Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A financial statement that covers a period of less than a year

An interim statement refers to a financial statement that covers a period of less than a year. Interim financial statements portray the financial performance of a company over a short period of time.

Publicly traded companies are required to release interim statements on a quarterly basis, providing investors with updates on how the company is performing and also to keep its financial activities transparent. It’s also important to note that the term “interim” can be applied to any period of time that’s less than a year and does not necessarily refer to quarterly results.

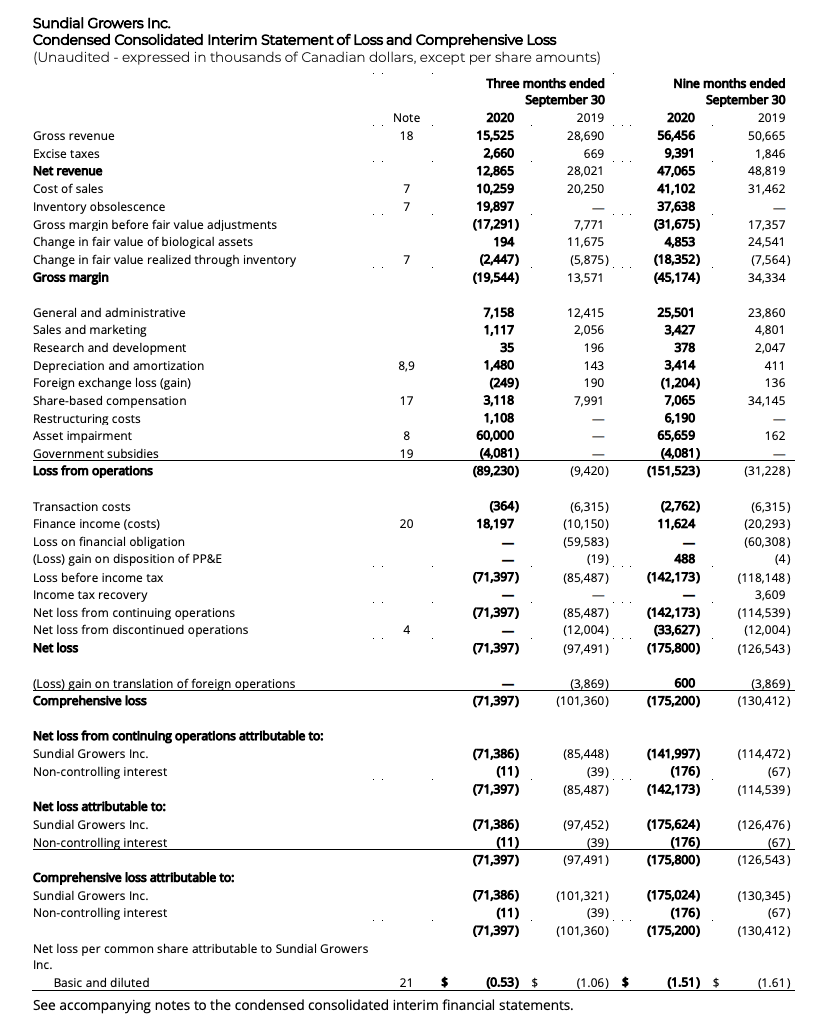

Here’s an income statement from an interim financial report released by Sundial Growers Inc., a Canadian cannabis company.

In the example above, Sundial Growers reports losses over the three-month and nine-month period ended September 30, 2020. The statement is unaudited since interim statements are not required to be audited, unlike annual financial statements. However, they still contain the same elements – a balance sheet, an income statement, and a statement of cash flows.

Interim statements allow investors to receive timely updates on a company’s operations and financial performance, which, in turn, influences investor’s capital decisions. For example, if a company exceeds expectations by reporting much higher sales in a particular quarter, investors are likely to be impressed and therefore invest more money in the company’s shares, and vice versa.

By providing a more frequent look at a company’s performance than annual statements, interim statements ensure that investors have the information required to make decisions on their allocation of capital. As a result, they ensure that the capital market remains liquid throughout the year.

Annual financial statements require certain disclosures that can be omitted or referenced for interim statements. In other words, the regulations for reporting in annual statements are much more stringent than those for interim statements.

If an expense is accrued within a particular interim reporting period, it will be reflected on the financial statements. For example, if Company X reports financial results from May-September, expenses accrued during that period will appear on the interim report. Therefore, if a company accrues an overwhelming majority of expenses within a short period of time, it can skew its interim statements towards the negative.

If a business goes through a period of higher-than-average sales due to seasonality (i.e., surfboards during the summer or toys during the Christmas season), it will be reflected in its interim statement that covers that particular period. However, it may not be reflected in its annual statement that covers the entire year.

Annual statements must be audited externally, which can be a costly process. The process is not necessary for interim statements. However, for many public companies, a review engagement is conducted instead, and audit procedures are performed at each interim period for annual audit purposes.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: