Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Fixed, tangible assets

Property, Plant, and Equipment (PP&E) is a non-current, tangible capital asset shown on the balance sheet of a business and is used to generate revenues and profits. PP&E plays a key part in the financial planning and analysis of a company’s operations and future expenditures, especially with regards to capital expenditures.

The PP&E account is often denoted as net of accumulated depreciation. This means that if a company does not purchase additional new equipment (therefore, its capital expenditures are zero), then Net PP&E should slowly decrease in value every year due to depreciation. This can be better determined with a depreciation schedule.

PP&E is a tangible fixed-asset account item, and the assets are generally very illiquid. A company can sell its equipment, but not as easily or quickly as it can sell its inventory or investments such as bonds or stock shares. The value of PP&E between companies varies substantially according to the nature of their business. For example, a construction company will generally have a significantly higher property, plant, and equipment balance than an accounting firm does.

Property, plant, and equipment basically includes any of a company’s long-term, fixed assets. PP&E assets are tangible, identifiable, and expected to generate an economic return for the company for more than one year or one operating cycle (whichever is longer).

The account can include machinery, equipment, vehicles, buildings, land, office equipment, and furnishings, among other things. Note that, of all these asset classes, land is one of the only assets that does not depreciate over time.

If a company produces machinery (for sale), that machinery is not classified as property, plant, and equipment, but rather is classified as inventory. The same goes for real estate companies that hold buildings and land under their assets. Their office buildings and land are PP&E, but the houses or land they sell are inventory.

Formula:

Net PP&E = Gross PP&E + Capital Expenditures – Accumulated Depreciation

To illustrate:

In May 2017, Factory Corp. owned PP&E machinery with a gross value of $5,000,000. Accumulated depreciation for the same machinery was $2,100,000. Due to the wear and tear of the machinery, the company decided to purchase another $1,000,000 in new equipment. For this period, the depreciation expense for all old and new equipment is $150,000.

Thus, the ending balance is $3,750,000. This is found by taking $5,000,000 + $1,000,000 – $2,100,000 – $150,000.

As the above formula shows, Capital Expenditures (often referred to as CapEx for short) are what is added to the net property, plant, and equipment balance on the balance sheet. When the company spends money investing in either (1) updating existing equipment, or (2) purchasing new additional equipment, this adds to the total PP&E balance on the balance sheet.

PP&E should be recognized by a company only if:

The initial costs of a PP&E item may include:

The nature of PP&E assets is that some of these assets need to be regularly fixed or replaced to prevent equipment failures or to adopt a more sophisticated technology. For example, it is normal for companies to repair or replace old factories or automobiles with new assets when necessary.

The general rule in accounting for repairs and replacements is that repairs and maintenance work are expensed while replacements of assets are capitalized. Repairs are easy to record; it is simply a debit to repair or maintenance expense and a credit to cash. Replacements, however, are a bit more complicated. For replacements, the old cost of the asset is written off from the company’s books, and the cost of the new replacement is recorded/recognized.

The other major component of the PP&E formula is depreciation. Depreciation reduces the value of property, plant, and equipment on the balance sheet as the value of assets is lowered over time due to wear and tear and the reduction of their useful life. The depreciation expense is used to reduce the value of the net balance and it flows to the income statement as an expense.

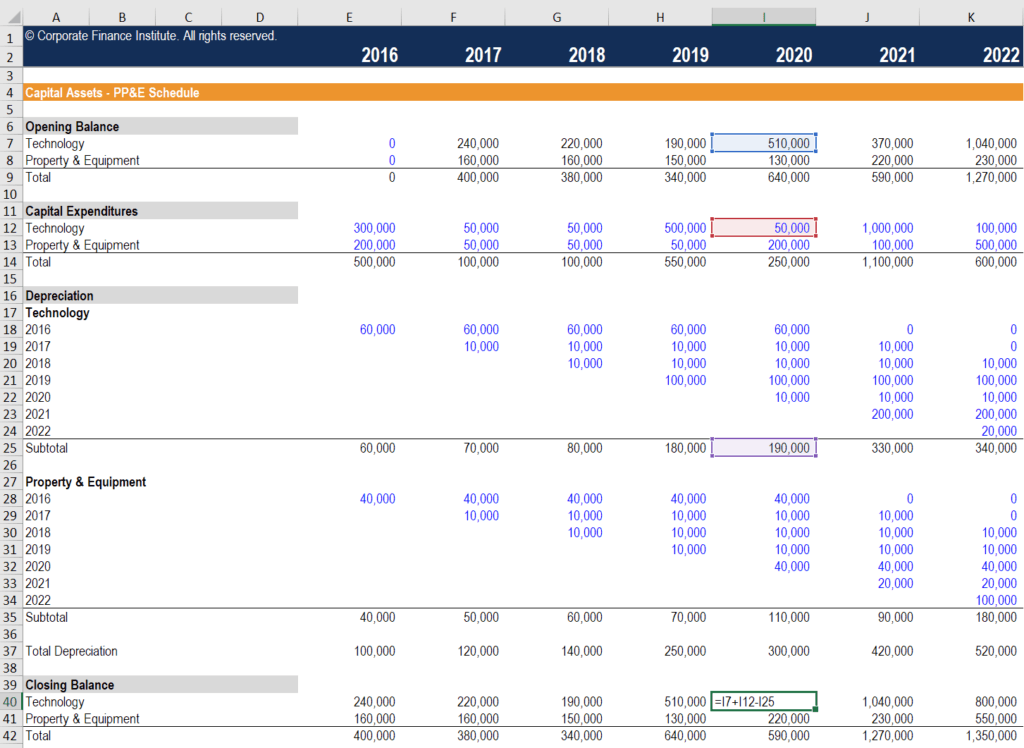

The easiest way to keep track of fixed capital assets is with a schedule, such as the one shown below. This is the type of analysis a financial analyst would prepare and maintain for a company in order to prepare complete financial statements or build a financial model in Excel.

Download the PP&E Schedule Template to use it on your own! Enter all assumptions in the blue font cells.

Click the button below to donwload CFI’s free Property Plant and Equipment Schedule Template

As shown above, the schedule starts with a PP&E opening balance, which is the beginning value of assets. From there, any additional purchases of new assets or improvements to existing ones are added as capital expenditures. Below that, depreciation expense is deducted (note: deprecation can be calculated in many different ways, depending on the type of depreciation method used). Finally, by taking the opening balance, adding CapEx, and deducting depreciation, we arrive at the closing balance.

The closing balance is what goes on the balance sheet at the end of each accounting period. Each subsequent period’s opening balance is equal to the prior period’s closing balance, which is how the schedule rolls forward. An exercise such as this is very common in financial modeling and valuation analysis.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to PP&E (Property, Plant & Equipment). To keep learning and advancing your career, the following CFI resources will be helpful: