Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Describes stock performance through market risk and outperformance of small-cap companies and high book-to-market companies

The Fama-French Three-Factor Model is an extension of the Capital Asset Pricing Model (CAPM). The Fama-French model aims to describe stock returns through three factors: (1) market risk, (2) the outperformance of small-cap companies relative to large-cap companies, and (3) the outperformance of high book-to-market value companies versus low book-to-market value companies. The rationale behind the model is that high-value and small-cap companies tend to regularly outperform the overall market.

The Fama-French Three-Factor Model was developed by University of Chicago professors Eugene Fama and Kenneth French.

In the original model, the factors were specific to four countries: the U.S., Canada, Japan, and the U.K. Subsequently, Fama and French adjusted the factors, making them applicable for other regions, including Europe and the Asia-Pacific region.

The mathematical representation of the Fama-French Three-Factor Model is:

Where:

Market Risk Premium

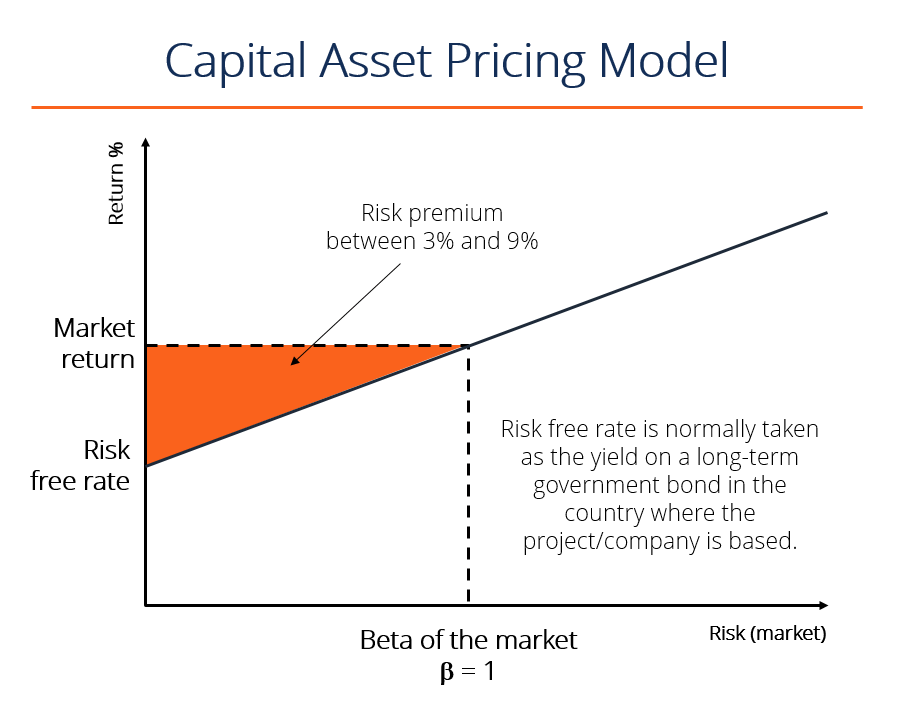

Market risk premium is the difference between the expected return of the market and the risk-free rate. It provides an investor with an excess return as compensation for the additional volatility of returns over and above the risk-free rate.

Small Minus Big (SMB) is a size effect based on the market capitalization of a company. SMB measures the historic excess of small-cap companies over big-cap companies. Once SMB is identified, its beta coefficient (β) can be determined via linear regression. A beta coefficient can take positive values, as well as negative ones.

The main rationale behind this factor is that, in the long-term, small-cap companies tend to see higher returns than large-cap companies.

High Minus Low (HML) is a value premium. It represents the spread in returns between companies with a high book-to-market value ratio (value companies) and companies with a low book-to-market value ratio. Like the SMB factor, once the HML factor is determined, its beta coefficient can be found by linear regression. The HML beta coefficient can also take positive or negative values.

The HML factor reveals that, in the long-term, value stocks (high book-to-market ratio) enjoy higher returns than growth stocks (low book-to-market ratio).

The Fama-French Three-Factor Model is an expansion of the Capital Asset Pricing Model (CAPM). The model is adjusted for outperformance tendencies. Also, two extra risk factors make the model more flexible relative to CAPM.

According to the Fama-French three-factor model, over the long term, small companies outperform large companies, and value companies beat growth companies. The studies conducted by Fama and French revealed that the model could explain more than 90% of diversified portfolios’ returns. Similar to the CAPM, the three-factor model is designed based on the assumption that riskier investments require higher returns.

Nowadays, there are further extensions to the Fama-French Three-Factor Model, such as the four-factor and five-factor models.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the Fama-French Three-Factor Model. To keep learning and advancing your career, the following CFI resources will be helpful: