Overview

Math for Finance Professionals Course Overview

Financial math is a critical tool for people working in the finance industry. Professionals within the industry need the skills to analyze financial data, manage financial risks, assess investment opportunities, and monitor transactions.

This course will provide you with the foundational math skills required to build a career in finance. You will compare simple and compound interest and learn how these different types of interest are used to compound and discount cash flows. You will also be introduced to the concepts of nominal and effective interest rates. You will then be ready to apply these skills to a variety of real-world finance applications.

Who Should Take Math for Finance Professionals Course?

This course is specifically designed for finance professionals seeking careers in investment banking, capital markets, risk management, investment and wealth management, finance, and accounting.

Math for Finance Professionals Learning Objectives

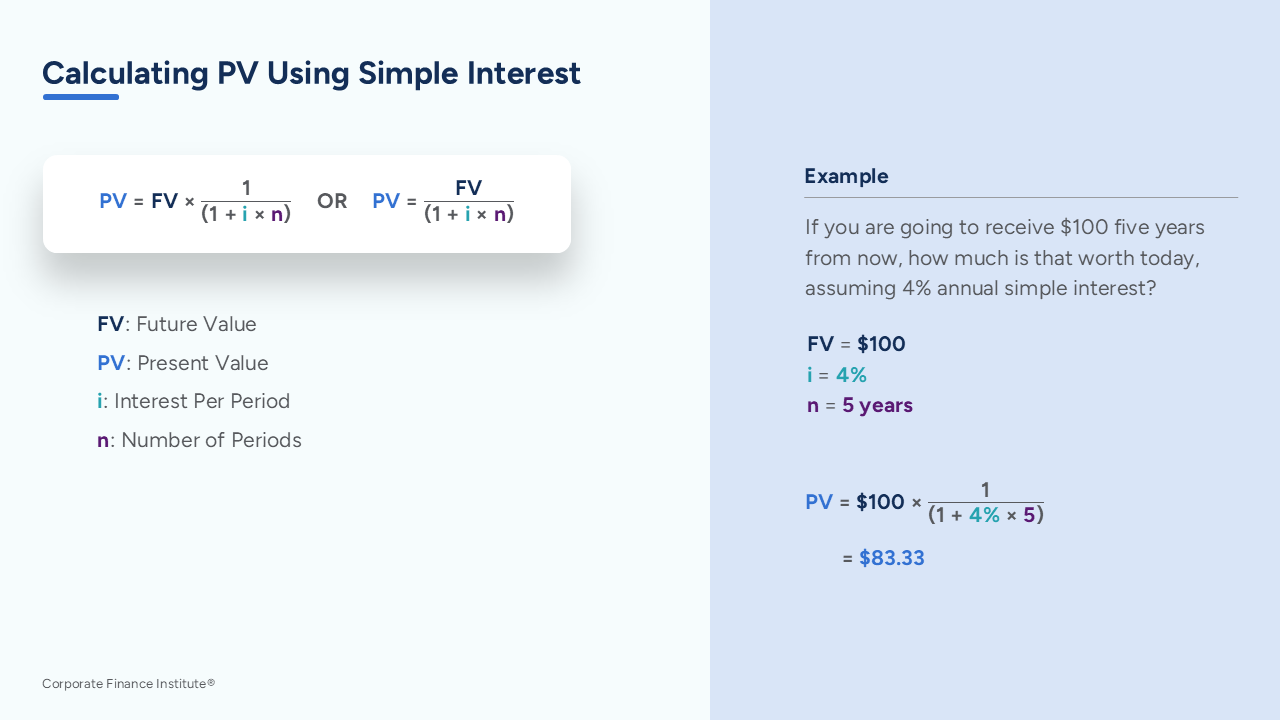

- Explain the difference between simple and compound interest

- Calculate and compare effective and nominal interest rates

- Build a range of discounted cash flow models that represent real-world applications

Prerequisite Skills

Recommended skills to have before taking this course.

- Basic Math

Level 2

1h 46min

100% online and self-paced

Field of Study: Finance

Start LearningWhat You'll Learn

Simple and Compound Interest

Nominal and Effective Interest Rates

Discounted Cash Flows

Course Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Financial Modeling & Valuation Analyst (FMVA®) Certification

- Skills Learned Financial modeling and valuation, sensitivity analysis, strategy

- Career Prep Investment banking and equity research, FP&A, corporate development

Capital Markets & Securities Analyst (CMSA®) Certification

- Skills Learned Trading strategies used in the finance and capital markets

- Career Prep Work in capital markets, whether on the buy-side or the sell-side

Financial Planning & Wealth Management Professional (FPWMP®) Certification

- Skills Learned Financial Learning, Business Development, Investment Management, Practice Management, Relationship Management

- Career Prep Financial Planner, Investment Advisor, Portfolio Manager

Risk Management Specialization

- Skills You’ll Gain Risk Identification, Regulatory Analysis, Risk Measurement, Risk Mitigation

- Great For: Market Risk Analyst, Credit Risk Analyst, Compliance Officer, consulting, Enterprise Risk Manager, Audit