Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Restatement of a company's profit that removes the effect of one-time charges, write-downs, cost-cutting, and other extraordinary items

Headline earnings are a restatement of a company’s profit that removes the effect of one-time charges, write-downs, cost-cutting, and other extraordinary items like tax liabilities. Another way of looking at headline earnings is that it is the part of a company’s earnings that pertains to its core business activities.

It is a less volatile measure of earnings compared to, say, net profit, which is a bottom-line figure that includes the impact of all items on an income statement. It is a more accurate representation of the business performance as it closely tracks business operations.

Headline earnings are a non-standard measure and are not recognized under GAAP and IFRS. The main purpose of headline earnings is in the field of financial statement analysis. The next sections discuss the importance of headline earnings as a measure and a simple example illustrating its calculation.

As stated in the previous section, headline earnings are primarily used for financial statement analysis. It is an important part of an analyst’s toolkit and helps them produce accurate analyses of individual companies, whether it is a recommendation or valuation.

One thing that headline earnings as a measure achieves is an accurate representation of the business performance. Given the complexity of accounting procedures, it is common for management to misrepresent the financial performance of the company using things such as extraordinary items. A common example is the use of non-recurring earnings to overstate a company’s earnings. If it is not adjusted for, it flows through to essential metrics like the P/E ratio widely used by investors.

In cases like above, headline earnings can be very effective as it removes the noise added by unusual items and isolates business performance. The headline earnings figure can be further used to arrive at alternative metrics like headline earnings per share and improve the information content of the P/E ratio. The accuracy of multiples is indispensable to certain analyses like valuation. Popular valuation methodologies, such as the discounted cash flow model and relative value models, use multiples as inputs while calculating the final price. Poor inputs at that stage derail even the most rigorous models.

Another property of headline earnings is low volatility. It makes them more amenable to forecasting and time series analysis. It is easier to create robust forecasts for a stable series without jumps. Again, good forecasts are an essential part of all financial analyses.

The stricter definition of headline earnings also excludes any impact of cost-cutting strategies in addition to unusual items. It focuses on business performance alone. A company can temporarily improve its performance by reducing costs, but such an approach is unsustainable if the business model is fundamentally unsound. Hence, headline earnings can be used as an investment tool to zero in on companies with high-quality business models, stable earnings, and sustainable earnings growth.

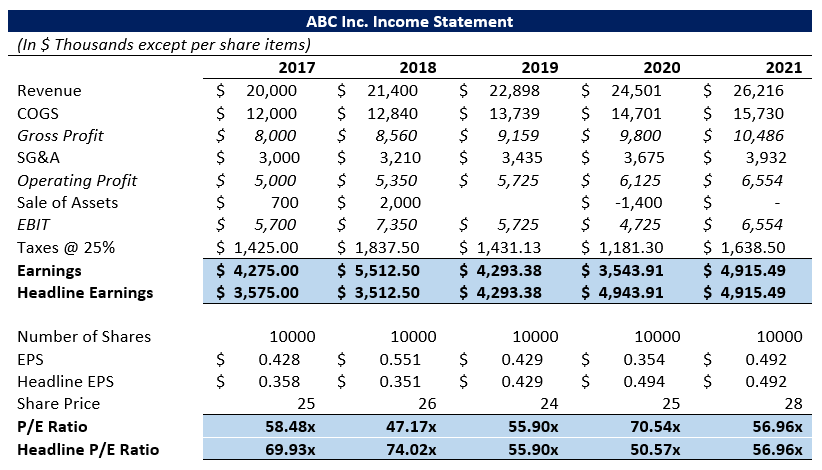

Headline earnings can be computed in two ways; one excludes the impact of unusual items only. The second method also excludes the impact of any cost-cutting strategies. The following example shows the effect of using headline earnings compared to net earnings on the P/E ratio.

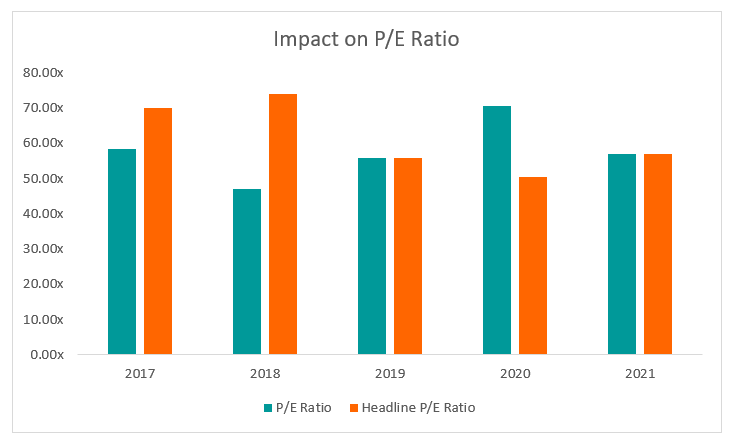

As is evident from the chart, the results can be very different depending on the choice of earnings metric. In such a case, the difference can be as much as 20x. The jumps in the P/E ratio can also lead to price jumps in the stock price as naïve investors rush to buy or sell the stock based on faulty information.

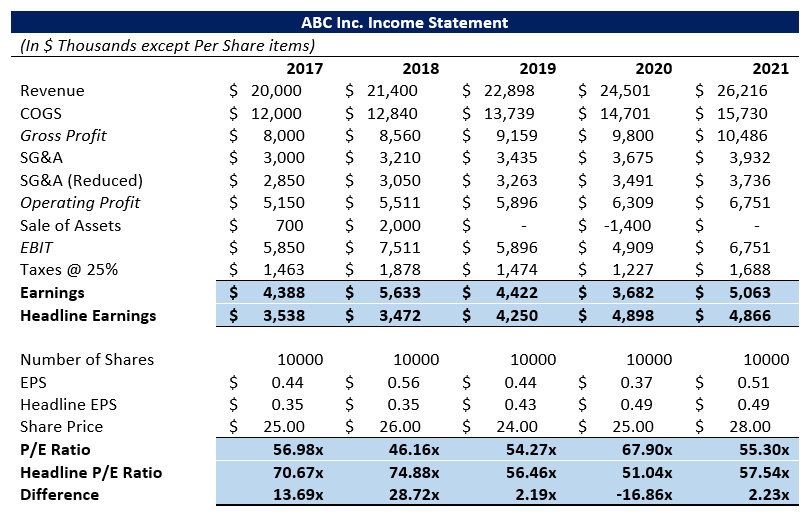

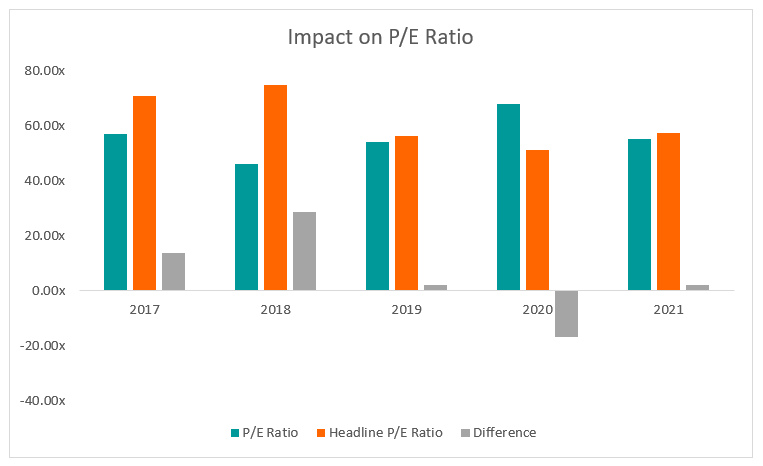

The next example looks at the stricter definition that excludes the effects of cost-cutting strategies in addition to extraordinary items. In such a case, the headline earnings are important as it helps the analyst study the sustainability of the business. In the above example, assume that the company cuts its Selling, General & Administration (SG&A) costs by 5% every year. The chart below shows the difference between using net earnings and headline earnings.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: