Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The equity value of a company before it receives cash from a round of financing

Pre money valuation is the equity value of a company before it receives the cash from a round of financing it is undertaking. Since adding cash to a company’s balance sheet increases its equity value, the post money valuation will be higher because it has received additional cash.

It’s important to note that pre money valuation refers to the total equity value of the business, and not the share price. While the equity value is impacted by receiving additional cash, the share price will be unaffected. The example below will illustrate why that’s the case.

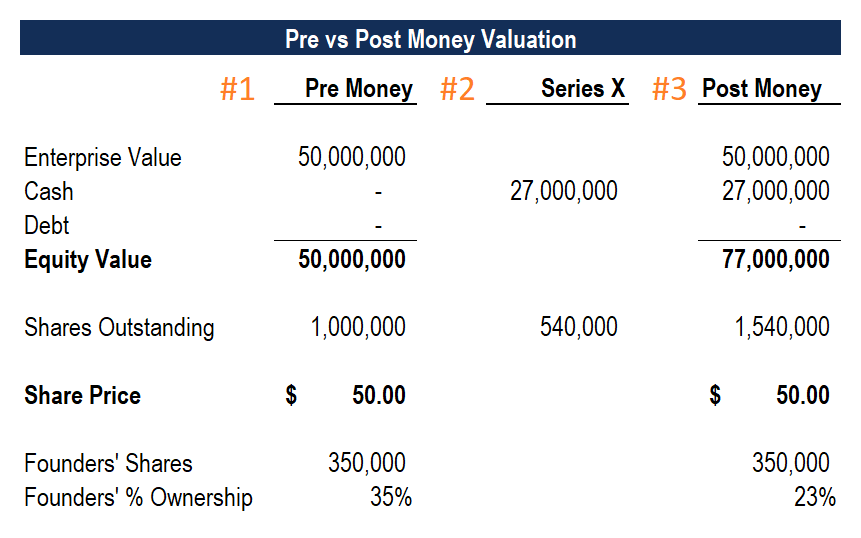

Below is a three-step example of the pre and post money valuation of a company undergoing a round of financing:

Below is a company that has a pre money equity value of $50 million. The company has one million shares outstanding, so its share price is $50.00.

The company is seeking to raise $27 million of equity at its pre money valuation of $50 million, which means it will have to issue 540,000 additional shares.

The company adds $27 million to its pre money valuation of $50 million for a post money valuation of $77 million. The company now has 1.54 million shares outstanding, so its share price is still $50.00.

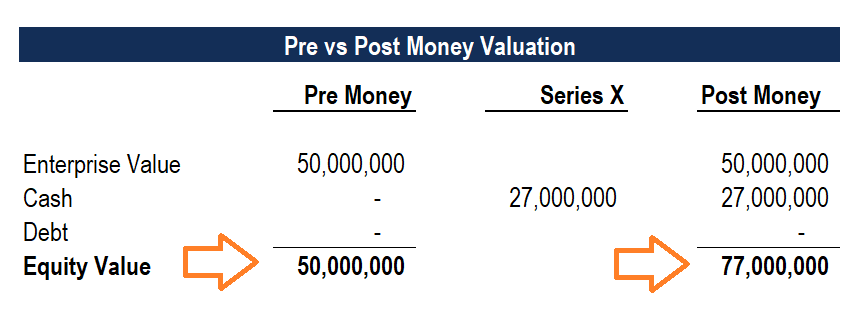

A company’s enterprise value (EV) is the value of the entire business without considering its capital structure. It’s important to point out that a company’s enterprise value is unaffected by a round of funding. While a company’s equity value increases by the amount of cash, its EV remains constant.

It’s important to point out that the existing shareholders (before the transaction) will have the ownership percentage diluted by issuing new shares. In the example we used above, the founders had 350,000 shares before the Series X, which represented 35% of the total shareholding. Post-transaction, they will still have 350,000 shares, but that will only represent 23% of the total. The value of their shareholding remains unchanged (350,000 x $50 = $17.5 million).

For early stage companies, the value of the cash that will be received from a round of financing can have a meaningful impact on the equity value of the business. It is why the phrase is so commonly used because a company could be looking at a dramatic change in its value.

When a company is undergoing a round of financing (i.e., Series X), it will have to negotiate with investors about the value of the company. It can be both an intense and subjective negotiation.

The most common valuation methods are:

To learn more about each of the above techniques, see CFI’s guide to valuation methods.

There is no single formula to calculate a company’s pre money valuation because it’s entirely subjective. What the business is worth may be a function of any of the three valuation methods outlined above.

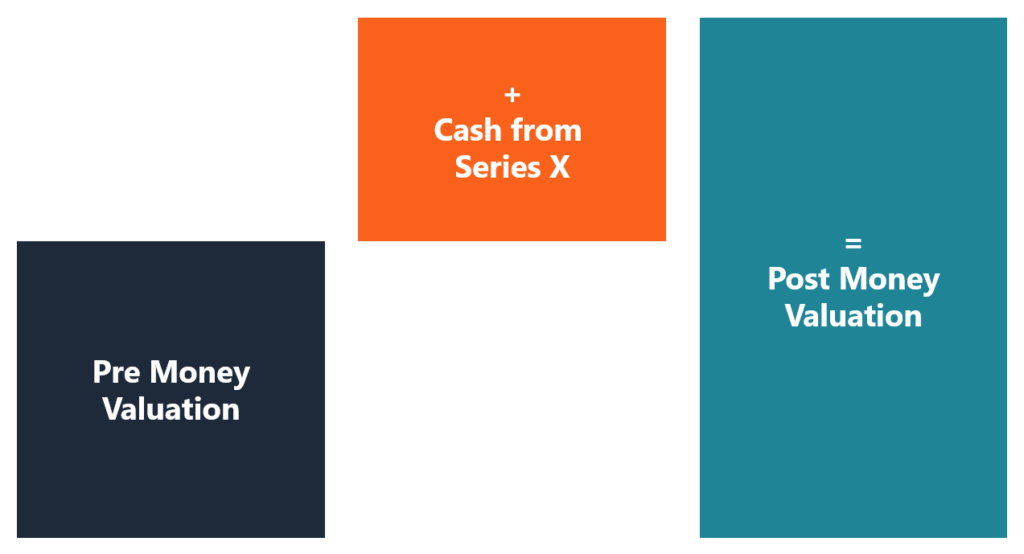

To calculate the post money valuation, use the following formula:

or,

Since the value of a company can be intensely debated, and since founders typically have very optimistic expectations for the business, Venture Capital (VC) firms will typically use preferred shares to “bridge the valuation gap.”

By receiving a preferred share (instead of common shares), VC firms get several advantages:

Since there is additional value in all of the above attributes, the VC firm’s preferred shares will be worth more than the common shares. It means they essentially get to buy preferred shares (which are more valuable) at a common share price (which are less valuable), making their investment returns more attractive.

Thank you for reading CFI’s guide to Pre Money Valuation. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: