Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

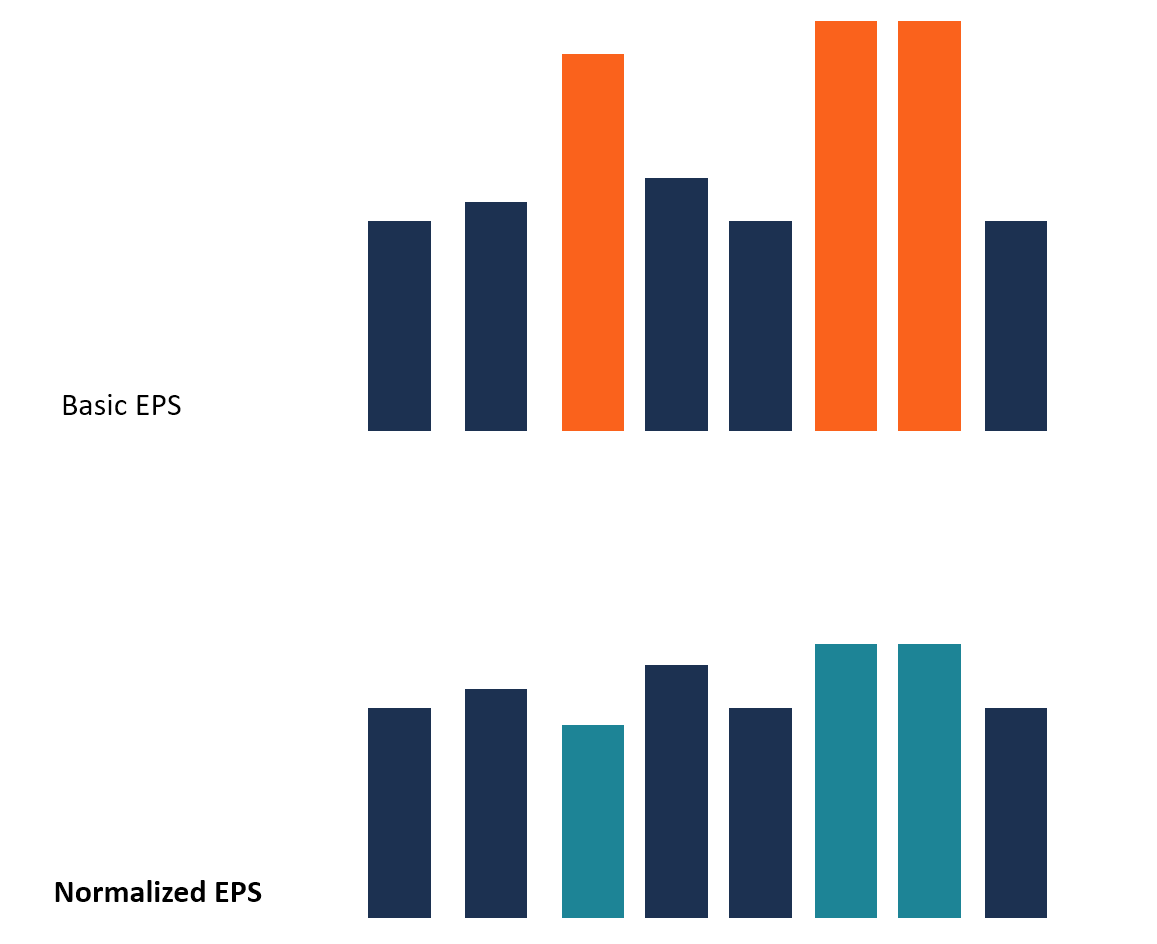

Removing unusual or one-time expenses from EPS

Normalized EPS refers to adjustments made to the income statement to reflect cycles of the economy, as well as adjustments that include removing unusual or one-time expenses that do not reflect the usual operations of the company.

Normalized EPS is intended to present an accurate picture of the company’s actual financial position, and the earnings are referenced during the sale of the business. They remove the fluctuations and provide an estimate of the earnings that the company would ordinarily generate in a typical year.

Normalized earnings are prepared by taking into account the information from previous years’ income statements. When the normalized earnings are high, it shows that the company typically generates higher revenues even if the economy has been experiencing up and down cycles.

Usually, the adjustments are made to the income statements that will be shown to potential buyers of the company. The buyers usually want to see the average earnings of the company, since the earnings for only one period may not reflect the actual performance of the company.

Approaches to normalizing the earnings of a company include:

This is one of the simplest ways to calculate normalized EPS since it only considers average dollar earnings during a specific economic cycle. Ideally, a firm should take the average earnings for an entire economic cycle in which it has experienced ups and downs that have affected the earnings. The economic cycles can range from 5 to 10 years.

This method is ideal for firms that have not changed in size during the period. For companies that have experienced tremendous growth during the period, the average dollar earnings method is likely to produce skewed results.

This method estimates the normalized earnings using scaled earnings rather than the average dollar earnings, as is the case with the first method. Companies that have grown in both size and revenues during the entire economic cycle can use this method to adjust the income statements for normalized earnings.

For example, assume that a company has returned an average yield of 10% during the entire economic cycle of eight years. If the company has invested $900 million in the current year, the company’s normalized earnings would be $90 million.

When calculating normalized earnings, analysts use the information from the company’s income statements during a given period. Here are the basic steps that companies use to calculate normalized earnings:

The following are the main types of expenses and gains that require adjustments when calculating normalized earnings:

Companies often incur certain non-recurring costs that are not part of the day-to-day expenses. These expenses include lawsuit costs, non-operating assets, asset depreciation costs, etc. When the expenses comprise a huge proportion of a company’s annual costs, it may experience a significant dip in its annual earnings due to non-recurring expenses.

Also, the business may experience huge gains during a financial year due to one-time gains like the sale of company assets, compensation from a lawsuit, etc. The short-term gains are not indicative of the company’s future performance. When analyzing the company or pitching a potential buyer, these short-term gains or losses would need to be removed to reflect the actual financial status of the company.

Discretionary expenses are costs associated with activities that are not directly related to the normal operating procedures of the business. The business does not need the costs to operate. The costs can be stopped, and the business will continue operating without disruption.

Examples of discretionary expenses include car rentals, vacation homes, executive bonuses, magazine subscriptions, conference charges, etc. The costs must be adjusted appropriately so that a potential buyer does not assume that the expenses are part of the company’s operational costs.

Assume that the founders of ABC Inc. are contemplating selling the business to an interested buyer. The buyer is interested in getting the latest statement for the company to know the financial position of the company. According to the company’s income statement for the previous year, the company earned an EBITDA of $7 million, a decrease of $2 million from the previous year.

The company’s analysts noted that the company incurred certain costs that are not part of the operational activities of the business. The expenses include a $2.3-million lawsuit that the company paid to a customer. The company also paid bonuses to its top executives amounting to $1.7 million.

When normalizing the earnings for the year, the company will need to remove the two major costs since they are one-time costs. It means that the EBITDA for the year will increase by $4 million ($2.3 million + $1.7 million). After normalization, the earnings for the year will be $11 million.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: