Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A type of financial ratio used to determine a company's ability to pay its short-term debt obligations

A liquidity ratio is a type of financial ratio used to determine a company’s ability to pay its short-term debt obligations. The metric helps determine if a company can use its current, or liquid, assets to cover its current liabilities. Liquidity ratios focus on short-term financial health, whether a company can meet upcoming bills with cash and near‑cash assets before considering long-term leverage or profitability.

Three liquidity ratios are commonly used the current ratio, quick ratio, and cash ratio. In each of the liquidity ratios, the current liabilities amount is placed in the denominator of the equation, and the liquid assets amount is placed in the numerator.

Given the structure of the ratio, with assets on top and liabilities on the bottom, ratios above 1.0 are sought after. A ratio of 1 means that a company can exactly pay off all its current liabilities with its current assets. A ratio of less than 1 (e.g., 0.75) would imply that a company is not able to satisfy its current liabilities.

A ratio greater than 1 (e.g., 2.0) would imply that a company is able to satisfy its current bills. In fact, a ratio of 2.0 means a company can cover its current liabilities twice over. A ratio of 3.0 would mean they could cover their current liabilities three times over, and so forth.

While liquidity ratios measure a company’s ability to meet short-term obligations, understanding cash vs liquidity provides deeper insight into how those obligations are actually funded.

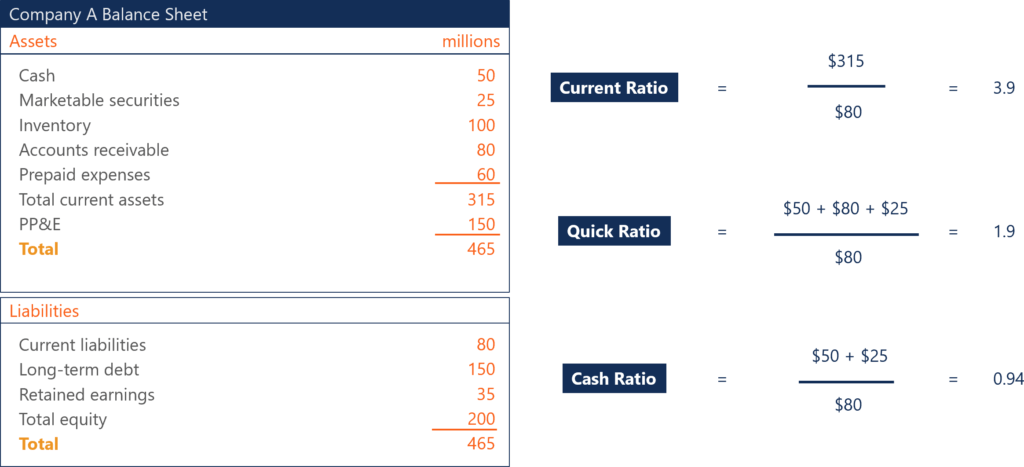

Current Ratio = Current Assets / Current Liabilities

The current ratio is the simplest liquidity ratio to calculate and interpret. Anyone can easily find the current assets and current liabilities line items on a company’s balance sheet. Divide current assets by current liabilities, and you will arrive at the current ratio.

A company has 500 in current assets and 250 in current liabilities. Its current ratio is 500 ÷ 250 = 2.0. This means the business has 2 dollars of current assets for every 1 dollar of short‑term obligations.

Quick Ratio = (Cash + Accounts Receivables + Marketable Securities) / Current Liabilities

The quick ratio is a stricter test of liquidity than the current ratio. Both are similar in the sense that current assets is the numerator, and current liabilities is the denominator.

However, the quick ratio only considers certain current assets. It considers more liquid assets such as cash, accounts receivables, and marketable securities. It leaves out current assets such as inventory and prepaid expenses because the two are less liquid. So, the quick ratio is more of a true test of a company’s ability to cover its short-term obligations.

Suppose current assets total 500, including 100 of inventory and 20 of prepaid expenses, and current liabilities are 250. Cash, accounts receivable, and marketable securities sum to 380. The quick ratio is 380 ÷ 250 = 1.52, showing the company can cover its short‑term liabilities with liquid assets even without selling inventory.

Cash Ratio = (Cash + Marketable Securities) / Current Liabilities

The cash ratio takes the test of liquidity even further. This ratio only considers a company’s most liquid assets – cash and marketable securities. They are the assets that are most readily available to a company to pay short-term obligations.

In terms of how strict the tests of liquidity are, you can view the current ratio, quick ratio, and cash ratio as easy, medium, and hard.

If a company holds 150 in cash and marketable securities and has 250 in current liabilities, the cash ratio is 150 ÷ 250 = 0.6. This means it could immediately cover 60% of its short‑term obligations using only cash and cash‑equivalents, before collecting receivables or selling inventory.

Since the three ratios vary by what is used in the numerator of the equation, an acceptable ratio will differ between the three. It is logical because the cash ratio uses only cash and marketable securities in the numerator, whereas the current ratio uses all current assets.

Therefore, an acceptable current ratio will be higher than an acceptable quick ratio. Both will exceed an acceptable cash ratio. For example, a company may have a current ratio of 3.9, a quick ratio of 1.9, and a cash ratio of 0.94. All three may be considered healthy by analysts and investors, depending on the company.

Liquidity ratios can help in the following:

Liquidity ratios are important to investors and creditors to determine if a company can cover its short-term obligations, and to what degree. A ratio of 1 is better than a ratio of less than 1, but it isn’t ideal.

Creditors and investors like to see higher liquidity ratios, such as 2 or 3. The higher the ratio is, the more likely a company is able to pay its short-term bills. A ratio of less than 1 means the company faces a negative working capital and may be experiencing a liquidity crisis.

Creditors analyze liquidity ratios when deciding whether or not they should extend credit to a company. They want to be sure that the company they lend to has the ability to pay them back. Any hint of financial instability may disqualify a company from obtaining loans.

For investors, they will analyze a company using liquidity ratios to ensure that a company is financially healthy and worthy of their investment. Working capital issues will put restraints on the rest of the business as well. A company needs to be able to pay its short-term bills with some leeway.

Low liquidity ratios raise a red flag, but “the higher, the better” is only true to a certain extent. At some point, investors will question why a company’s liquidity ratios are so high. Yes, a company with a liquidity ratio of 8.5 can confidently pay its short-term bills, but investors may deem such a ratio excessive. An abnormally high ratio means the company holds a large amount of liquid assets.

For example, if a company’s cash ratio was 8.5, investors and analysts may consider that too high. The company holds too much cash on hand, which isn’t earning anything more than the interest the bank offers to hold its cash. It can be argued that the company should allocate the cash amount towards other initiatives and investments that can achieve a higher return.

With liquidity ratios, there is a balance between a company being able to safely cover its bills and improper capital allocation. Capital should be allocated in the best way to increase the value of the firm for shareholders.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

This has been CFI’s guide to Liquidity Ratio. To keep advancing your career, the additional CFI resources below will be useful: