Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A type of individual retirement account that a holder funds with no tax deduction and makes tax-free withdrawals while being retired

A Roth IRA refers to a type of individual retirement account that a holder funds with no tax deduction and makes tax-free withdrawals while being retired. The IRA contains investments in bonds, stocks, certificates of deposit, and other securities. It was first proposed in 1989 by Oregon Senator Robert Packwood and Delaware Senator William Roth and was established in 1997.

Contributions made to a Roth IRA are not tax-deductible, which means that the account holder funds with the after-tax income. Gains from the investment of the Roth IRA are tax-free, and the account holder can withdraw without paying any income taxes. After keeping the IRA account for at least five years and at the age of 59½ or above, the individual can withdraw from his account without paying any penalty.

An individual who meets the income and other requirements can open a Roth IRA with an IRS-approved institution, including banks, brokerage firms, loan associations, and so on. The individual can then fund the account continuously, and the money funded will be invested in securities to generate earnings. A Roth IRA can be a self-directed IRA, for which the account holder can make decisions on investment by himself.

There are several limitations to the eligibility for a Roth IRA. One of these is income restriction. According to the International Revenue Service (IRS), the limit for the tax year of 2019 is a modified adjusted gross income (MAGI) below $137,000 (filing as a single person).

There is also an upper limit for the amount of contributions that can be made annually. In 2019 and 2020, the limits for the traditional and Roth IRA are the same: up to $6,000 for those under age 50 and up to $7,000 for those at and above age 50.

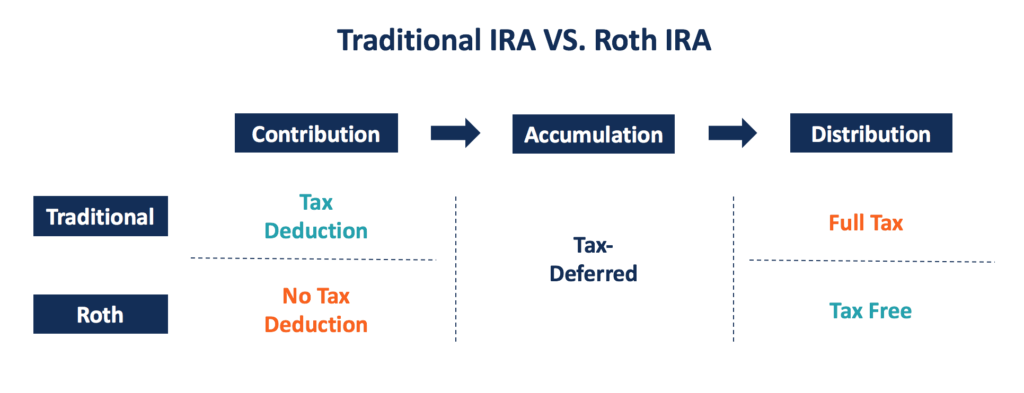

The other type of IRA offered by the U.S. government is the traditional IRA. Roth IRAs share many similarities with traditional IRAs, but different tax rules and limitations are applied to them by the IRS.

In terms of similarities, both traditional and Roth IRAs are tax-advantaged and can be self-directed. The minimum age to withdraw without penalty is 59½. Also, there is an upper limit on the amount of contributions that can be made annually for both types.

In terms of the differences, the most fundamental one is their taxes. The contributions are tax-deductible for a traditional IRA but not for a Roth IRA, but the withdrawals from a traditional IRA are taxed, while those from a Roth IRA are tax-free. Such a major difference makes it important for individuals to understand their current and forecasted future tax rates to choose between these two types of accounts.

If an individual’s current marginal tax rate is higher than the future marginal tax rate, then he/she should open a traditional IRA to get more dollar amounts of tax deduction. If an individual’s future marginal tax rate is forecasted to be higher than the current rate, then he/she should go for a Roth IRA for better tax benefits.

In addition to the tax structure, there are other differences regarding the limitations between the two IRA types. As mentioned above, there is a maximum income restriction for eligibility for a Roth IRA. It does not apply to a traditional IRA, which is available to everyone regardless of their income level.

A traditional IRA holder must withdraw annually after the age of 70, and the withdrawals must be above the required minimum distributions (RMD). A Roth IRA holder is not subject to these withdrawal restrictions. The individual can continue to make contributions even above age 70.

Besides the tax benefit, there is no minimum dollar amount of annual withdrawal required. RMD is applied against the situations that someone might use a retirement account to avoid taxes. Since a Roth IRA does not offer any tax deduction for contributions and is tax-free at the distribution stage, the RMD limitation is no longer necessary for a Roth IRA.

Roth IRAs don’t come with age limits. Account holders can make contributions as long as they are still earning income. Fewer limitations allow account holders to enjoy more flexibility in managing their retirement accounts.

A Roth IRA account is not restricted by the employer’s plans as well. Anyone within the income limit can contribute to a Roth IRA up to the maximum annual amount, regardless of the terms of the employer’s plan.

Additionally, if a retiree passes away, the IRA account can be inherited by beneficiaries, and the withdrawals will still be tax-free.

An obvious disadvantage of a Roth IRA is its non-tax-deductible contributions. However, it can be offset by its tax-free distributions, especially when the future marginal tax rate is expected to be higher than the current marginal tax rate.

Another important disadvantage is the income restriction. People with very high MAGI are not eligible for Roth IRA. Also, the contributions that can be made are limited by the account owner’s income. He/She cannot make contributions that are higher than the limit set by the IRS, based on the owner’s MAGI.

However, there is a method that allows those with high incomes to contribute to Roth IRAs, known as “Roth conversion.” To apply, the individual can first open and contribute to a traditional IRA, then pay the taxes that were deducted.

Later, he/she can convert the traditional IRA to a Roth IRA. The conversion cannot be reversed, so the account holder must carefully decide whether to convert or not.