Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The replacement of an existing debt by means of another debt with more favorable terms and/or conditions

Debt refinancing is the replacement of an existing debt by means of another debt with terms and/or conditions that are more favorable. In other words, debt refinancing refers to the replacement of existing debt with new debt.

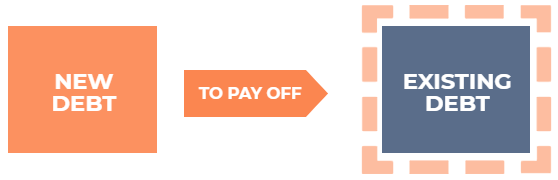

Debt refinancing is commonly used to take advantage of new financing that offers more favorable terms and/or conditions. In such a situation, an individual or company will settle their outstanding debt by issuing new debt with more favorable terms. The process is illustrated below:

The most common reasons to refinance debt are:

An individual currently has $1,000,000 remaining on their mortgage for 20 years at 10%. In such a situation, the monthly installment payments (principal and interest) would be $9,650. The bank has indicated to the individual that they can refinance to a 7% loan for 20 years due to a decrease in the bank’s interest rate.

As such, the monthly mortgage installment payments would be $7,753. If the individual refinances their mortgage, they would be saving $1,897 ($9,650 – $7,753) in monthly installment payments.

Although refinancing existing debt is an attractive option for borrowers, it may not be feasible in some cases. Debt may include call provisions so that a penalty payment is incurred to the borrower if they refinance the debt. In addition, there may be closing and/or transaction fees associated with refinancing existing debt.

As such, although an individual or company may have the option to secure better terms and/or conditions on their debt, it may not be ideal to do so given the penalty payments, closing fees, and/or transaction fees.

In the example above, refinancing the debt would save the individual approximately $455,280 over the life of the mortgage. If the penalty payment, closing fees, and/or transaction fees do not amount to $455,280, the individual should refinance the debt. If the penalty payment, closing fees, and/or transaction fees exceed $455,280, it would not be in the individual’s best interest to refinance their debt.

The two terms are commonly used interchangeably. Readers should note that they are actually different.

To reiterate, debt refinancing involves replacing existing debt with new debt that offers more favorable terms or conditions. On the other hand, debt restructuring refers to the restructuring of existing debt. It can be in the form of delaying interest payments or extending the term of the debt. Debt restructuring is commonly used by a company approaching bankruptcy that needs to restructure its debt to stay afloat.

For example, in September 2018, Sears Holdings Corp. proposed restructuring the company’s debt to avoid bankruptcy. As such, debt restructuring was used to restructure the company’s debt structure, which was near-bankrupt.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA®) certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: