Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The speed at which a business sells its inventory

Inventory turnover, or the inventory turnover ratio, is the number of times a business sells and replaces its stock of goods during a given period. It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time.

A high inventory turnover generally means that goods are sold faster and a low turnover rate indicates weak sales and excess inventories, which may be challenging for a business.

Inventory turnover can be compared to historical turnover ratios, planned ratios, and industry averages to assess competitiveness and intra-industry performance. Inventory turns can vary significantly by industry.

Enter your name and email in the form below and download our free Inventory Turnover Calculator Template now!

For example:

Republican Manufacturing Co. has a cost of goods sold of $5M for the current year. The company’s cost of beginning inventory was $600,000, and the cost of ending inventory was $400,000. Given the inventory balances, the average cost of inventory during the year is calculated at $500,000. As a result, inventory turnover is rated at 10 times a year.

Cost of goods sold is an expense incurred from directly creating a product, including the raw materials and labor costs applied to it. However, in a merchandising business, the cost incurred is usually the actual amount of the finished product (plus shipping cost if any is applicable) paid for by a merchandiser from a manufacturer or supplier.

In both types of businesses, the cost of goods sold is properly determined by using an inventory account or list of raw materials or goods purchased that are maintained by the owner of the company.

Average inventory is the average cost of a set of goods during two or more specified time periods. It takes into account the beginning inventory balance at the start of the fiscal year plus the ending inventory balance of the same year.

These two account balances are then divided in half to obtain the average cost of goods resulting in sales.

Average inventory does not have to be computed on a yearly basis; it may be calculated on a monthly or quarterly basis, depending on the specific analysis required to assess the inventory account.

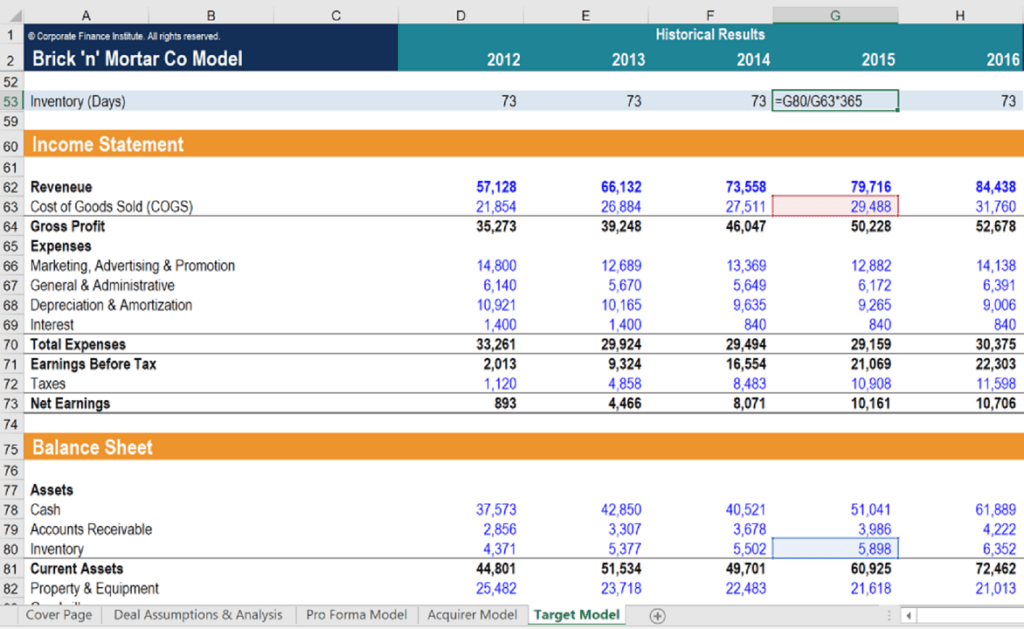

Below is an example of calculating the inventory turnover days in a financial model. As you can see in the screenshot, the 2015 inventory turnover days is 73 days, which is equal to inventory divided by cost of goods sold, times 365. You can calculate the inventory turnover ratio by dividing the inventory days ratio by 365 and flipping the ratio.

In this example, inventory turnover ratio = 1 / (73/365) = 5. This means the company can sell and replace its stock of goods five times a year.

Source: CFI Financial Modeling Courses

One way to assess business performance is to know how fast inventory sells, how effectively it meets the market demand, and how its sales stack up to other products in its class category. Businesses rely on inventory turnover to evaluate product effectiveness, as this is the business’s primary source of revenue.

Higher stock turns are favorable because they imply product marketability and reduced holding costs, such as rent, utilities, insurance, theft, and other costs of maintaining goods in inventory.

Another purpose of examining inventory turnover is to compare a business with other businesses in the same industry. Companies gauge their operational efficiency based on whether their inventory turnover is at par with or surpasses the average benchmark set per industry standards.

Thank you for reading this guide to better evaluate how inventory turns at a company. To keep learning and advancing your career as a financial analyst, these additional CFI resources will help you: