Accumulation Phase

The time in the life cycle of an investment when an individual or an investor builds up the value of their annuity or investment

What is the Accumulation Phase?

The accumulation phase refers to the time in the life cycle of an investment when an individual or an investor builds up the value of their annuity or investment. It is the second phase in the process of investing.

The fundamental principle at work that makes it possible is the concept of delayed gratification and time value of money, where one foregoes immediate consumption today for amassing a larger payout at a later date in the future. The interest earned on the cash flows foregone in the present compounded over time can yield significant value for the individual, which can be used during the next phase (the annuitization phase or the distribution phase) of the investment.

Summary

- The accumulation phase is the second phase in the investment phases: planning, accumulation, distribution, and legacy.

- The accumulation phase presents a lot of control in some key aspects of investing.

- Typically, the accumulation phase is the longest part of the investment lifecycle, spanning over 35-40 years and making it important to have a solid strategy in place.

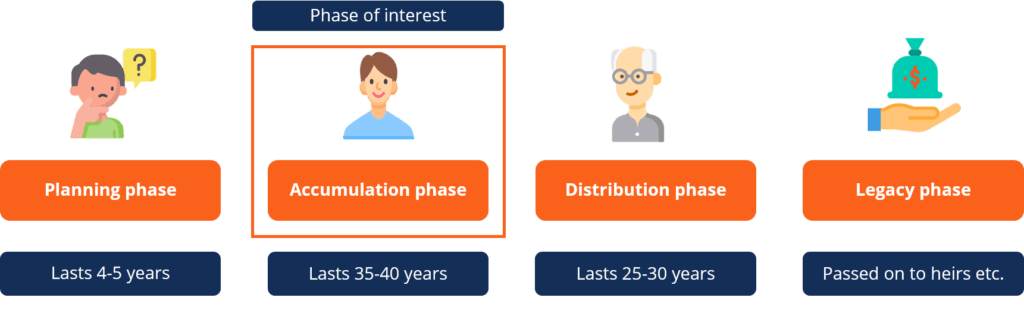

Investment Phases

The investment phases typically include the planning phase, the accumulation phase, the distribution phase, and the legacy phase. Most of the cash inflows into the investment pool happen during the accumulation phase.

1. Planning phase

The planning phase sets the stage for understanding the options available to the investor in terms of security selection, investment options, budgeting, and goal-setting as per their individual needs. It is where the investor becomes aware of their investment needs, and financial planners engage with new clients.

2. Accumulation phase

Accumulation phase brings to life the planning done in the planning phase and is the longest phase in an investor’s life cycle.

3. Distribution phase

The distribution phase is triggered upon retirement or in the years leading to the retirement of the individual.

4. Legacy phase

The legacy phase is typically one of the most ignored sections of personal financial planning. However, sophisticated investors work backward and try to attain their legacy and retirement goals by focusing more on the accumulation phase.

Importance of the Accumulation Phase

Investors who understand their consumption needs for today and the future can make the most of the accumulation phase as they grow their investments to an amount that can be valuable when their income levels decline. It is evident in the lives of many people that income levels are higher for most people before their retirement, after which consumption levels are higher than income levels.

Most people who start investing early on in their lifetime effectively utilize the time in the accumulation phase, making it possible to amass a relatively larger sum of money than people who start later in their life. The fact highlights the underlying importance of investing from as early on as possible and makes it possible to grow investments by relying on compound interest accumulation.

Unlike the annuitization phase (distribution phase) of the investment, which may be unpredictable in length and may fail to capture consumption estimates accurately, the accumulation phase typically is of fixed duration and is less variable for the average individual investor.

Real-World Example of the Accumulation Phase

Assuming an individual begins to save at age 25, the accumulation phase can be 35-40 years, depending on when the individual chooses to retire. Most people retire around 60-65 years, and the average life expectancy is 85-90 years in most developed economies of the world, leading to a 25-30 years period of distribution.

Investors can be better positioned by focusing on effective investment strategies during the accumulation period in order to receive a better payout at the end of the phase. The accumulation phase is analogous to laying out the foundation of the building, and the portfolio growth is contingent on how well it is laid out.

Investment Framework

A lot of investors use an investment framework to inform the decision-making process over time. Before an Investment Policy Statement (IPS) is formulated, it is important to get a deeper understanding of all the variables that may apply to an investor.

There are several key consideration variables in setting up an investment policy statement, and some variables may hold higher weightage compared to others depending on the stage of life the investments are being made.

The IPS can be a guidance framework to assist in identifying the right performance metrics, as well as investment opportunities that might work for a particular investor.

Additional Insights

It is worth noting that the accumulation phase indirectly dictates how large the final investment will be, and it inherently determines the size of the payments that can be drawn out of the sum once it’s been accumulated. It is very important to make logical investment decisions at such a time, as a lot of variables in the accumulation phase are in control of the investor.

The risk tolerance, income level, and time remaining for making investments keep declining over time with more expertise building. Thus, a sophisticated investor must aim to factor all the variables depending on which stage of the investment life cycle they are in.

More Resources

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: