Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

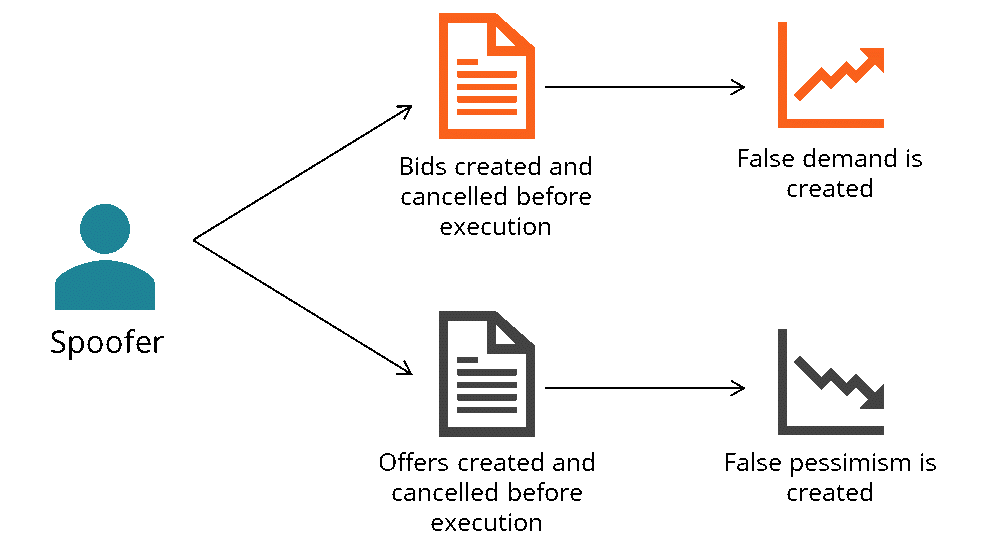

Placing bids to buy or offers to sell futures contracts and canceling the bids or offers prior to the deal’s execution

Spoofing is a disruptive algorithmic trading practice that involves placing bids to buy or offers to sell futures contracts and canceling the bids or offers prior to the deal’s execution. The practice intends to create a false picture of demand or false pessimism in the market.

By creating a false sentiment in the market, a trader can manipulate the actions of other market participants and change the price of a security. Subsequently, by reacting to the fluctuations, a spoofer can earn a profit. Therefore, spoofing is considered a form of market manipulation.

Spoofing became prominent with the rise of high-frequency trading (HFT). High-frequency trading allows the execution of large trade orders in a very short time. Given the advantages of HFT, spoofing gains an immense scope that provides opportunities for moving the prices of the securities to a larger extent and earning higher profits.

Since spoofing is considered a form of market manipulation, the practice is considered illegal. In the United States, it is considered an illegal activity and a criminal offense under the 2010 Dodd-Frank Act. The U.S. Commodity Futures Trading Commission (CFTC) is an independent agency that monitors such activities in futures markets.

Despite the accompanying criminal liability, some large financial institutions continue to engage in the illegal practice. For example, in January 2018, three European banks – UBS, Deutsche Bank, and HSBC – were accused of market manipulation using spoofing schemes and were fined by the Commodity Futures Trading Commission (CFTC).

The 2010 Flash Crash erased almost $1 trillion in market value in U.S. stock markets. The market crash was characterized by a rapid decline in the stock markets and their quick partial rebound within an hour.

Following a series of investigations, market manipulation using spoofing schemes was determined as one of the primary triggers of the Flash Crash. In 2015, the U.S. Department of Justice filed charges against a London-based trader, Navinder Singh Sarao. He was accused of market manipulation after placing a large order for E-Mini S&P 500 stock index futures contracts with the intent to cancel the order prior to execution.

Thank you for reading CFI’s explanation of spoofing. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: