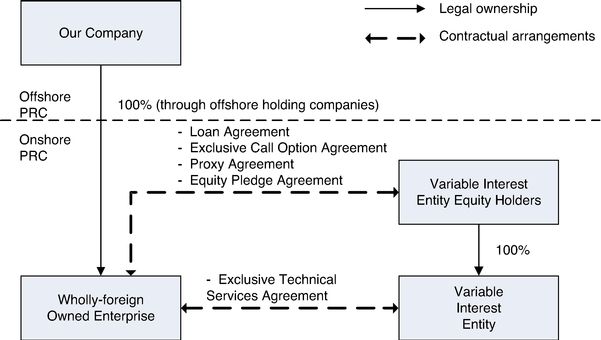

Variable Interest Entity (VIE)

Any type of legal business structure created to protect the business from legal action by its creditors

What is a Variable Interest Entity (VIE)?

A variable interest entity (VIE) may be any type of legal business structure. It can be, for instance, a trust, a partnership, a corporation, or joint venture. It is created such that even if an investor does not hold a majority of the voting rights, they are able to exercise a controlling interest in it.

A VIE is almost always created to protect a business from legal action by its creditors. It may also be an accounting structure wherein the equity investors are unable to finance the working capital needs or operating costs of the business.

An accounting entity is an established economic unit to isolate the accounting of a certain type of transactions from other divisions of a business entity. Such an accounting entity may either be a corporation, a subsidiary within a corporation, or sole proprietorship. The accounting entity is required to have a separate set of books that differentiates the assets and liabilities from those of the owner company or entity.

Summary

- A variable interest entity (VIE) may be any type of legal business structure created to protect the business from legal action by its creditors.

- A VIE may also be an accounting structure wherein the equity investors are unable to finance the working capital needs or operating costs of the business.

- Public companies are required to disclose their relationships with VIEs according to the accounting rules to be followed by corporations with respect to VIEs, as per the FASB.

Variable Interest Entity – Formation

A VIE is usually formed with a limited scope and purpose. For instance, a VIE may be established to finance a project – purchasing a large asset to lease it back to another entity without putting the entire business at risk. It is done by establishing special purpose vehicles that enable the company to hold financial assets passively or to conduct research and development activities actively.

Creating a VIE – Advantages

If done properly, a VIE can create a completely new risk category for the business. A less risky entity can bargain for credit at a lower rate of interest, drastically decreasing the cost of capital for new investments. A high-risk entity, on the other hand, can shield the company from higher liability.

Creating a VIE – Disadvantages

There exists a propensity to misuse structures such as VIE, for instance, to keep securitized assets off the balance sheets of corporates. Regulatory reforms that followed the 2008 global financial crisis sought to curtail the excessive use of asset-backed securities in the financial industry. However, due to lobbying efforts by banks, the Financial Accounting Standards Board (FASB) rules for VIEs were relaxed, which enabled banks to continue pouring debt in off-balance-sheet entities.

Variable Interest Entity – Disclosure Requirements

Public companies are required to disclose their relationships with VIE according to the accounting rules to be followed by corporations with respect to VIEs, as per the FASB. In a situation where the company owns a majority interest in a VIE, the holdings are to be disclosed in the consolidated balance sheet of the company. The consolidation is not mandatory in situations where the company is not the primary beneficiary of such an entity.

Companies are also mandated to disclose information regarding VIEs wherein they hold a significant interest. It may include information on how the entity operates, the sources and quantum of financial support it receives, and the kind of financial support received, among other contractual commitments. An estimation of the potential losses that could be incurred by the VIE may also be included.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional CFI resources below will be useful:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.