A-B Trust

An estate planning tool that married couples use to minimize estate taxes

What is an A-B Trust?

An A-B Trust is an estate planning tool that married couples use to minimize estate taxes. Essentially, when the first spouse dies the trust is split into two portions – an “A” part and a “B” part. The “A” part of the trust is the assets of the surviving spouse (also called the Survivors Trust) and the “B” part is the assets of the deceased spouse (also called the Bypass Trust). The A-B Trust is created when each spouse places assets in the trust and names a final beneficiary (who is any suitable person that is not the other spouse).

Purpose of A-B Trusts

The A-B Trust allows spouses to provide for the surviving spouse, as well as protect the estate tax (the “death tax”) exemption. In Canada, everyone is entitled to a combined federal gift tax and estate tax exemption of $5.43 million, so A-B Trusts attempt to combine the exemptions between married couples (i.e., $10.86 million in exemptions). The A-B Trust structure can also protect the assets of a deceased spouse so they transfer to the original beneficiary and cannot be tampered with by the surviving spouse.

How It Works

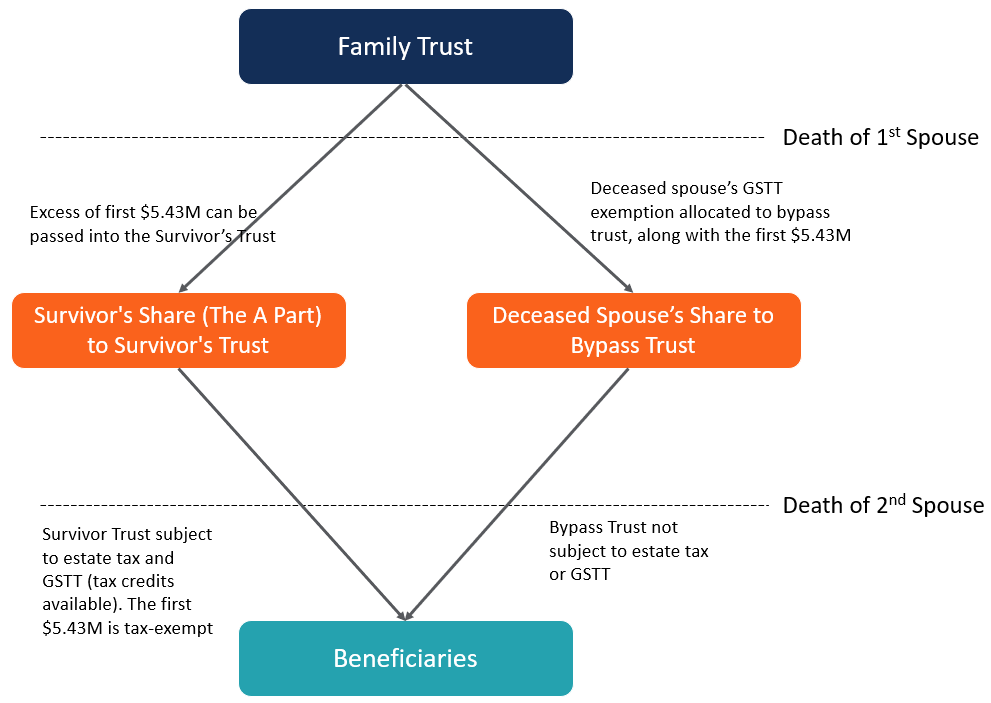

An A-B Trust is structured to maximize the tax exemption of both spouses’ estates. Below is a diagram that provides an overview to explain how an A-B Trust works:

Explanation

1. Married couples include the appropriate A-B Trust language in their last will and testaments or revocable living trusts with the assistance of an estate planning attorney.

2. The couple divides their assets, so each couple lists the same value of assets in their individual names. It is essential to making the A-B Trust structure.

3. When the first spouse dies, the first $5.43 million would be funded into the “B” trust or the Bypass Trust. The residual value of the trust will be placed in the “A” Trust. It defers the payment of estate taxes on the assets of the deceased spouse through the unlimited marital deduction rule.

4. When the surviving spouse dies, they will still receive their tax exemption from estate taxes. The first $5.43 million from the “A” portion will be tax-exempt, plus any “B” tax exemption that the first spouse had remaining.

5. The assets from the “B” portion will pass through to the final beneficiary tax-free. It is because the “B” Trust used the federal estate tax exemption when the first spouse died.

Advantages of A-B Trusts

Creating an A-B Trust comes with a few benefits, including:

1. Death tax exemptions

When an individual dies, their estate must be settled – it includes paying the “death tax.” In an A-B Trust, the “A” part or Survivors Trust is the only portion of the trust that is subject to the “death tax.” As a result, the trust will pay less in taxes than a simple trust.

2. Portability of exemption

In December 2011, the U.S. allowed the “A” portion to acquire the residual “death tax” exemption from the deceased spouse. It effectively raised the exemption amount, so most estates do not need to pay any taxes.

3. Inherent trust protection

In the off-chance that there are some internal family issues (maybe a spouse decides to run away to the Bahamas), the “A” portion of the trust can be transferred, but the “B” portion cannot. It provides a guarantee to the original beneficiary that they will receive the assets that were promised to them.

Disadvantages of A-B Trusts

There are also some disadvantages that are inherent to an A-B Trust, specifically:

1. Maintenance cost after the first death

After the first spouse dies, income tax returns will need to be filed for both portions of the trust. To accomplish it, the surviving spouse should compile financial reports for the trust and will usually include associated fees to accomplish this (i.e., an accountant fee).

2. More complicated than a simple trust

Instead of including one account, the trust will be split into two accounts. It makes keeping track of certain items more difficult.

3. After the second death, large capital gains taxes could apply

Even though “Death Tax” exemptions exist, both portions of the trust are still subject to capital gains taxes. It can create unwanted complexities and costs.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: