Get In-Demand Finance Certifications

Within any industry, including banking and finance, navigating uncertainties is an integral part of success. This article highlights the importance of risk management professionals in developing risk management frameworks, as well as exploring the role of risk management within a broader business strategy.

Primarily, risk management is responsible for identifying, assessing, monitoring, and mitigating various types of risks that the bank faces. These potential risks can include credit risk, market risk, liquidity risk, operational risk, compliance risk, and strategic risk, among others.

Risk management develops and implements policies, procedures, and frameworks to ensure that risks are managed within acceptable limits and in accordance with regulatory requirements.

Additionally, risk management provides guidance and support to business lines in understanding and managing risks inherent in their activities, while also providing independent oversight to ensure risk-taking activities are prudent and aligned with the bank’s risk appetite.

Furthermore, risk management plays a crucial role in regulatory compliance, reporting, and stress testing, helping the bank demonstrate its ability to withstand adverse scenarios and meet regulatory expectations.

While risk management functions autonomously to assess and manage risks across banks and other financial institutions, they typically collaborate closely with business units to understand their activities, products, and strategies. This partnership ensures that risk management practices are aligned with the objectives of the business lines while also providing independent oversight and guidance to mitigate risks effectively.

Risk culture refers to the collective attitudes, behaviors, and values within an organization regarding risk management. An effective risk culture within an organization plays a fundamental role in raising risk awareness, as well as supporting and enhancing an effective risk management framework in several ways.

First, it fosters a proactive and risk-aware mindset among employees, encouraging them to identify, assess, and mitigate risks as an integral part of their roles and responsibilities. This helps in early identification and mitigation of risks, reducing the likelihood of adverse events.

Second, a strong risk culture promotes open communication and transparency regarding risks, facilitating the sharing of risk-related information across departments and levels of the organization. This enables more informed decision-making and ensures that risks are appropriately considered in strategic planning and day-to-day operations.

Third, an effective risk culture encourages accountability for risk management, where individuals take ownership of managing risks within their areas of responsibility. This helps in ensuring that risk management practices are consistently applied throughout the organization.

Overall, a robust risk culture not only supports the implementation of risk management processes but also enhances their effectiveness by creating an environment where managing risks is ingrained in the organization’s DNA.

Here are several benefits provided by managing risks effectively:

Effective risk management shields businesses from the potential negative impact risk events can have on an organization.

For example, any bank faces a wide range of risks. One significant risk is loans not being repaid, which can lead to financial losses. Another risk is market fluctuations, such as interest rate changes or currency value swings, which can affect the bank’s profits. Operational risks, like system failures or human errors, are also a concern.

By effectively managing these risks, banks can maintain stability and protect themselves from potential financial losses. It’s all about finding the right balance between caution and adaptability in the ever-changing world of finance.

Risk management failures can lead to enormous reputational damage, especially in the highly regulated and interconnected financial sector. Given the trust-centric nature of banking, any perceived or actual lapse in integrity, security, or compliance can quickly erode customer confidence and investor trust, leading to substantial financial losses and regulatory scrutiny.

By implementing robust risk management practices, banks can proactively identify, assess, and mitigate risks that threaten their brand reputation, such as fraud, data breaches, or unethical behavior. This includes stringent compliance measures, rigorous due diligence procedures, and ongoing monitoring of internal processes and external factors.

Banks are in the business of taking risk. By carefully assessing and understanding the potential risks associated with various ventures, senior management can strategically leverage opportunities to innovate, diversify their offerings, and gain a competitive advantage in the market.

For instance, a bank might consider investing in new financial technologies or expanding its services into untapped markets, knowing that the calculated risks taken can lead to substantial growth and innovation within the institution.

In any industry, let alone banking and finance, the significance of informed decision-making cannot be overstated. Comprehensive risk management plays a pivotal role in this process, offering valuable insights into the dynamic landscape of risks and rewards.

By conducting thorough analyses, organizations can better understand the intricacies of various opportunities and challenges, empowering them to make strategic choices with confidence and foresight.

It is through rigorous risk analysis that an organization assesses the viability of potential investments and the allocation of resources to maximize returns. This approach ensures that every decision is grounded in a thorough understanding of the associated risks and potential rewards, laying the groundwork for sustainable growth and success.

Within the banking and finance industry, resilience stands as a fundamental pillar of survival and success. Cultivating a culture of risk awareness and preparedness is paramount, allowing financial institutions to navigate through uncertain conditions and rebound from challenges with agility.

Consider the scenario of a bank that foresees potential economic downturns and strategically diversifies its investment portfolio to mitigate risks, thereby safeguarding its stability and continuity amidst market volatility.

By proactively identifying vulnerabilities and implementing robust plans to manage risks, financial institutions can fortify themselves against the potential impact of industry shocks, ensuring the organization’s ability to continue to offer their customers uninterrupted service delivery as well as preserving stakeholder trust.

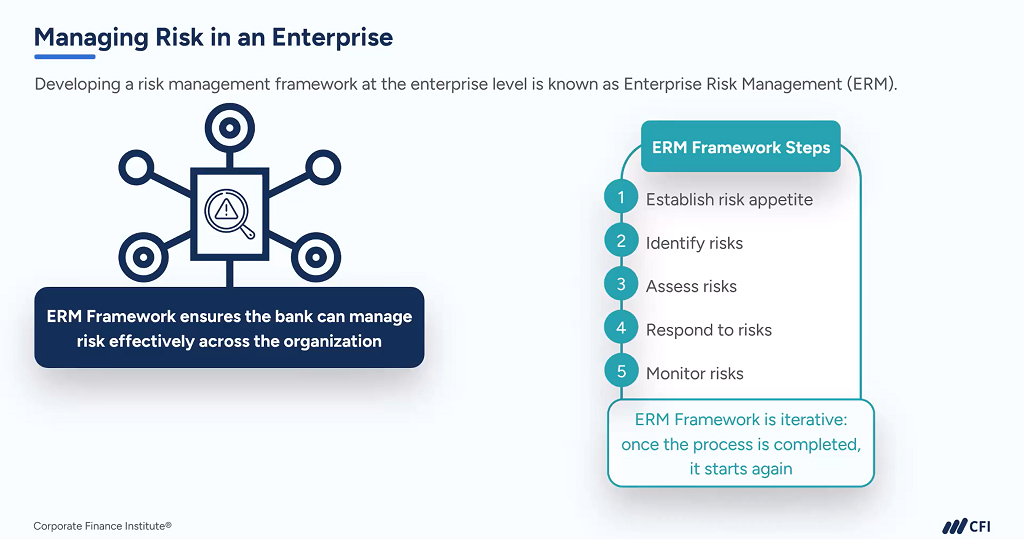

Risk and business leaders within any organization, whether it be a bank or non-bank, are responsible for implementing an effective risk management plan across the entire business. This framework is called an Enterprise Risk Management (ERM) framework.

An ERM framework is a comprehensive approach to identifying, assessing, and responding to risks across an entire organization. At a high level, the process can be broken down into the following five steps:

The initial stage of effective Enterprise Risk Management involves defining the organization’s risk appetite — the threshold of risk it is willing to accept while pursuing its strategic objectives.

For instance, a financial institution may exhibit a heightened risk appetite concerning investment ventures and market expansions yet demonstrate a more conservative stance regarding credit risk and regulatory compliance.

By clearly defining these boundaries, banking and financial entities can align their risk-taking behaviors with their organizational ethos, thereby optimizing decision-making processes and enhancing overall risk governance.

Once the risk appetite is established, the next step is identifying potential risks that could impact the organization’s objectives. This involves conducting a thorough assessment of both internal and external factors that could pose threats or opportunities.

Internal risks may include operational inefficiencies, employee turnover, or cybersecurity vulnerabilities, while external risks may include market volatility, regulatory changes, or geopolitical instability.

Utilizing tools such as a centralized risk register, brainstorming sessions, and stakeholder interviews can help identify potential risks across all areas of the organization.

Identified risks are then assessed on their likelihood and potential impact. Risk assessment involves quantifying risks based on factors such as the probability of the risk occurring, the severity of the impact should the risk occur, and velocity, or how quickly the risk could develop.

For example, a financial institution may assess the risk of a cyberattack by considering the likelihood of a breach occurring and the potential financial losses associated with it.

Risk assessment techniques such as scenario analysis, risk heat maps, and Monte Carlo simulations can help organizations prioritize risks and allocate resources effectively.

Once risks are assessed, the organization must develop strategies to respond to them effectively. There are four ways to respond:

A bank may choose to avoid the avoid the risk entirely. This risk management approach is especially appropriate when there is zero risk appetite for it. For example, a bank may decide against setting up new business operations in a specific country if the political and economic landscape is too uncertain.

Reducing risk could be appropriate if the risk is above a bank’s risk appetite, but it still wants to accept some exposure to this risk. For example, a bank may use artificial intelligence to scan and analyze internal data to reduce the chance of financial fraud.

Risk transfer is another response risk. In this scenario, a bank moves the responsibility of the risk to a third party. Hedging and insurance are two risk transfer techniques.

Risk acceptance is the fourth response to risk. Any time a bank decides to lend money to a customer, when it enters into a financial transaction within another bank, or when it onboards a new customer, a bank is accepting risk.

The final step in the ERM framework is to continuously monitor and review risks to ensure that the organization’s risk management strategies remain effective. This involves tracking key risk indicators, monitoring changes in the internal and external environment, and reassessing risks as new information becomes available.

Regular risk reporting and communication with stakeholders are essential to keep everyone informed and engaged in the risk management process.

In today’s fast-paced and often volatile banking and finance industry, the importance of effective risk management is more crucial than ever. With technological advancements, globalization, and evolving market dynamics, risks are evolving at an exponential rate. From cybersecurity threats to regulatory changes, organizations must stay ahead of the curve to mitigate potential risks effectively.

Also, as businesses expand globally and embrace new technologies, the risk landscape becomes increasingly complex. Traditional risk management approaches may fall short in addressing multifaceted risks, necessitating innovative strategies and tools.

In the interconnected world of banking and finance, risks are not confined to individual organizations; they can have cascading effects across entire financial services ecosystem. For instance, a cyberattack on a major financial institution can ripple through the entire banking sector, underscoring the need for collaborative risk management efforts.

New risks, from climate change to geopolitical instability, are constantly emerging on the horizon. Organizations must stay vigilant and adapt their risk management strategies to address these evolving threats proactively.

Finally, regulatory requirements are becoming increasingly stringent, placing greater emphasis on effective risk management practices. Non-compliance can lead to severe penalties, legal liabilities, and reputational damage, highlighting the importance of robust risk management frameworks.

The importance of risk management cannot be overstated. By embracing proactive risk management strategies and implementing robust risk management plans, organizations can safeguard their financial future, capitalize on opportunities, and thrive in a rapidly evolving landscape.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Analyzing Growth Drivers & Business Risks Course

Enterprise Risk Management for Financial Institutions

Financial Risk Management Process