Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The Stock Market Crash of March 6, 2010

The 2010 Flash Crash is the market crash that occurred on May 6, 2010. During the 2010 crash, leading US stock indices, including the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite Index, tumbled and partially rebounded in less than an hour. The day was distinguished by high volatility in trading of all types of securities, including stocks, futures, options, and ETFs.

Although the market indices managed to partially rebound in the same day, the flash crash erased almost $1 trillion in market value.

Beginning in the morning, trading on major US markets on May 6, 2010 showed a negative trend. It was mainly due to concerns regarding the financial situation in Greece and the upcoming elections in the UK. By afternoon, the major indices of equities and futures were down by 4% from their previous day’s close.

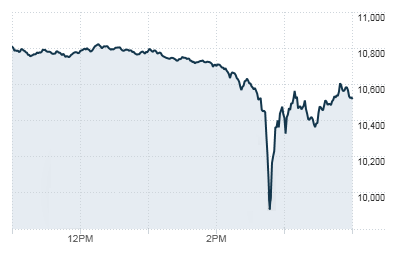

By 2:30 p.m., trading was becoming extremely turbulent. The Dow Jones Industrial Average (DJIA) lost almost 1,000 points in around 10 minutes. However, in the next 30 minutes, the index recovered almost 600 points.

Other market indices across North America were also affected by the Flash Crash. The S&P 500 Volatility Index increased by 22.5% on the same day, while the S&P/TSX Composite Index in Canada lost more than 5% of its value in between 2:30 p.m. to 3:00 p.m.

By the end of the trading day, the major indices regained more than half of the lost values. Nevertheless, the Flash Crash took away around $1 trillion in the market value.

After the Flash Crash, the US Securities and Exchange Commission (SEC) conducted an investigation of the possible causes of the unexpected market event. In September 2010, the SEC published a report containing the findings of its investigation.

According to the report, before the flash crash, the markets were particularly fragile and were exposed to extreme turbulence. A single selling order of an enormously large amount of E-Mini S&P contracts and subsequent aggressive selling orders executed by high-frequency algorithms triggered the massive decline in market prices, which was already accruing exponentially due to prevailing negative market trends at that time.

The immense volatility compelled many high-frequency traders to halt their trading. The trading of E-Mini S&P contracts was paused to prevent it from further declines. When the trading of the contracts resumed, their prices started to stabilize. The markets started to regain their positions as the prices of many securities returned to near their initial levels.

The DJIA on May 6, 2010 (11:00 AM – 4:00 PM EST)

The results of different investigations of the 2010 Flash Crash led to conclusions that the high-frequency traders played a significant role in the crash. The aggressive selling and buying of large volumes of securities resulted in enormous price volatility in the financial markets. At minimum, the activities of high-frequency traders exacerbated the effects of the crash.

In 2015, London-based trader Navinder Singh Sarao was arrested following allegations of market manipulation that resulted in the Flash Crash. According to the charges, Sarao’s trading algorithm executed a number of large selling orders of E-Mini S&P contracts to push the prices down, which ultimately triggered the market crash.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s explanation of the Flash Crash. CFI offers the Capital Markets & Securities Analyst (CMSA®) certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following resources: