Get In-Demand Finance Certifications

In banking, it’s vital that measures are in place to ensure that banks have enough funds to honor their financial obligations regardless of any risks, financial struggles, or investments that arise. That’s where bank regulatory ratios and capital requirements come into play.

Bank regulatory ratios are key measures of the strength and resilience of banks used by investors, creditors, regulators, customers, and other stakeholders. Essentially, bank regulatory ratios help measure the solvency and efficiency of banks.

There are various regulatory capital ratios that measure different aspects of a bank’s solvency. While calculating these different bank regulatory capital ratios can be complex, doing so helps establish an entire framework that keeps the banks running.

The purpose of the banking regulatory framework is to create a secure financial system that enables banks to continue serving their clientele in any economic condition. If banking regulatory capital ratios are calculated and used correctly, they’ll set up a structure that will ensure banks always have enough funds to service their obligations.

Essentially, banking ratios make banks self-insure against losses. This is because as long as banks maintain a sufficient financial “buffer,” they can still meet obligations as they arise, helping keep the financial system solvent and stable.

Risk-weighted assets are a bank’s loans and other assets weighted according to risks to determine the minimum amount of capital that banks need at any given time. The risk-weighted assets calculation is commonly used to determine the adequacy of a bank’s capital.

Regulators require that banks group assets together into classes by risk category so that the amount of required capital matches the risk level of each asset type. For example, debentures carry a higher risk than low-risk government bonds and are thus in a different class of risk weight.

Because a large percentage of bank assets are loans, regulators consider both the source of loan repayment and the underlying value of the collateral when assessing their risk. Riskier assets, such as unsecured loans, are assigned a higher risk weight than assets such as cash and Treasury bills. The higher the amount of risk an asset possesses, the higher the regulatory capital requirements.

To calculate risk-weighted assets, banks multiply the exposure amount by the relevant risk weight for the type of loan or asset. Banks repeat this calculation for all their loans or assets and then add them to calculate total credit risk-weighted assets. Risk exposure is the maximum amount of potential loss. The Basel Committee on Banking Supervision (BCBS) is the global banking regulator that sets the rules for risk weighting.

The Basel Accords are a series of banking regulatory agreements set by the Basel Committee on Bank Supervision (BCBS). These three banking regulatory agreements are Basel I, Basel II, and Basel III. The Accords ensure that financial institutions have enough capital to absorb unexpected losses.

The first Basel Accord, Basel I, was issued in 1998 and focused on the capital adequacy of financial institutions. Under Basel I, banks that operate internationally must maintain capital equal to at least 8% of their risk-weighted assets. For example, if a bank has risk-weighted assets equal to $100 million, it must have a minimum capital of at least $8 million. A bank’s regulatory capital under Basel I has two tiers.

Basel II, also known as the Revised Capital Framework, was an updated version of the original Basel Accord. The Basel II framework focused on three main areas, otherwise known as three pillars: capital adequacy requirements, supervisory review, and market discipline.

Basel II also divided a bank’s regulatory capital from two to three tiers. The third tier, defined as tertiary capital, is derived from trading activities. While tier 3 capital included a greater variety of debt than tier 1 and tier 2, it was of much lower quality and thus later rescinded.

The third and most recent set of updates to the Basel Accord was agreed upon in 2010. Basel III focused on the same three main pillars that it did before, just with additional requirements and safeguards. An example of a Basel III additional requirement is that banks now have to have a minimum amount of common equity and a minimum liquidity ratio.

Basel III also added requirements for global systemically important banks that are considered “too big to fail.” While Basel III added additional safeguards and requirements to the Accords, it rescinded regulatory capital tier 3 at this time.

The final Basel III framework includes phase-in provisions that started at 50% in January 2023 and have been rising in annual steps of 5% ever since. These provisions are expected to be fully phased in at the 72.5% level in January 2028. The onward measures to the Basel Accord have been referred to as Basel 3.1 or IV.

Capital requirements are standardized regulations that determine how much liquid capital banks must hold given a certain level of assets. The purpose of capital requirements is to ensure that banks have enough liquid funds to uphold their financial obligations to customers and stakeholders despite experiencing operating losses.

Capital requirements were also set to ensure that bank and depository institution holdings aren’t dominated by investments that increase the risk of default. According to the government Federal Reserve Board site, “Under the Federal Reserve Board’s capital framework for bank holding companies, covered savings and loan holding companies, and U.S. intermediate holding companies with $100 billion or more in total consolidated assets, capital requirements are in part determined by the supervisory stress test results.”

The biggest catalyst for the creation or alteration of banking capital requirements is financial crises. Capital requirements are created or altered when financial crises occur to ensure that banks will always be able to meet their financial obligations to stakeholders, investors, and customers.

In addition, when banks experience financial issues during economic recessions or crises, capital requirements are often altered to resolve those issues and prevent those issues from occurring again in the future. The key financial crises that led to capital requirements being created or altered are listed below.

According to the Basel Accords, types of regulatory bank capital in capital requirements are divided into tiers. These bank capital tiers are based on subordination and the bank’s ability to absorb losses.

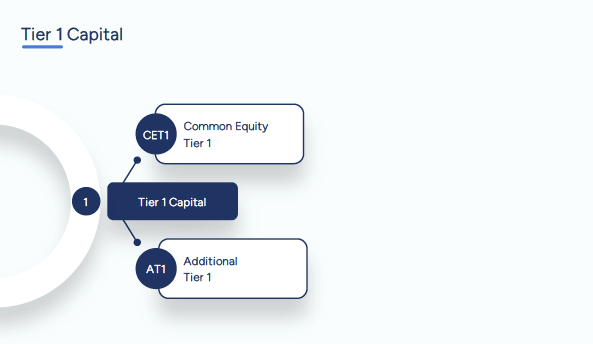

Tier 1 Capital is the primary funding source of the bank, holding nearly all the bank’s accumulated funds. These funds support banks by absorbing losses so that regular business functions can continue running.

Common Equity Tier 1 (CET1) is a component of tier 1 capital that comprises a bank’s core capital and includes common shares, stock surpluses resulting from the issuance of common shares, retained earnings, common shares issued by subsidiaries and held by third parties, and accumulated other comprehensive income (AOCI).

Tier 1 Capital includes CET1 plus Additional Tier 1 Capital. Thus, like CET1 Capital, Additional Tier 1 Capital is a component of Tier 1 Capital. Additional Tier 1 Capital consists of contingent convertible bonds, perpetual non-cumulative preferred shares, and perpetual subordinated debt.

Under Basel III, the Tier 1 capital requirement is 6%. The 6% includes 4.5% of Common Equity Tier 1 and an extra 1.5% of Additional Tier 1 Capital.

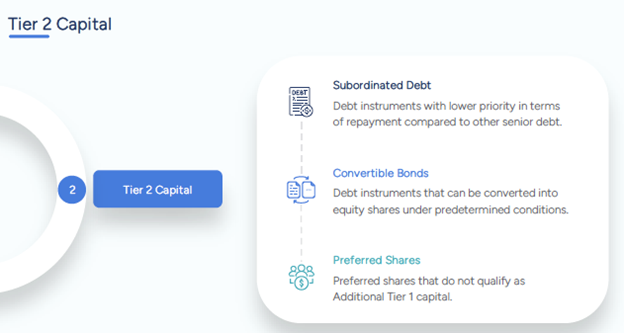

Tier 2 Capital is supplementary bank capital because it’s less reliable than Tier 1 Capital. Tier 2 Capital includes undisclosed funds that don’t appear on a bank’s financial statements, revaluation reserves, hybrid capital instruments, subordinated term debt, also known as junior debt securities, and general loan loss or uncollected reserves. Under Basel III, the minimum Tier 2 capital requirement is 8%.

Banking ratios for financial strength measure the bank’s ability to have the necessary cash or funds to uphold its financial obligations. In other words, banking ratios for financial strength measure the solvency of a bank. Common banking ratios for financial strength include the capital adequacy ratio, liquidity coverage ratio, supplementary leverage ratio, and the common equity tier 1 (CET1) capital ratio.

The capital adequacy ratio (CAR) is the ratio of a bank’s capital to its risk. Banks use the capital adequacy ratio to prevent themselves from taking excess leverage and becoming insolvent in the process. To calculate the capital adequacy ratio, you must divide the eligible capital by the risk-weighted assets. Essentially, the more risks a bank takes, the more capital it needs to protect its depositors.

As its name suggests, the liquidity coverage ratio measures the liquidity of a bank. Liquidity refers to the ability to have money, such as cash, that is easily accessible. More specifically, the liquidity coverage ratio measures the ability of a bank to meet 30 days’ worth of its financial obligations without having to access outside cash. To calculate the liquidity coverage ratio, you must divide the high-quality liquid asset amount by the total net cash outflow amount.

Any bank that can fund cash outflows for 30 days should be financially stable enough not to collapse during a financial crisis. This is because 30 days is approximately the amount of time it takes for the government to step in to help a bank during a financial crisis.

The supplementary leverage ratio measures the ability of a bank to cover its leverage exposure with tier 1 capital. Tier 1 capital is the primary funding source of the bank, as it typically holds all of the bank’s accumulated funds. Because tier 1 capital is the first capital source to absorb losses in a financial downturn, it helps the bank maintain solvency. To calculate the supplementary leverage ratio, divide the tier 1 capital by the bank’s total leverage exposure.

There are various bank regulatory ratios that are commonly used. You can divide these banking regulatory ratios into the following categories: profitability, efficiency, and financial strength.

Banking ratios for profitability are bank-specific ratios that measure forms of income. Common banking ratios for profitability include the net interest margin ratio and the return-on-assets (ROA) ratio.

The net interest margin ratio measures the difference between interest income and interest expense.

Most of a bank’s revenue comes from collecting interest on loans. Additionally, banks fund most of their operations through customer deposits and debt and will incur a large amount of interest expense.

Therefore, the net interest margin is calculated as the difference between interest income and interest expense and then dividing that result by the bank’s total assets.

A return-on-assets (ROA) ratio is a company’s net, after-tax income divided by its total assets. The ROA ratio is often applied to banks because cash flow analysis is more difficult to construct accurately. Also, the per-dollar profit return indicated by the ROA ratio in an important bank management metric. Because banks are highly leveraged, even an ROA as low as 1% or 2% can lead to substantial revenue and profits in banking.

Banking ratios for efficiency are bank-specific ratios that measure the efficiency of different bank operations. Common banking ratios for efficiency include the efficiency ratio, the operating leverage ratio, and the loan-to-assets ratio.

The efficiency ratio measures the efficiency of a bank’s operations by dividing a bank’s non-interest expense by its revenue. The reason why the efficiency ratio doesn’t measure interest expense is that banks can’t control interest expense in the way that they can control non-interest expense. As a result, the efficiency ratio of a bank paints a more accurate picture of the efficiency of that bank’s operations.

A lower efficiency ratio means a bank is more efficient. A lower ratio indicates that there’s less non-interest expense per dollar of banking revenue. A higher ratio indicates that there’s more non-interest expense per dollar of revenue.

The operating leverage ratio measures banking efficiency by comparing the growth of revenue with the growth of non-interest expenses. To calculate operating leverage, you must subtract the growth rate of non-interest expense from the growth rate of revenue. If this calculation results in a positive number, then revenue is growing faster than expenses.

On the other hand, if the result is negative, the bank is accumulating expenses faster than revenue. A bank accumulating expenses faster than revenue suggests inefficiencies in operations.

Investors use the loan-to-assets ratio to analyze a bank’s operations. Banks with a higher loan-to-assets ratio receive more of their income from loans than investments. Banks with lower levels of loan-to-asset ratios receive more of their income from more diversified, non-interest-earning sources such as asset management or trading.

To build a well-rounded career in banking and finance, you’ll need to learn all there is to know about bank regulatory ratios and capital requirements, along with other terms and resources. To expand your knowledge on all things finance and banking, take advantage of the numerous courses CFI offers, including courses on financial analysis, modeling and valuation, and capital markets.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.