Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Earnings per Share (EPS) adjusted for mergers & acquisitions

Proforma earnings per share (EPS) is the calculation of EPS assuming a merger and acquisition (M&A) takes place and all financial metrics, as well as the number of shares outstanding, are updated to reflect the transaction. “Pro forma” in Latin means “for the sake of form.” In this case, it refers to calculating EPS “for the sake of form” in the event of the acquisition.

Basic EPS is calculated by dividing a firm’s net income by its weighted shares outstanding. The pro forma EPS, on the other hand, adds the target firm’s net income and any additional synergies or incremental adjustments to the numerator, while adding new shares issued due to the acquisition to the denominator.

(Source: Google Finance, Tesla)

Here is the formula for proforma earnings per share:

Proforma EPS is used by the acquiring company to determine the financial outcome they will have by acquiring the target or merging with the target. This also allows the acquirer to determine whether this transaction will be accretive or dilutive and cause a positive effect on their EPS.

Note that simply analyzing an acquisition or merger on the basis of EPS is not recommended, as there are situations where EPS can increase, but the value of the merged firm is lower than the sum of the acquirer and target.

These are additional value items that are created when the two firms combine, which impact proforma earnings per share:

For example, a manufacturing company merges with a transportation firm. Due to this merge, the manufacturing firm can save on their original distribution costs, which were initially paid out to a third party. Because they can now use the assets of the transportation, they realize after-tax savings of $50M. The incremental adjustment here is an after-tax synergy arising from those savings of $50M, which did not originally exist when the firms were separate.

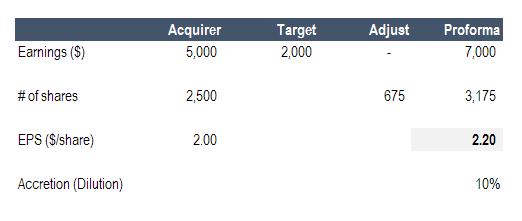

Here is a simple example of how to calculate proforma earnings per share (EPS) in an M&A transaction.

Here is a breakdown of what’s happening in the table above:

Enter your name and email in the form below and download our free Proforma EPS template now!

We hope this has been a helpful guide to calculating Proforma Earnings per Share (EPS). To keep expanding your knowledge and complete your quest of becoming a world-class financial analyst, these additional resources may be helpful: