Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A financial product that provides specific cash flows at equal time intervals

An annuity is a financial product that provides certain cash flows at equal time intervals. Annuities are created by financial institutions, primarily life insurance companies, to provide regular income to a client.

An annuity is a reasonable alternative to some other investments as a source of income since it provides guaranteed income to an individual. However, annuities are less liquid than investments in securities because the initially deposited lump sum cannot be withdrawn without penalties.

Upon the issuance of an annuity, an individual pays a lump sum to the issuer of the annuity (financial institution). Then, the issuer holds the amount for a certain period (called an accumulation period). After the accumulation period, the issuer must make fixed payments to the individual according to predetermined time intervals.

Annuities are primarily bought by individuals who want to receive stable retirement income.

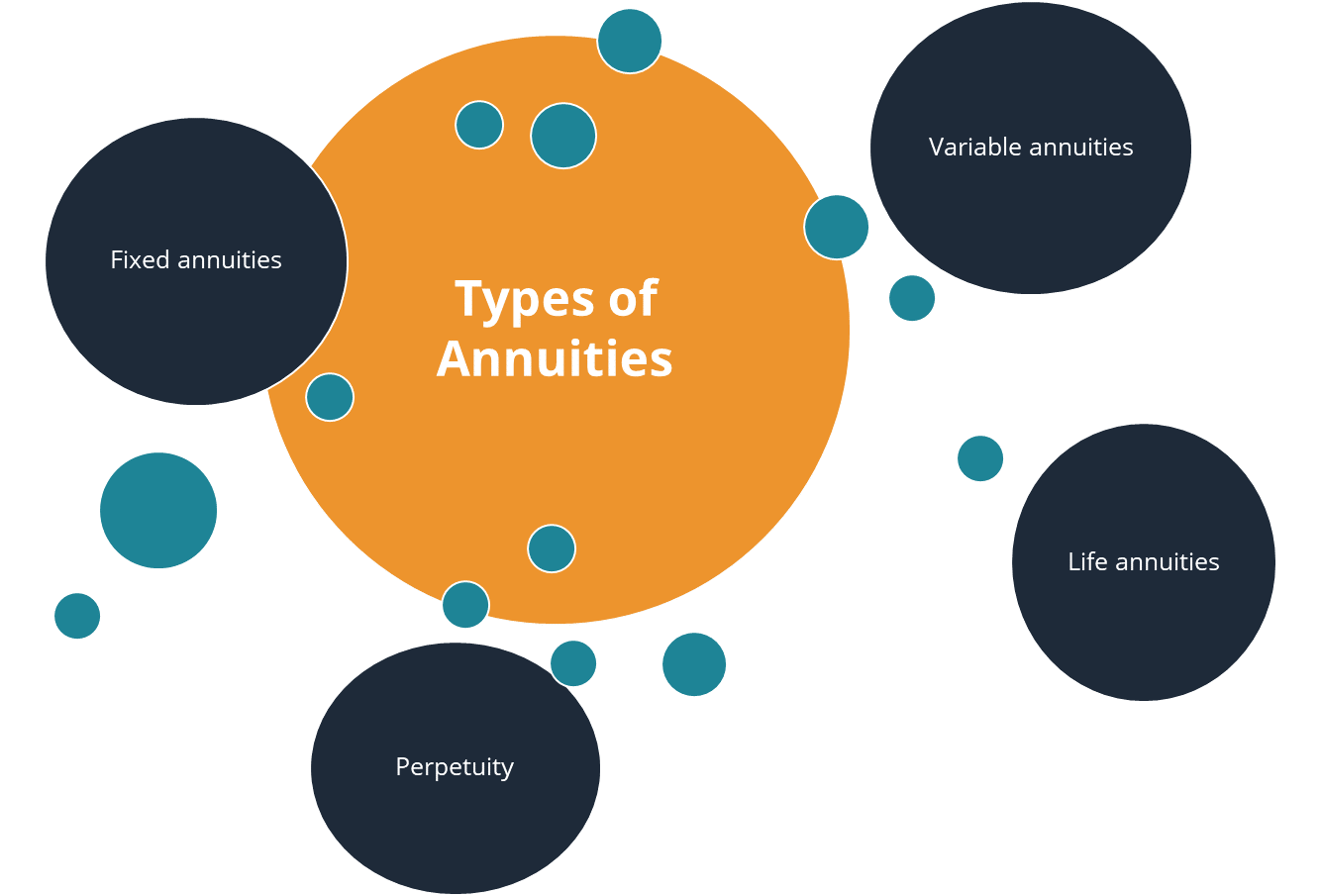

There are several types of annuities that are classified according to frequency and types of payments. For example, the cash flows of annuities can be paid at different time intervals. The payments can be made weekly, biweekly, or monthly. The primary types of annuities are:

Annuities that provide fixed payments. The payments are guaranteed, but the rate of return is usually minimal.

Annuities that allow an individual to choose a selection of investments that will pay an income based on the performance of the selected investments. Variable annuities do not guarantee the amount of income, but the rate of return is generally higher relative to fixed annuities.

Life annuities provide fixed payments to their holders until his/her death.

An annuity that provides perpetual cash flows with no end date. Examples of financial instruments that grant perpetual cash flows to its holder are extremely rare.

The most notable example is a UK Government bond called consol. The first consols were issued in the middle of the 18th century. The bonds did not specify an explicit end date and were redeemable at the option of the Parliament. However, the UK Government redeemed all consols in 2015.

Annuities are valued by discounting the future cash flows of the annuities and finding the present value of the cash flows. The general formula for annuity valuation is:

Where:

The valuation of perpetuity is different because it does not include a specified end date. Therefore, the value of the perpetuity is found using the following formula:

Thank you for reading CFI’s guide on Annuity. To learn more about related topics, check out the following CFI resources: