Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A market order that requires immediate execution

A held order refers to a market order that should be executed promptly with no hesitation. When a trader receives instructions by way of a held order, implementation time is instant, as the order needs to be filled immediately. In financial markets jargon, it is called “hit the bid or take the offer line.” Like all market orders, held orders are instructions to buy and sell securities such as stocks, bonds, or other hybrid marketable instruments in financial markets.

A derivative of the held order is the held limit order, where the held order comes with a limit on either the buying or selling price. A variant of the held order is the not-held order (the opposite of a held order), which gives traders both time and price discretion in filling the order.

Held orders are typically issued by investors who wish to swiftly change their exposure to certain stocks by liquidating or switching to other stocks or a different instrument altogether. Hence, with the immediate execution feature, a held order is the best market order a trader can use to guarantee an instantaneous transaction.

A trader who receives a held order must act on it immediately. It does not give ample discretion to prowl the market to find a better deal as in other exchange orders, particularly the not-held order. The major constraint of a held order is time, since the order needs to be immediately filled. Let us look at an example of two held orders – a sell held order and a buy held order.

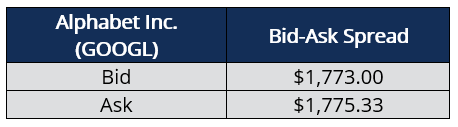

The sell held order instruction is to sell Alphabet Class A shares with a bid-ask price as below:

A trader must satisfy the order by matching the highest bid price; in this case, the price is $1,773. Through such action, a transaction is executed immediately under normal market conditions.

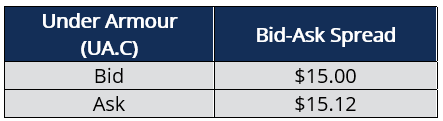

The buy held order instruction is to buy Under Armour (UA.C) Class C shares with a bid-ask price as below:

A buy held order instructs the trader to satisfy the order through matching the lowest offer (ask price); in this case, $15.12. A purchase transaction is executed immediately under normal market conditions.

There are two circumstances where issuing a held order is ideal – i.e., trading a breakout and closing an error position.

Held orders are particularly useful if a trader wants to immediately enter the market on a breakout. A breakout is defined as an increase in a security’s price above a resistance level (previous high) or a drop below a level of support (previous low). In addition, the trader should not be concerned about slippage costs.

Slippage occurs when, after receiving a market order, a market maker changes the bid-ask spread to their benefit. Hence, with a high turnover stock, a trader can choose to incur slippage costs in order to fill the order. It, therefore, depends if the trader is prepared to incur slippage to fill the order promptly.

Such a scenario occurs when a trader makes an error in purchasing a security (for whatever reason). A held order, in this case, is placed to reverse the error position immediately in order to limit any foreseen or unforeseen downside risk. Because of its instantaneous execution attribute, a held order is perfect for unwinding an error position and immediately executing the correct trade.

Illiquid securities normally generate wide bid-ask spreads. Hence, a held order placed on an illiquid stock will force the trader to incur a huge spread in settling the order. Below is an example of a liquid and illiquid stock and the resultant spread incurred by a trader with a held order.

A trader executing a held order on an illiquid stock will incur a 37.5% spread compared to one executing a liquid stock at a 2.9% spread. The trader is better off sitting on top of a bid and enticing the seller through a gradual order price increase.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: