exchange rate is quoted higher than the spot exchange rate

What is a Forward Premium?

Forward premium occurs when the forward exchange rate is quoted higher than the spot exchange rate. The expectation of the market is that the domestic currency will be worth less in the future or will depreciate in value versus the foreign currency.

To determine the forward premium, the difference between the spot rate and the forward rate must be estimated. This calculation assumes that the future spot rate and the current futures rate will be equivalent.

This assumption is supported by pragmatic studies around the expectation’s theory of exchange rates, the current spot futures rate is expected to be the future spot rate.

Summary

- A forward premium occurs when the forward exchange rate is quoted higher than the spot exchange rate.

- A forward contract will have a premium when the expectation in the market is for the domestic currency to depreciate in value in the future versus the foreign currency

- To find the forward premium for a currency pair, the forward exchange rate must be calculated.

Determining the Forward Premium

To find the forward premium for a currency pair, the forward rate must be calculated. It is found by using the predominant interest rates of both the local and foreign currencies and the current spot rate and is adjusted for time until expiration. The forward rate is found with the use of forward points.

Forward points are the basis points that are added to or deducted from the current spot rate to determine the future forward rate . Forward currency contracts tend to be quoted in forward points. Forward points are estimated predominant interest rates of the two currencies and with the consideration of the contract length.

The addition of forward points to a spot rate is known as a forward premium, and the subtraction of forward points to a spot rate is known as a forward discount.

A forward point is equivalent to 1/10,000 of a spot rate. For example, a forward contract is believed to include 170 forward points. It is written as 170/10,000 and is added to the spot price to estimate the forward rate.

The fraction 170/10,000 equates to 0.017 units. Hence, the forward rate will be computed by adding the 0.017 unit to the current spot rate. If the situation is reversed and the 170 forward points are to be subtracted from the spot rate, the future rate will be 0.017 units fewer than the spot rate.

Example

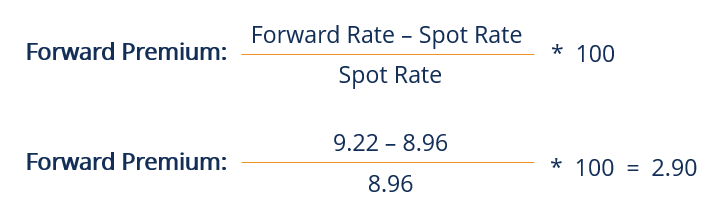

The Canadian dollar and the Namibian Dollar are currently quoted at CAD/NAD = 8.96, with annual interest rates of 4.00% and 7.00%, respectively.

The forward rate can be determined as follows:

To find the forward premium, the forward exchange rate (as computed above) and the spot exchange rate are needed to satisfy the following equation:

Forward Points, Interest Rates, and Forward Rates

Generally, forward points tend to mirror or reflect interest rate disparities between currency pairs. The points can either be positive or negative, in conjunction with lower or higher interest rates.

The adjustment of a spot rate through the addition or subtraction of forward points is done to represent and account for the interest rate differentials between a currency pair. In essence, the currency with a higher yield will be discounted and the currency with a lower yield may have a premium.

The Forward Premium Puzzle

The forward premium puzzle/anomaly (also known as the FAMA puzzle) is a common term in currency trading. The anomaly is based on studies that found that a local or domestic currency may appreciate against a foreign currency if the domestic interest rate is higher than the foreign nominal interest rate.

It is viewed as perplexing, based on the hypothesis that the projected future fluctuations in the exchange rate between nations is equivalent to the interest-rate differences between the respective countries.

The theory assumes that in a case where all currencies are comparably risky, investors will seek higher interest rates on currencies projected to decline in value.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: