Money Market Funds

Open-ended fixed income mutual funds that invest in short-term debt securities

What are Money Market Funds?

Money market funds are open-ended fixed income mutual funds that invest in short-term debt securities, such as Treasury bills, municipal bills, and short-term corporate and bank debt instruments that come with low credit risk and emphasize liquidity.

Understanding Money Market Funds

Money market securities typically come with maturities under 12 months. The short-term nature of the securities is a way of reducing risk and uncertainty. The selection of money market investments is performed by a fund manager as it should relate to the type of money market fund. Money market funds are not insured by the federal government (FDIC), unlike money market accounts, which are insured.

Money market mutual fund income is usually in the form of a dividend; it can be taxed or tax-exempt depending on the nature of securities invested in the fund. The funds can be used as a cash management tool in business because of their liquidity and flexibility, hence their popularity.

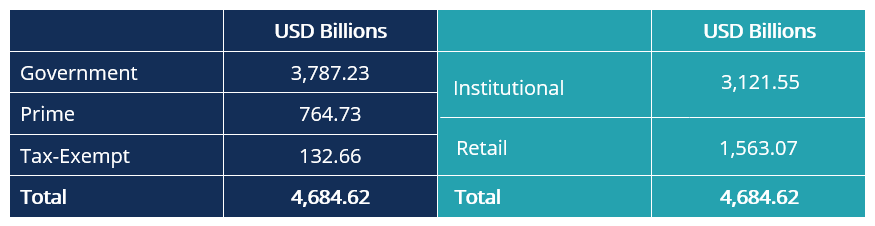

Money market funds were developed and came into use in the 1970s. They are regulated through the Securities and Exchange Commission (SEC) under the Investment Company Act of 1940 in the United States and Regulation 2017/1131 in Europe. According to the Investment Company Institute, money market funds total $4.68 trillion, as of June 17, 2020, and are distributed as follows:

Objectives of Money Market Fund Investments

Investors take part in money market funds for the following reasons:

- Short-term investment horizon

- Low conservative risk appetite with preference to low-security volatility

- High liquidity needs

- Low returns, which is compensated by low risk

- Stability and certainty

Types of Money Market Funds

The Securities and Exchange Commission (SEC) regulations comprise three categories of money market funds based on the securities in the fund:

1. Government

The funds invest in about 99.5% in government-backed securities such as U.S. Treasury bills, collateralized U.S. Treasury securities, repurchase agreements, and Federal Home Loan securities. They also invest in government-sponsored enterprises (GSE) securities, such as Freddie Mac and Fannie Mae. Since government-backed paper is “risk-free,” the funds are considered very safe.

2. Prime

They are funds invested in short-term corporate debt instruments, such as commercial paper, corporate notes, and short-term bank securities (banker’s acceptances and certificates of deposits). They also include repurchase and reverse repurchase agreements.

3. Municipal tax-free

The money market funds are predominantly invested in securities issued by municipalities, which are federal and often state income tax-exempt securities. Other entities also issue securities with tax protection, which the money funds also participate in, such as state municipal.

Benefits of Using Money Market Funds

1. Liquidity

The redemption of a money market fund usually takes less than two business days, and it is fairly easy to settle brokerage account investment trades.

2. Risk management

Money market funds act as a risk management tool, as funds are invested in cash equivalent securities with low risk and high liquidity.

3. Short-term

The short-term nature of money market funds ensures a low interest rate, credit, and liquidity risk.

4. Security

Money market funds invest in low-risk and high-credit quality securities, ensuring high security.

5. Stability

Money market funds are low volatility investments.

6. Convenience

Easy access to funds through a checking account linked to an income-yielding money market investment fund.

7. Diversification

Money market funds usually hold a diversified portfolio of government, corporate, and tax-free debt securities.

8. Tax exemption

Municipal issues in which money market funds invest in are federal and often state income tax-exempt; hence they provide tax-efficient income.

Money Market Fund Risks

1. Credit risk

Money market securities are susceptible to volatility and are not FDIC-insured, hence the potential to not lose money, however low, is not guaranteed. There exists a probability of loss, although it is generally quite small. There is no guarantee that investors will receive $1.00 per share on the redemption of their shares.

2. Low returns

The low returns of money market funds are usually lower than other funds comprising of assets such as stocks and properties. There is a chance that money market returns may also fall below the inflation rate, providing negative real returns to investors (inflation risk). Interest rates can also go down further, reducing returns on money market investments.

3. Liquidity fees and redemption gates

It involves the imposition of high liquidity fees, i.e., fees levied on the sale of shares. Redemption gates require waiting periods before redeeming proceeds from money market funds, normally implemented to prevent a run on the fund in periods of market stress.

4. Foreign exchange exposure

This risk is borne by funds that invest in money market instruments across borders that are denominated in other currencies other than the home currency.

5. Environmental changes

Changes in economic policies and government regulations can result in an adverse impact on the price of money market securities and their issuers’ financial standing, i.e., if they affect interest rates and money supply.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: