Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A common industry practice for auditors to gather audit evidence from external stakeholders

Negative confirmation is a common industry practice for auditors to gather audit evidence from external stakeholders. A negative confirmation is a letter addressed to a debtor, requesting a response if the debtor disagrees with the stated account balance.

Confirmation occurs if the third party doesn’t respond, or when a correction is submitted by the third party. The process is used in testing managerial assertions about account balances.

Auditors apply professional judgment in deciding which confirmation method is most appropriate in reference to the audit’s risk for material misstatement. An auditor must employ analytical, systematic, and objective judgment when deciding on which confirmation procedure to apply. Below are two primary judgments an auditor must make when deciding to accept an external confirmation from a third party:

The confirmation’s value is completely reliant on the independence of the external party. For example, consider when an auditor sends a confirmation of a fraudulent account receivable to the person who committed the fraud. In such a scenario, the value of the confirmation is nil, as the fraudster would act in their self-interest and conceal their behavior.

Confirmation of the account balance with a third party is important because it explains the managerial assertions behind the stated balance. It is important to assess managerial accounting assertions relative to generally accepted accounting principles (GAAP), as well as to apply testing procedures that comply with generally accepted auditing standards (GAAS).

If the auditor is not satisfied with the third party”s quality of confirmation, they should practice further professional skepticism, and implement further audit procedures.

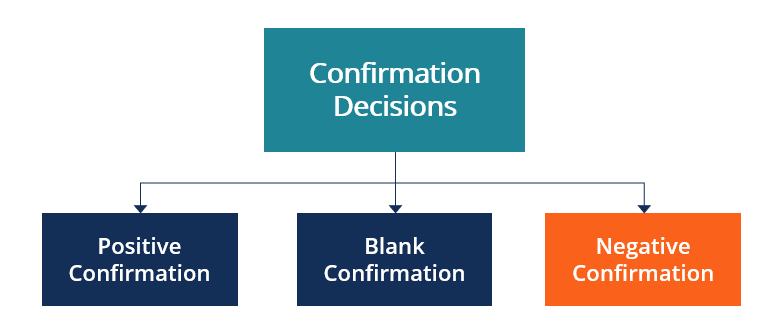

A letter sent to the debtor requesting direct confirmation of the account balance’s accuracy. If inaccurate, the debtor must produce a reason for the discrepancy and update the account balance. If accurate, the debtor must simply confirm the account balance through a response.

Blank confirmation forms are a type of positive confirmation requiring the debtor to return a letter detailing the account balance. The number is then used to cross-reference against the listed receivable balance to ensure accuracy.

A letter sent to the debtor that denotes a specific account and value associated with its balance. The third party can choose to reject the balance and supply their number for the suggested account, or they can choose not to respond to the letter. A suggestion of a differing balance or nonresponse is considered confirmation.

Negative confirmation is best applied in cases where the risk of material misstatement is low. The primary drivers of the risk of material misstatement are inherent risk and control risk. If acceptable audit risk is held equal, a decreased risk of material misstatement increases the detection risk of an auditor failing to identify material misstatements.

Logically, the auditor is willing to accept a higher risk of failing to identify material misstatements due to a less perceived risk of the business’ operating environment and internal processes.

Generally, negative confirmations are most effective when the following are true:

Negative confirmations are advantageous in terms of cost and efficiency. It is measurably less expensive to distribute negative confirmations instead of positive confirmations, and therefore, more can be distributed for the same total cost.

Depending on the auditor’s detection risk, the auditor may need confirmation from hundreds of customers, and it can be more efficient to use negative confirmations to collect audit evidence in such a manner.

If an auditor significantly tests internal controls, negative confirmations are utilized to provide audit evidence of the account balance. Generally, negative confirmations are most often used in audits, where the primary consumer is the general public.

For example, municipalities, retail stores, and banks are all typical audit clients where negative confirmations are utilized in the evidence-gathering process.

The primary factors affecting the confirmation decision are:

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: