Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Payments that are overdue and that is supposed to be made at the end of a given period after missing out on the required payments

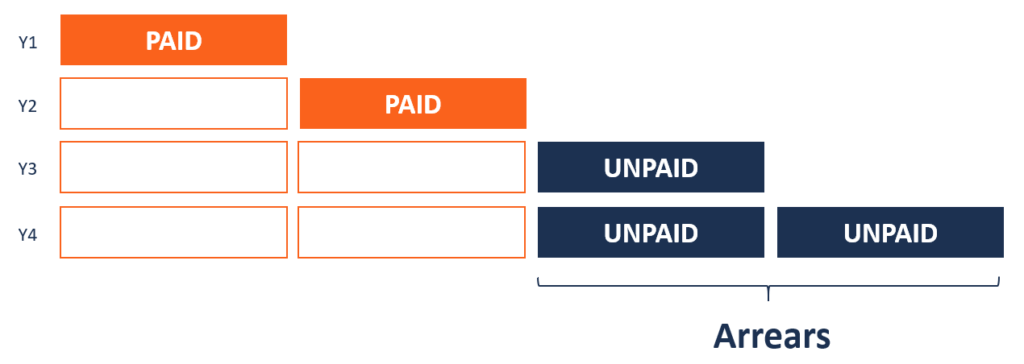

Arrears refers to payments that are overdue and that are supposed to be made at the end of a given period after missing out on the required payments. Total arrears equals the sum of all the payments that have accumulated over time since the first payment was due. The term can be used in relation to various costs such as rent payments, water bills, child support, royalties, dividends, loan repayments, etc.

An account can also be said to be in arrears if the service has already been rendered, and the payment is due to be made at the end of the agreed period. For example, an employee is paid a salary in arrears because the service must be offered and completed before any payments can be made.

Payment in arrears is a payment that is made once a service has been offered. It differs from payments in advance or past due payments. For salaried employees, payments are made once the service has been delivered by the employee to the employer.

The payment may also be referred to as a singular arrear not classified as a late payment. Other examples of payments in arrears include postpaid phone service, postpaid water bills, postpaid electricity bills, property taxes, etc.

Payment in advance is made before the actual service has been provided. An example of a payment in advance is rent, which is paid at the start of the month. If a tenant fails to honor the payment at the start of the month and makes the payment one month later, the payment is said to be one month in arrears.

Other examples of payments that are made in advance include insurance premiums, internet service bills, prepaid phone service, lease, prepaid electricity bills, etc.

Call-in arrears refers to the amount that a defaulter shareholder has not paid on the call money by the due date. It is calculated by deducting the paid-up capital from the called-up capital. The issuer may recover the unpaid call money if the received shares are forfeited. If there is no difference between the called up capital and the paid-up capital, the call-in arrears will be zero.

Arrears also apply in the financial industry when making annuity payments. An annuity is a transaction that occurs in equal intervals and in equal amounts over a defined period of time. For example, an annuity transaction may involve equal payments of $300 over a period of 10 years.

If the annuity payment is made at the end of a fixed period rather than at the start, it is referred to as an annuity in arrears or an ordinary annuity.

The concept of arrears also applies when a publicly-traded company issues dividends to its investors. It occurs when the company delays in paying the cumulative dividends to its preferred stockholders by the agreed date. Preferred stockholders are a type of stockholders that must be paid regardless of whether the company makes profits or not.

The delay in dividend payments to preferred stockholders occurs because the company lacks sufficient cash flow to pay dividends; therefore, the board of directors may not authorize them. Information about the dividends in arrears is recorded in the notes to the financial statements.

When dividends are in arrears, there is usually a legal agreement between the preferred stockholders and the management that prevents the company from paying dividends to ordinary stockholders. Also, the company may be restricted from using cash during the period when the dividends are in arrears.

If the company’s financial situation improves in the future, the board of directors will authorize the payment of all or a portion of the cumulative dividends. Preferred stockholders must be paid first before any payments are made to common stockholders. The paid dividends will be recorded as a short-term liability in the balance sheet.

An arrears swap is a type of interest rate swap that sets and pays the interest rate at the end of the coupon period, rather than in the beginning. On the contrary, a standard swap sets the interest rate at the beginning and pays the interest at the end.

An arrears swap is preferred by speculators who predict the yield curve and receive interest payments at the end of the coupon period. The interest reflects the timeliness of the predictions they made at the start of the coupon period.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: