Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Cash EBITDA incorporates a company’s YOY change in deferred revenue to give a more accurate picture of its financial position

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is one of the most frequently used metrics in finance. Across the finance industry, investment bankers, buy-side and sell-side analysts, valuation experts, company managers, and other professionals use EBITDA to compare a company’s financial performance relative to industry peers and assess its profitability at the core business level.

By removing the impact of capital structure and taxation, EBITDA supports a view of the underlying profitability of a company and is often used in valuation ratios. Analysts can make additional adjustments to core EBITDA based on the types of comparisons they wish to make. Cash EBITDA is a variant often used for valuation purposes.

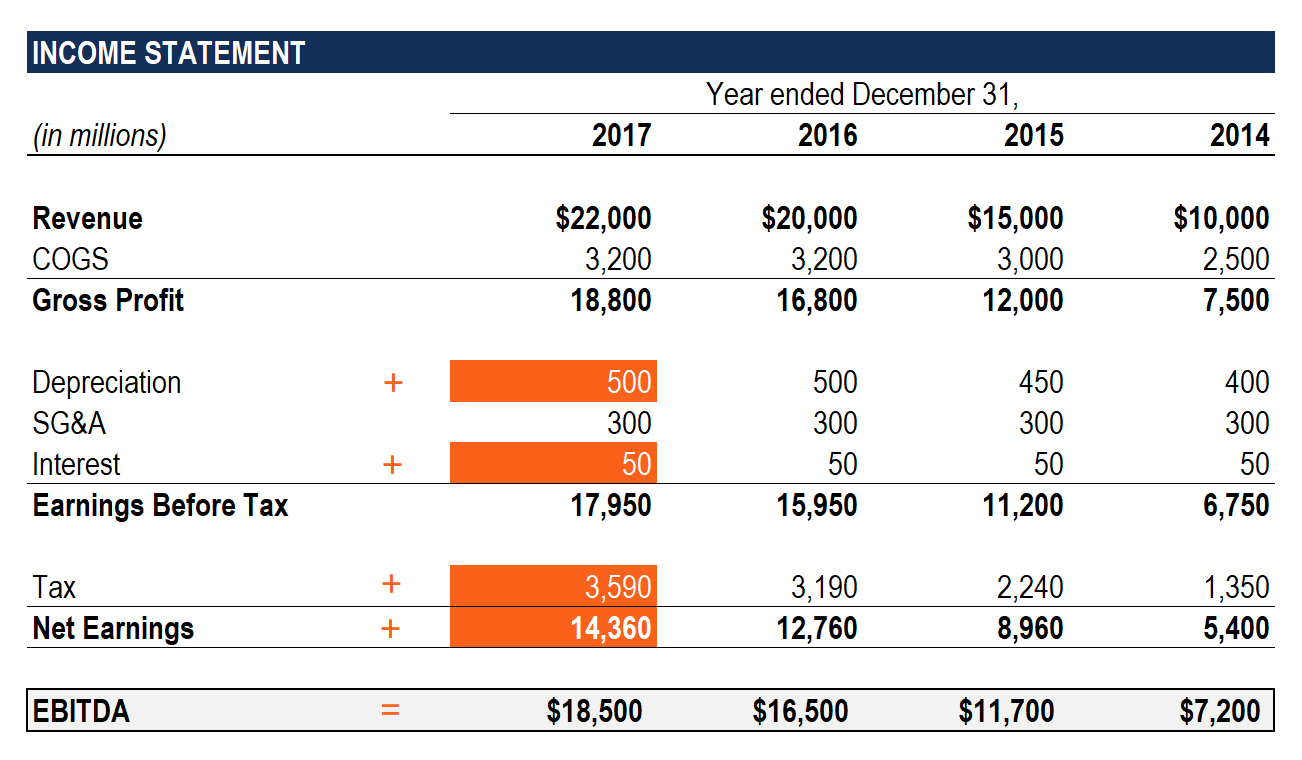

When you want to know how profitable a company is, you might look at its income statement. Net income seems like a pretty good indicator, but it’s not entirely helpful when you want to compare one company against another or against a group of industry peers.

Companies aren’t all the same; they may have different tax profiles, capital structures, and capitalization policies, all of which have an impact on net income. To compare apples with apples, analysts need to be able to compare companies on a common financial basis, using information that is readily available from a company’s published financial statements.

EBITDA offers analysts an alternative to net income for assessing profitability. EBITDA takes net income and adds back non-cash expenses like depreciation and amortization, as well as taxes and interest costs, which are determined by capital structure.

While EBITDA might not be recognized under generally accepted accounting principles (GAAP), many companies report both EBITDA and adjusted EBITDA figures since they are widely used in analysis.

Although EBITDA is an extremely popular metric, there are concerns regarding its use. Some suggest that it overstates profitability. In the spirit of full disclosure, the U.S. Securities and Exchange Commission (SEC) requires companies that report EBITDA to show how the metric is derived. Reporting EBITDA on a per-share basis is not allowed.

Some analysts also believe that EBITDA ignores the cost of assets in assessing profitability. Since EBITDA tends to show profitability in a better light, companies that are borrowing heavily and want to downplay that fact may also highlight EBITDA. For example, two companies may have the same EBITDA, but one is highly levered while the other is debt free.

Similarly, EBITDA viewed in isolation does not provide any insight into changes in a company’s working capital, or reinvestment into the business through capital expenditures. In any analysis, it’s vital to review the information provided by the financial statements, including the statement of cash flows and footnotes, to understand all the factors at play.

Calculating EBITDA is straightforward. Net income, tax expense, and interest expense are all found on the income statement. Depreciation and amortization might require a bit more digging but will typically be found on the cash flow statement or in the footnotes to the financial statements. Once you have these figures, calculate as follows:

As a shortcut, you can use earnings before interest and taxes (EBIT, also known as operating income) from the income statement and add back depreciation and amortization.

When considering EBITDA for a merger or acquisition, or for raising capital, valuation can often be based on an EBITDA multiple. Since the underlying goal is to understand core profitability, the analyst wants to normalize the metric and make it as “clean” as possible. It means adjusting EBITDA by adding back unusual or non-recurring expenses. Some of the adjustments might include:

While EBITDA involves adding back interest, taxes, depreciation and amortization, adjusted EBITDA might involve some subtraction as well. For example, an inflow from a one-time sale of assets would be subtracted from operating income. Now, the formula becomes:

Remember, since EBITDA in all its variations is a non-GAAP metric, keep careful track of the sources for all your adjustments and be ready to justify the calculations.

Some types of companies frequently book deferred revenue, which is money received in advance for products or services that will be delivered in the future, with revenue only being recorded in the income statement when delivery occurs. This occurs when a customer prepays for something, for example, a software subscription.

Since the company has not yet delivered the service or product, the prepayment is recorded under deferred revenue as a liability and then recognized as income over a specified period of time.

When calculating cash EBITDA, the formula is only slightly more complicated. First, calculate the 12-month trailing (TTM) EBITDA. Next, add the year-over-year change in deferred revenue, which should be taken from the balance sheet.

Say, for example, that a company adds a new customer in the first quarter of the year. In any valuation discussion, if the full impact of the new customer is not accounted for, the company would be undervalued.

That’s why it’s important to use cash EBITDA for the valuation in any transaction involving a business that records significant prepayments and deferred revenue.

EBITDA is a ubiquitous metric in many different aspects of finance as it makes it possible to analyze companies in the same industry, or across industries, on a more directly comparable basis.

Adjusting EBITDA for varying unique factors that apply to a business adds relevance to any valuation. The adjustment to cash EBITDA can be very significant for valuing companies in particular industries.

However, in every circumstance, it’s vital to look not only at how adjusted and cash EBITDA are calculated but to understand the many factors that can impact a company’s true value and profitability. EBITDA is a valuable tool, but not a one-size-fits-all solution to valuation and profitability.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.