Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Bonds that are linked to a country’s inflation index

An index-linked bond is used to protect the income earned by bond investors against inflation. Index-linked bonds are linked to a country’s inflation index. For example, the U.K. issues index-linked bonds called linkers that are linked to the Retail Price Index (RPI). Similarly, Canada issues Real Return Bonds (RRBs) that are linked to the Consumer Price Index (CPI).

Bond investors earn a fixed rate of return on the capital that they contribute. The coupon rate determines periodic interest payments received by bondholders. However, in an inflationary environment, the real value of cash flows earned through fixed coupon payments declines. Therefore, index-linked bonds are used as a hedge against inflation to secure the purchasing power of income earned through bonds.

Index-linked bonds were first issued during the American Revolution (1775-1783). The U.S. government financed the war by printing currency, which increased annual inflation to 30%. To protect interest income, Massachusetts issued an index-linked bond where payments were linked to a basket of goods and services representative of inflation.

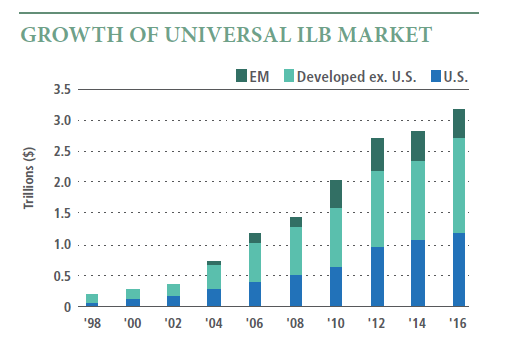

In 1981, the U.K. was the first industrialized nation to adopt index-linked bonds. Soon, adoption was followed by Sweden, Australia, and Canada. In 1997, the US began issuing TIPS or Treasury Inflation-Protected Securities, which comprise a Treasury bond that is linked to the Consumer Price Index (CPI).

Index-linked bonds are composed in two ways. One way involves adjusting the coupon rate to match inflation and keeping the face value constant. Such index-linked bonds are called C-linkers, as the inflation link is attached to coupons. C-linkers are often issued by commercial banks and life insurance companies.

The second kind of index-linked bond is constructed by adjusting the principal based on inflation and recalculating coupons using the adjusted principal. Such index-linked bonds are called P-linkers, as the inflation link is attached to the principal. P-linkers are usually issued by governments. Most index-linked bonds in the market are P-linkers, developed by adjusting the principal to inflation figures and recalculating coupons.

Let’s consider an example to understand the construction of index-linked bonds and arrive at real interest rates. In this example, the Consumer Price Index (CPI) will be used as a measure of inflation.

Bond CFI was issued at face value of $1,000, at an annual coupon rate of 10%, and with a maturity of 1 year. The Consumer Price Index (CPI) when the bond was issued was 170. A year later, CPI equals 175.

The indexation factor represents inflation and is used to adjust the bond’s principal. In this example, it will be calculated by dividing the bond’s CPI at maturity by its CPI at the time of issuance.

Indexation Factor = CPI at Maturity / CPI at Issuance = 175 / 170 = 1.0294

An indexation factor of 1.0294 indicates that the inflation rate is 2.94%. The figure can be confirmed by calculating the percentage change in CPI.

Inflation Rate = (175 – 170) / 170 = 0.0294 = 2.94%

As seen above, the percentage change in CPI confirms that inflation is 2.94%.

At maturity, the bond would pay out its face value and annual interest payment. The interest payment is the product of the annual coupon rate and face value.

Cash Flows from the Bond at Maturity = Face Value + Interest Payment = $1,000 + ($1,000 x 0.10) = $1,100

The product is the total amount received by investors when the security expires.

Amount Received at Maturity = $1,100 x 1.0294 = $1,132.34

The total amount received by bondholders at maturity will be $1,132.34. This amount includes the original face value ($1,000), annual interest payment ($100), and the amount adjusted for inflation ($32.34).

The nominal interest rate is the percentage change between the amount investors receive at maturity and the face value (the amount they contribute while purchasing the bond from the issuer).

Nominal Interest Rate = ($1,132.34 – $1,000) / $1,000 = 13.23%

According to Irving Fisher’s calculations, the equation below illustrates the relationship of real interest rate, nominal interest rate, and inflation.

Real Interest Rate = Nominal Interest Rate – Inflation Rate = 13.23% – 2.94% = 10.29%.

The real interest rate for this index-linked bond is 10.29%.

Since many index-linked bonds link bond principals to an inflation index, deflation can lower the adjusted principal. During a period of deflation, the inflation-adjusted principal can fall below its face value. To protect investors during deflationary periods, countries such as the U.S., France, Germany, and Australia provide deflation floors.

A deflation floor ensures that investors receive the face value of the index-linked bond at maturity, even if deflation’s caused the bond’s principal to fall below its face value. It offers capital protection to investors during periods where deflation can negatively affect the repayment values of their securities.

However, note that deflation can lower the value of coupons calculated based on a lower adjusted principal. Most countries only provide a deflation floor to secure the original face value of the bond. Australia is an exception to this standard, as Australian linkers protect coupon payments during deflation.

The break-even inflation rate refers to the difference in the nominal yield on a regular bond and the real yield on an index-linked bond. Investors choosing between a regular bond and an index-linked bond of the same maturity and credit risk consider the break-even inflation rate. It is the inflation rate at which the performance of an index-linked bond will be as good as the performance of a comparable regular bond.

If actual inflation is higher than break-even inflation over the life of the bonds, then investors will earn a higher return on index-linked bonds over regular bonds. If actual inflation is lower than break-even inflation, investors will earn a lower return on index-linked bonds than regular bonds.

For example, if a regular bond yields 3% and an index-linked bond provides a real yield of 2%, the break-even inflation rate will be 1%. If the investor expects inflation to be above 1% over the life of the bonds, then the index-linked bond will outperform the regular bond. If inflation equals 1%, then the regular and index-linked bond will perform equally well. If inflation falls below 1%, then the regular bond will outperform the inflation-linked bond.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: