Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Measures a company’s capacity to meet debt obligations using cash generated from operating activities

The Debt Service Coverage Ratio (sometimes called DSC or DSCR) is a credit metric used to understand how easily a company’s operating cash flow can cover its annual interest and principal obligations.

Because the Debt Service Coverage Ratio also includes principal obligations in the denominator, it’s considered a very useful metric when a corporate borrower has reducing term debt in its capital structure (meaning monthly or annual principal repayments).

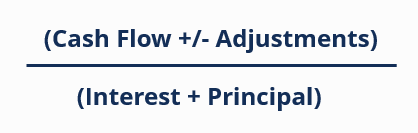

Conceptually, the idea of DSCR is:

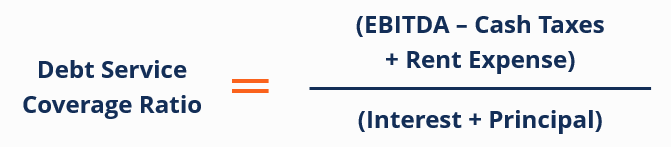

Debt Service Coverage is usually calculated using EBITDA as a proxy for cash flow. Adjustments will vary depending on the context of the analysis, but the most common DSCR formula is:

Where:

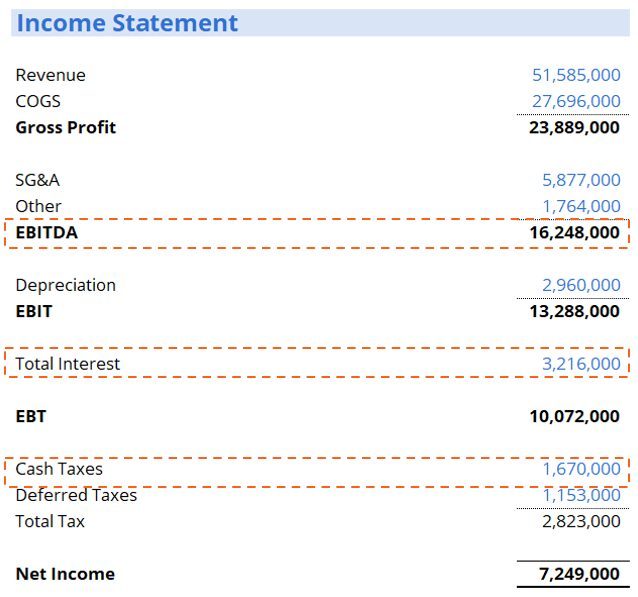

Let’s look at an example. Assume the client below had $20 million in long-term debt plus $5 million in current portion of long-term debt (CPLTD). Based on that information, plus what’s been provided in the income statement below, what is the borrower’s DSCR?

We would plug the numbers into our DSCR formula and calculate as follows:

The Debt Service Coverage Ratio (DSC) is one metric within the “coverage” bucket when analyzing a company. Other coverage ratios include EBIT over Interest (or something similar, often called Times Interest Earned), as well as the Fixed Charge Coverage Ratio (often abbreviated to FCC).

Coverage measures are never taken in isolation when analyzing a company; they’re always used in conjunction with other categories of credit metrics like leverage (Debt-to-Equity, Funded Debt-to-EBITDA, etc.) and liquidity (Current Ratio & Quick Ratio)

DSC is calculated on an annualized basis – meaning cash flow in a period over obligations in the same period. This is in contrast to leverage and liquidity, which represent a snapshot of the borrower’s financial health at a single point in time (usually period end).

In all adjustment scenarios, a higher DSCR is considered better than a lower one. Anything less than 1x (or 1:1) is considered very weak and suggests that a company owes more money to creditors (per year) than it generates in cash per year.

Most commercial banks and equipment finance firms want to see a minimum of 1.25x but strongly prefer something closer to 2x or more. Many small and middle market commercial lenders will set minimum DSC covenants at not less than 1.25x.

While most analysts acknowledge the importance of assessing a borrower’s ability to meet future debt obligations, they don’t always understand some of the nuances of the DSCR formula.

Common questions include:

EBITDA is not cash flow. However, it often serves as a proxy for it because it’s easy to calculate, and both its definition and its purposes are generally agreed-upon across jurisdictions.

Some important points include:

In most jurisdictions, income taxes owing to the regional or federal governments count as “super-priority” liabilities (meaning they rank above even the senior-most secured creditors).

Basically, the cash portion of taxes owing (meaning any non-deferred portion) must be paid in order for the business to continue operating unimpeded by intervention from tax authorities.

Cash flow (as expressed on the CF statement) includes increases and decreases of cash like tightening or extending payable days, increasing or decreasing inventory turns, and collecting payments more (or less) quickly from customers.

Because these fluctuate from period to period and are heavily influenced by market forces and supply chain relationships, CF from operations does not always represent a company’s ability to consistently generate earnings and cash flow from its core business operations. This is largely why EBITDA is used.

Debt Service Coverage formulas and adjustments will vary based on the financial institution that’s calculating the ratio as well as the context of the borrowing request.

Some examples include:

CAPEX stands for Capital Expenditure. Some businesses require constant reinvestment in order to remain competitive.

Some management teams elect to use cash on hand to support some or all of that CAPEX (meaning it’s not funded by debt, which would be captured in the denominator of the DSC ratio).

In these cases, that’s cash that’s gone and can no longer be used to service debt. Some more conservative lenders will adjust EBITDA accordingly when calculating DSC for CAPEX-heavy industries.

Because personal income tax rates can be quite high in many jurisdictions, some owner-operators of small and medium-sized businesses pay themselves a modest management “salary” and instead take compensation through dividends or by moving funds in and out of the shareholder loan accounts.

Adjusting for cash outflows that effectively represent ownership’s compensation gives a more accurate picture of the company’s ability to generate actual profits and cash flows for the purpose of retention in the company (as opposed to funding the owner’s lifestyle).

Consider a company that’s been renting its warehouse but recently exercised an option to purchase the building. This company’s historical income statements show “rent expense,” but that expense will no longer exist once it owns the building.

Assuming the company was looking to take out a Commercial Mortgage to support the property acquisition, the mortgage lender would need to add back rent to the numerator to understand the going-forward cash flow.

Of course, the “new” occupancy cost would be captured in the denominator as the principal and interest obligations for the commercial mortgage loan.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Debt Service Coverage Ratio. Check out some of our resources below to expand your knowledge and further your career!