Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A valuation method used to determine the appraisal value of a business

The market approach is a valuation method used to determine the appraisal value of a business, intangible asset, business ownership interest, or security by considering the market prices of comparable assets or businesses that have been sold recently or those that are still available. Price-related indicators like sales, book values, and price-to-earnings are usually utilized.

Image: CFI’s Business Valuation Course.

Regardless of the asset under valuation, the market approach looks at the prices of comparable assets and makes proper adjustments for different quantities, qualities, or sizes. For instance, when you want to determine the value of a share of stock, you should look at the recent selling price of shares of stock that are similar. Since ownership shares of a company are usually identical, the recent selling price of the shares will provide a good estimation of their fair value.

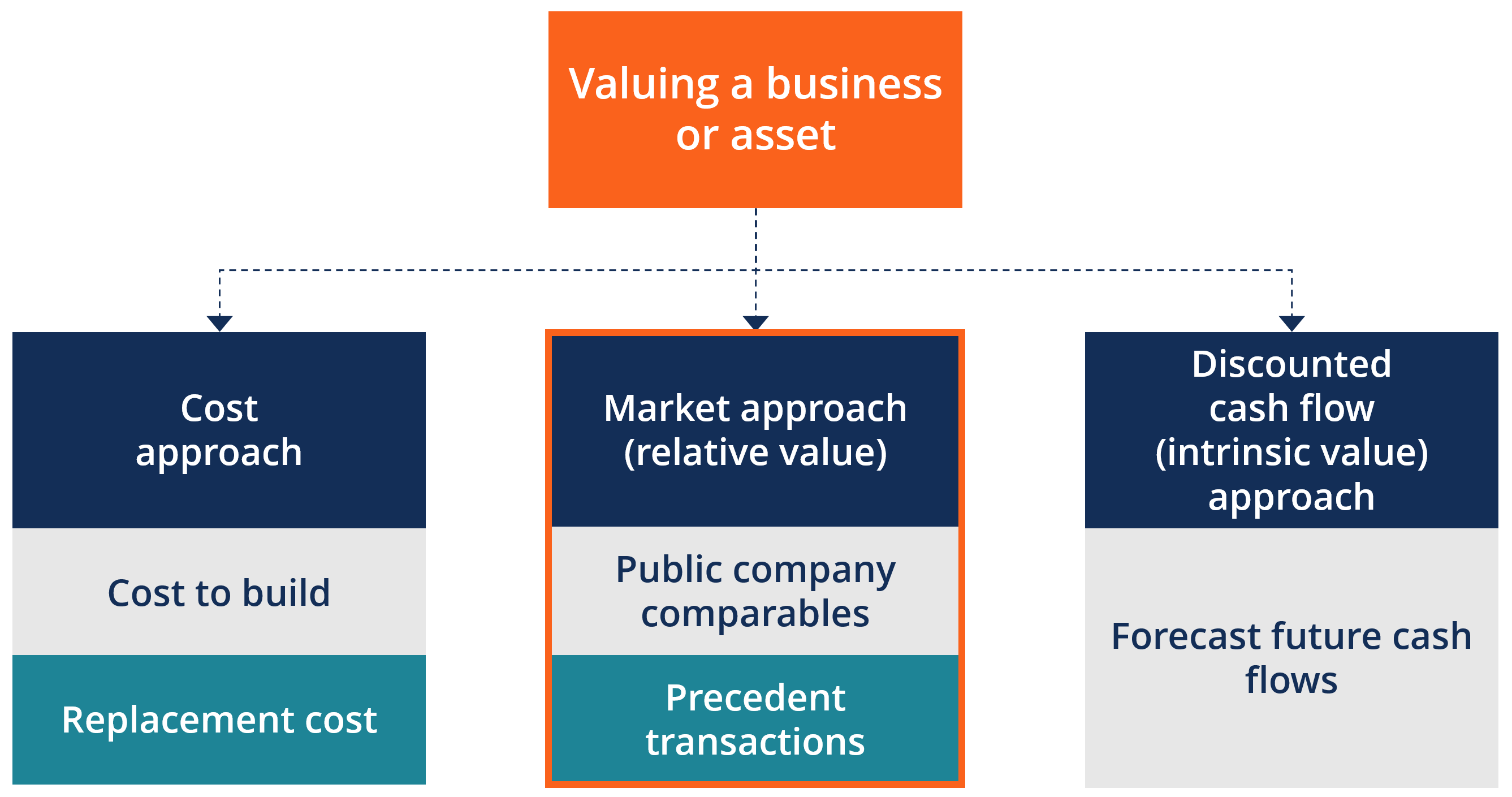

The above-mentioned business valuation method is also referred to as the market comparison approach or the market-based approach. It is one of the three valuation methods used to estimate the value of an entity. The other two include the Income Approach (Intrinsic Value or DCF Analysis) and the Cost Approach.

There are a number of valuation methods that may be used by a valuation analyst under the market approach. The methods are named according to the source of known values that are used as guidelines. The two main valuation methods that are used under the market approach are:

The Public Company Comparables Method entails using valuation metrics from companies that have been traded publicly, which are considered to be rightly similar to the subject entity. In most situations, direct comparability is hard to attain since a majority of public companies are not only larger but also more dissimilar to the subject.

Nonetheless, the direct comparability threshold should be a little flexible so that public companies that have comparable business features are not excluded from giving guidance on the subject company’s valuation.

Direct comparability can be readily achieved in comparatively few industries. Most of them are faced with challenges of scalar differences existing between most private enterprises and public operators. The process of selecting, adjusting, and applying public company valuation data is usually complex and needs significant experience and appraiser skill.

Guideline companies are usually companies that have been traded publicly in a similar or equivalent industry as the subject company. They should also have a practical basis for comparison to the subject of evaluation because of resemblances in demand and supply factors, operational processes, and financial composition.

The Precedent Transactions Method involves deriving value using pricing multiples that are based on observed transactions of companies in the industry of the subject company. It is based on the perception that comprehensive company financial data is not easily available, but there is an availability of transaction value.

Precedent transactions can be analyzed through conventional industry classification methods, like SIC codes. Furthermore, there are also valuation databases that can be examined for evidence of historical actuals and valuation. Such transactions may represent a majority or a minority perspective. A good guideline transaction should be from a very comparable company in the same industry. In cases where there is no direct comparability, other data can be used but not before considering such things as their market or products.

The use of the Transaction Method can be valuable in cases where a purchase or sale is under consideration or as an exit strategy for the management of the company. One weakness though is that some transactions may have happened in significantly diverse markets or industry conditions and therefore may not represent the prevailing acquisition and merger environment. Moreover, a major challenge in finding out if a transaction is suitable enough to be used as comparable data is the lack of information in the public spectrum or in research databases.

In both market valuation methods discussed above, the key is searching for companies that are sufficiently comparable to the subject company under valuation. When trying to find out whether a company is comparable enough to be used in determining the value of the other company, the appraiser should consider a number of factors such as:

All methods under the Market Approach come with their own advantages and disadvantages. However, as a whole, the Market Approach offers the following benefits and weaknesses:

Determining the value of your business using the market approach is particularly suitable in the following situations:

The market approach as a valuation method is used to find the value of a business by comparing it to other similar businesses that have sold recently. The two commonly used market approach methods are the Public Company Comparables and Precedent Transactions. These methods both assess the value of a business through the application of several ratios of value to financial metrics or non-financial parameters of companies traded publicly or market transactions.

For the market approach to be successful, it is critical to ensure that all companies being used for comparison are similar to the subject company or that premiums and discounts are applied for divergent features. Moreover, the market approach can only work effectively if the number of other similar businesses to compare with is adequate. For this reason, it is difficult to assign a value to a sole proprietorship purely on the basis of market value.

Since sole proprietorships are owned by individuals, trying to get public information on previous sales of similar businesses is a very hard task. It is important to consult a professional to offer you help with assessing the true value of your asset or business.

Thank you for reading CFI’s guide to Market Valuation Approach. To keep learning and advancing your career, the following resources will be helpful: