Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

How to calculate Discounted Cash Flow (DCF)

This article breaks down the discounted cash flow DCF formula into simple terms. We will take you through the calculation step by step so you can easily calculate it on your own. The DCF formula is required in financial modeling to determine the value of a business when building a DCF model in Excel.

Discounted cash flow (DCF) is an analysis method used to value investments by discounting the estimated future cash flows. DCF analysis can be applied to value a stock, company, project, and many other assets or activities, and thus is widely used in both the investment industry and corporate finance management.

Innovative projects and growth companies are some examples where the DCF approach might not apply. Instead, other valuation models can be used, such as comparable analysis and precedent transactions.

The discounted cash flow (DCF) formula is equal to the sum of the cash flow in each period divided by one plus the discount rate (WACC) raised to the power of the period number.

Here is the DCF formula:

![]()

Where:

The CFn value should include both the estimated cash flow of that period and the terminal value. The formula is very similar to the calculation of net present value (NPV), which sums up the present value of each future cash flow. The only difference is that the initial investment is not deducted in DCF.

Cash Flow (CF) represents the net cash payments an investor receives in a given period for owning a given security (bonds, shares, etc.)

When building a financial model of a company, the CF is typically what’s known as unlevered free cash flow. When valuing a bond, the CF would be interest and or principal payments.

To learn more about the various types of cash flow, please read CFI’s cash flow guide.

For business valuation purposes, the discount rate is typically a firm’s Weighted Average Cost of Capital (WACC). Investors use WACC because it represents the required rate of return that investors expect from investing in the company.

For a bond, the discount rate would be equal to the interest rate on the security.

Each cash flow is associated with a time period. Common time periods are years, quarters, or months. The time periods may be equal, or they may be different. If they’re different, they’re expressed as a percentage of a year.

The DCF formula is used to determine the value of a business or a security. It represents the value an investor would be willing to pay for an investment, given a required rate of return on their investment (the discount rate).

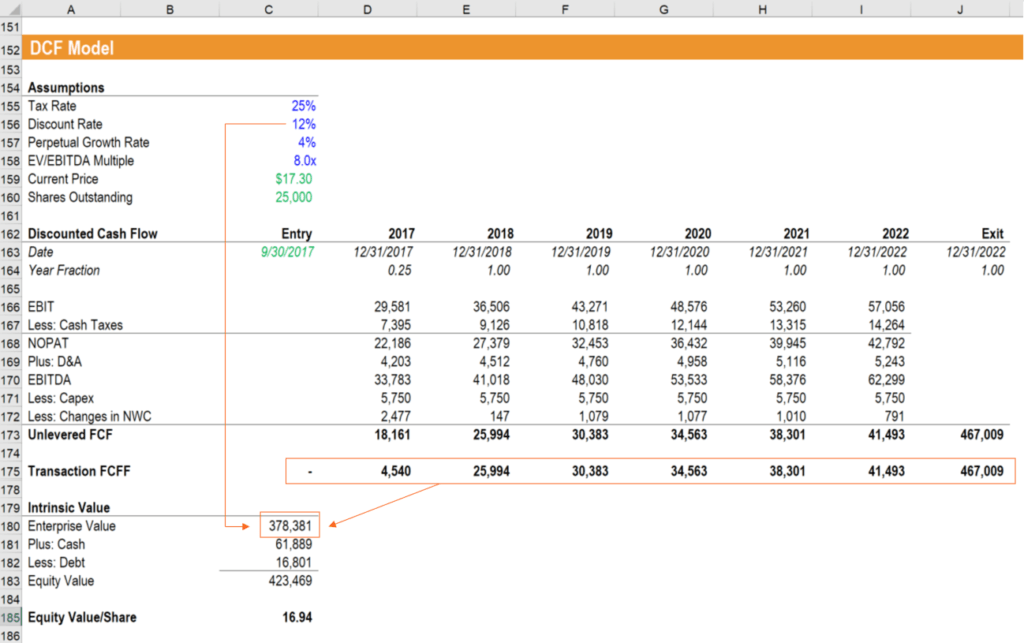

Below is a screenshot of the DCF formula being used in a financial model to value a business. The Enterprise Value of the business is calculated using the =NPV() function along with the discount rate of 12% and the Free Cash Flow to the Firm (FCFF) in each of the forecast periods, plus the terminal value.

Image: CFI’s Business Valuation Modeling Course

Enter your name and email in the form below and download the free DCF Model template now!

When assessing a potential investment, it’s important to take into account the time value of money or the required rate of return that you expect to receive.

The DCF formula takes into account how much return you expect to earn, and the resulting value is how much you would be willing to pay for something to receive exactly that rate of return.

If you pay less than the DCF value, your rate of return will be higher than the discount rate.

If you pay more than the DCF value, your rate of return will be lower than the discount.

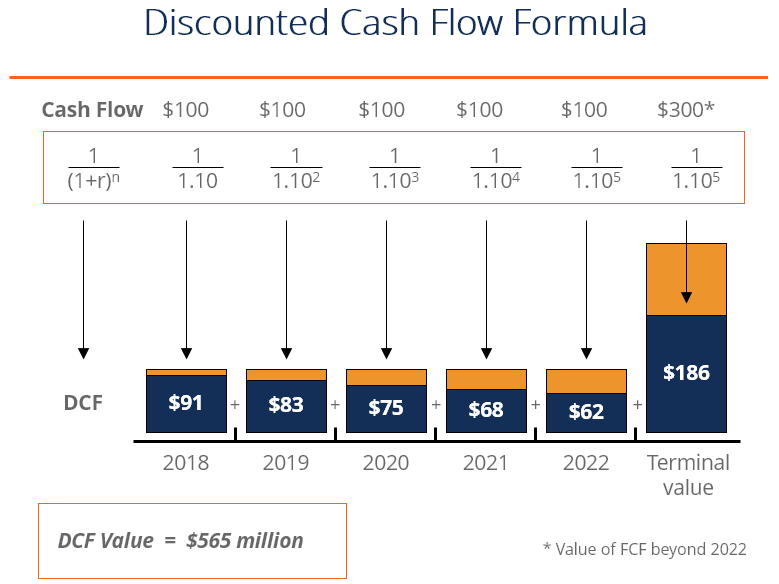

Below is an illustration of how the discounted cash flow DCF formula works. As you will see, the present value of equal cash flow payments is being reduced over time, as the effect of discounting impacts the cash flows.

Image: CFI’s free Intro to Corporate Finance Course

When valuing a business, the annual forecasted cash flows typically used are 5 years into the future, at which point a terminal value is used. The reason is that it becomes hard to make reliable estimates of how a business will perform that far out into the future.

There are two common methods of calculating the terminal value:

Check out our guide on how to calculate the DCF terminal value to learn more.

The total Discounted Cash Flow (DCF) of an investment is also referred to as the Net Present Value (NPV). If we break the term NPV, we can see why this is the case:

Net = the sum of all positive and negative cash flows

Present value = discounted back to the time of the investment

MS Excel provides two formulas that can be used to calculate discounted cash flow, which it terms as “NPV.”

Regular NPV formula:

=NPV(discount rate, series of cash flows)

This formula assumes that all cash flows received are spread over equal time periods, whether years, quarters, months, or otherwise. The discount rate has to correspond to the cash flow periods, so an annual discount rate of r% would apply to annual cash flows.

Time adjusted NPV formula:

=XNPV(discount rate, series of all cash flows, dates of all cash flows)

With XNPV, it’s possible to discount cash flows that are received over irregular time periods. This is particularly useful in financial modeling when a company may be acquired partway through a year.

For example, this initial investment may be on August 15th, the next cash flow on December 31st, and every other cash flow thereafter a year apart. XNPV can allow you to easily solve for this in Excel.

To learn more, see our guide on XNPV vs. NPV in Excel.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI’s mission is to help you advance your career. With that mission in mind, we’ve compiled a wide range of helpful resources to guide you along your path to becoming a certified Financial Modeling & Valuation Analyst (FMVA)® analyst.

Relevant resources include: